Select a Market Report to Read:

- National Market Update Overview

- Bay Area Report

- North Bay Report

- East Bay Report

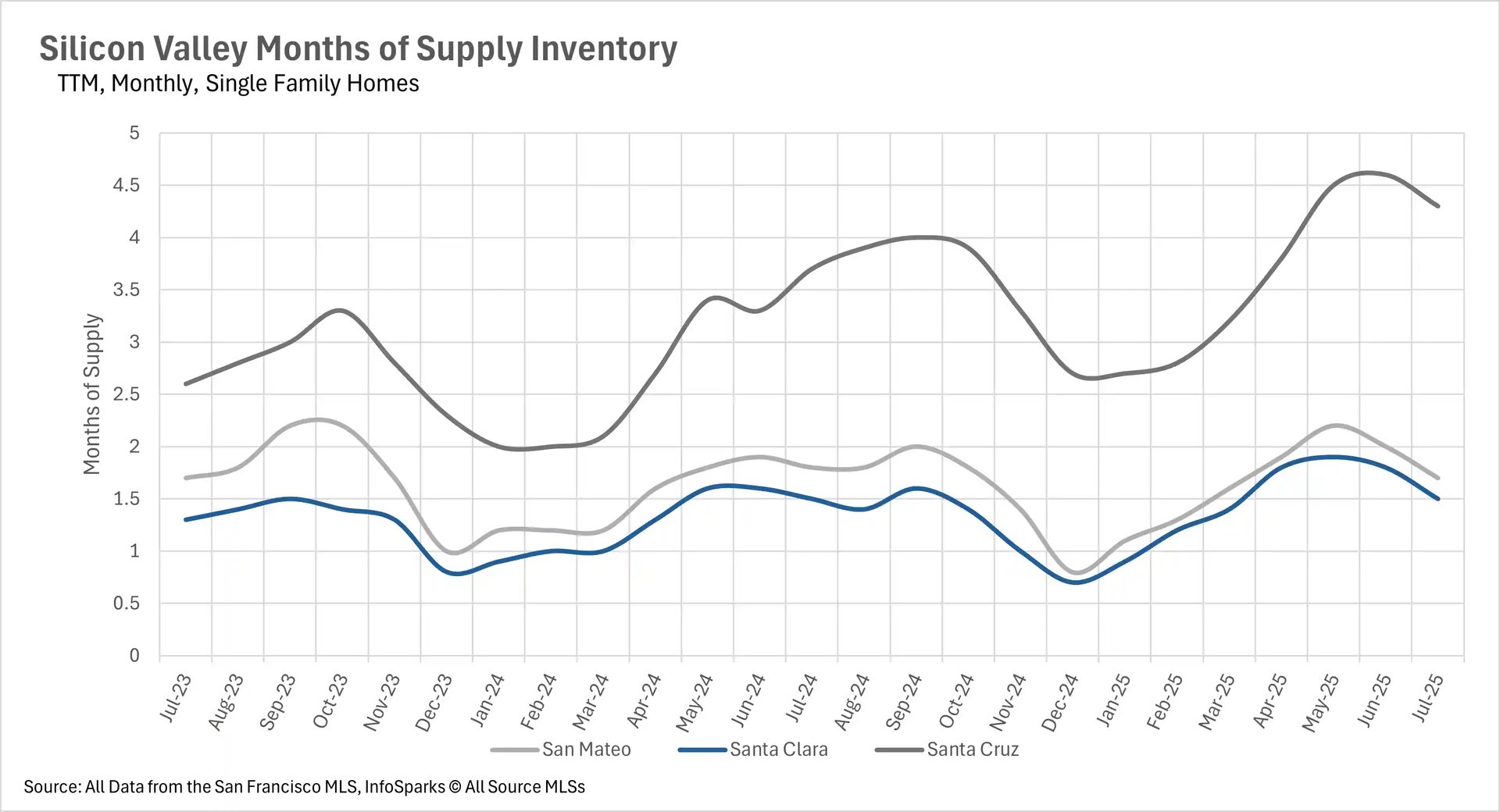

- Silicon Valley Report

- San Francisco Report

The Local Lowdown

Quick Take:

- Median sale prices show mixed performance across the Bay Area, with Silicon Valley maintaining strength while the East Bay experiences six consecutive months of declines.

- Inventory dynamics vary dramatically by region - San Francisco faces severe shortages while most other areas see rising inventory levels.

- Despite varying inventory conditions, listings are spending significantly more time on the market across nearly all Bay Area markets.

- Market conditions range from highly competitive sellers' markets in core Silicon Valley to more balanced or buyer-friendly conditions in outlying areas.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

Regional price performance reveals a tale of two markets

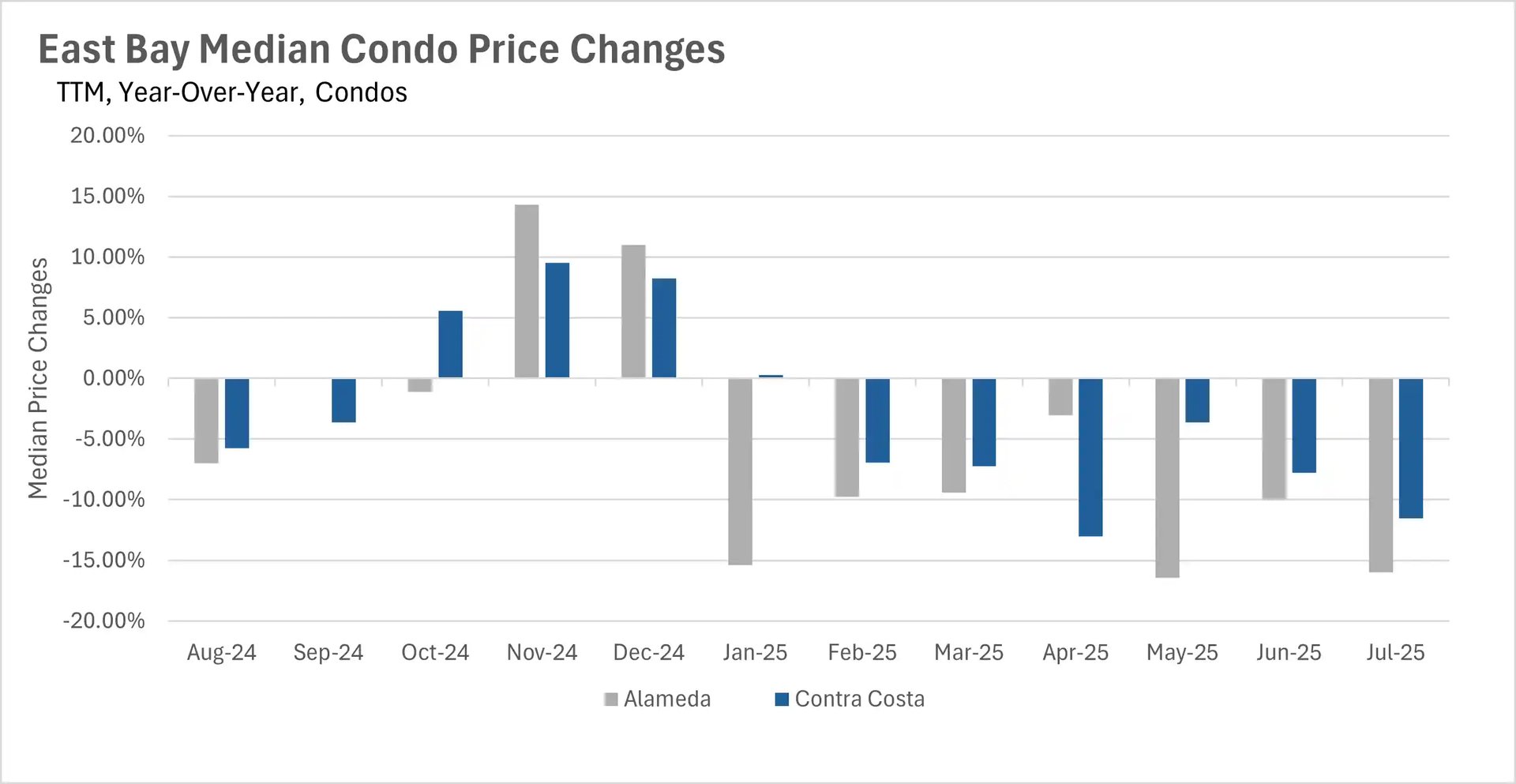

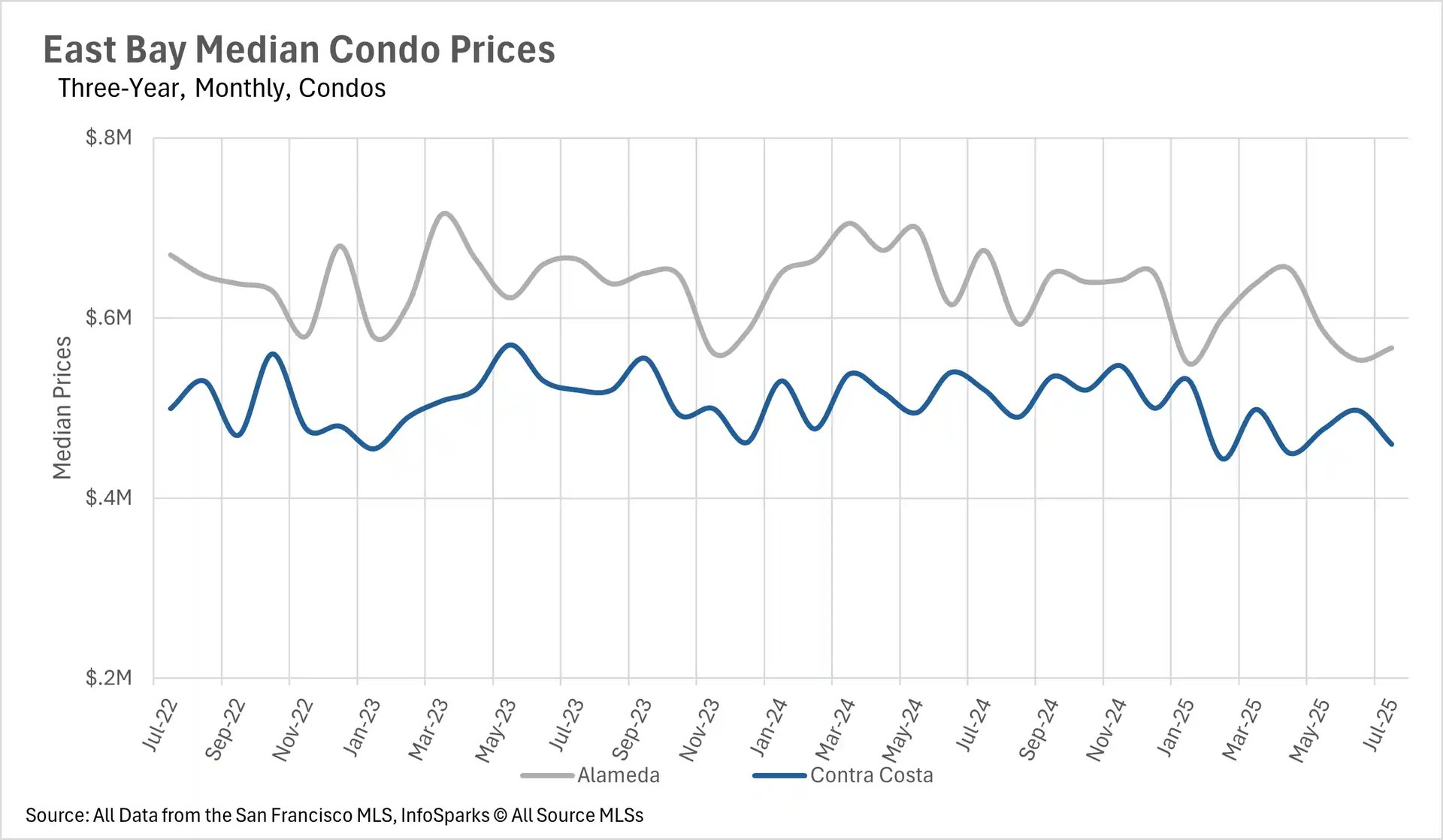

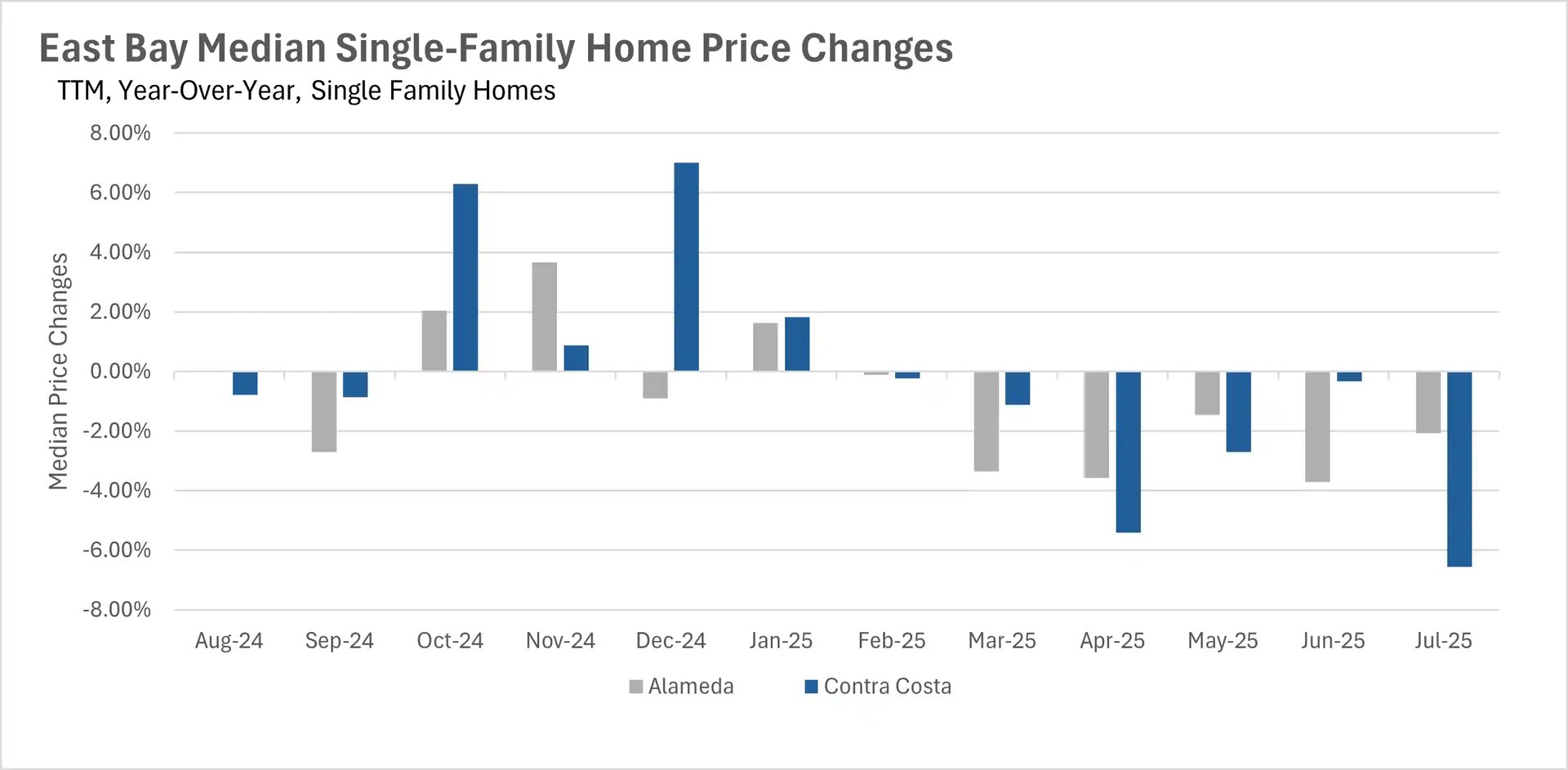

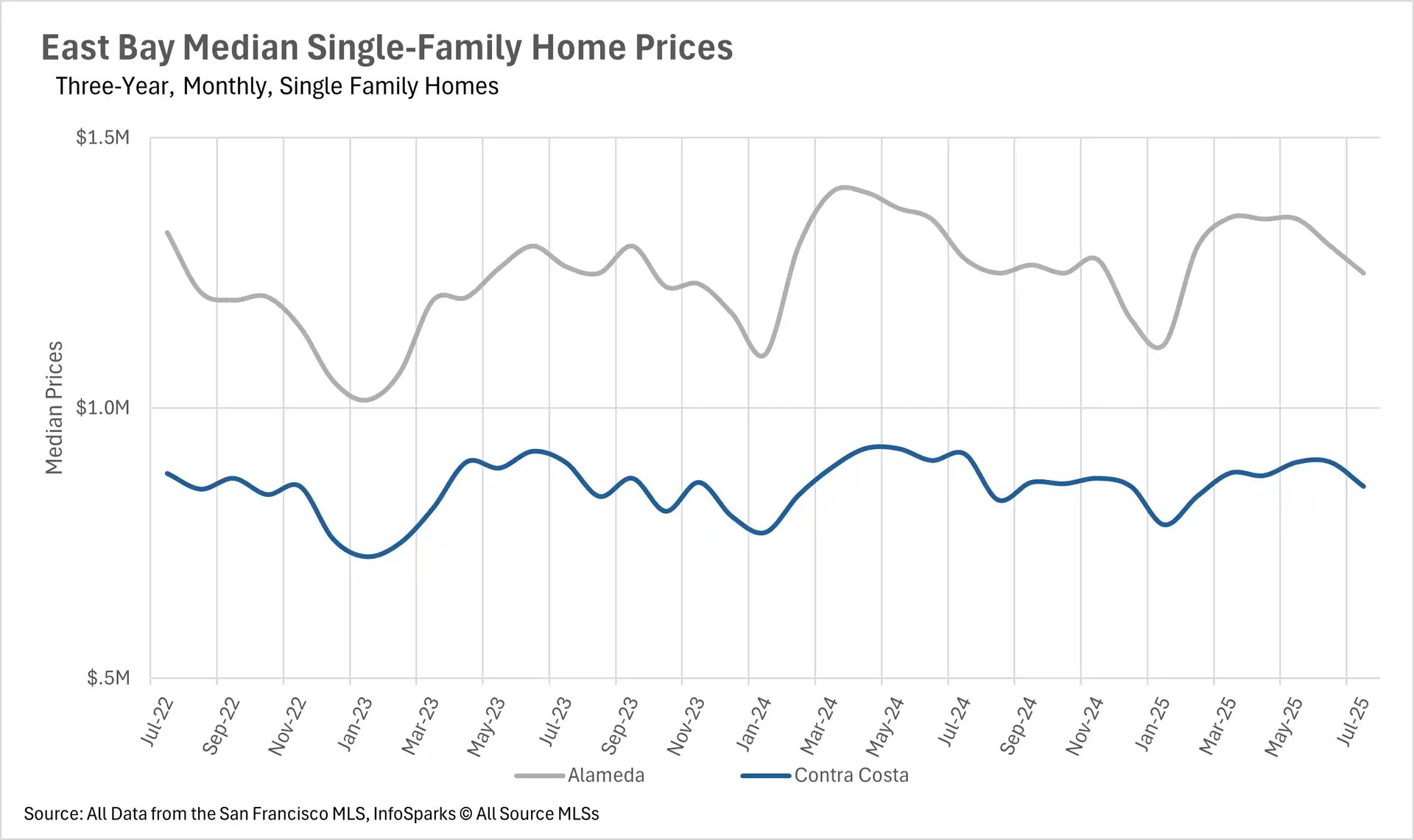

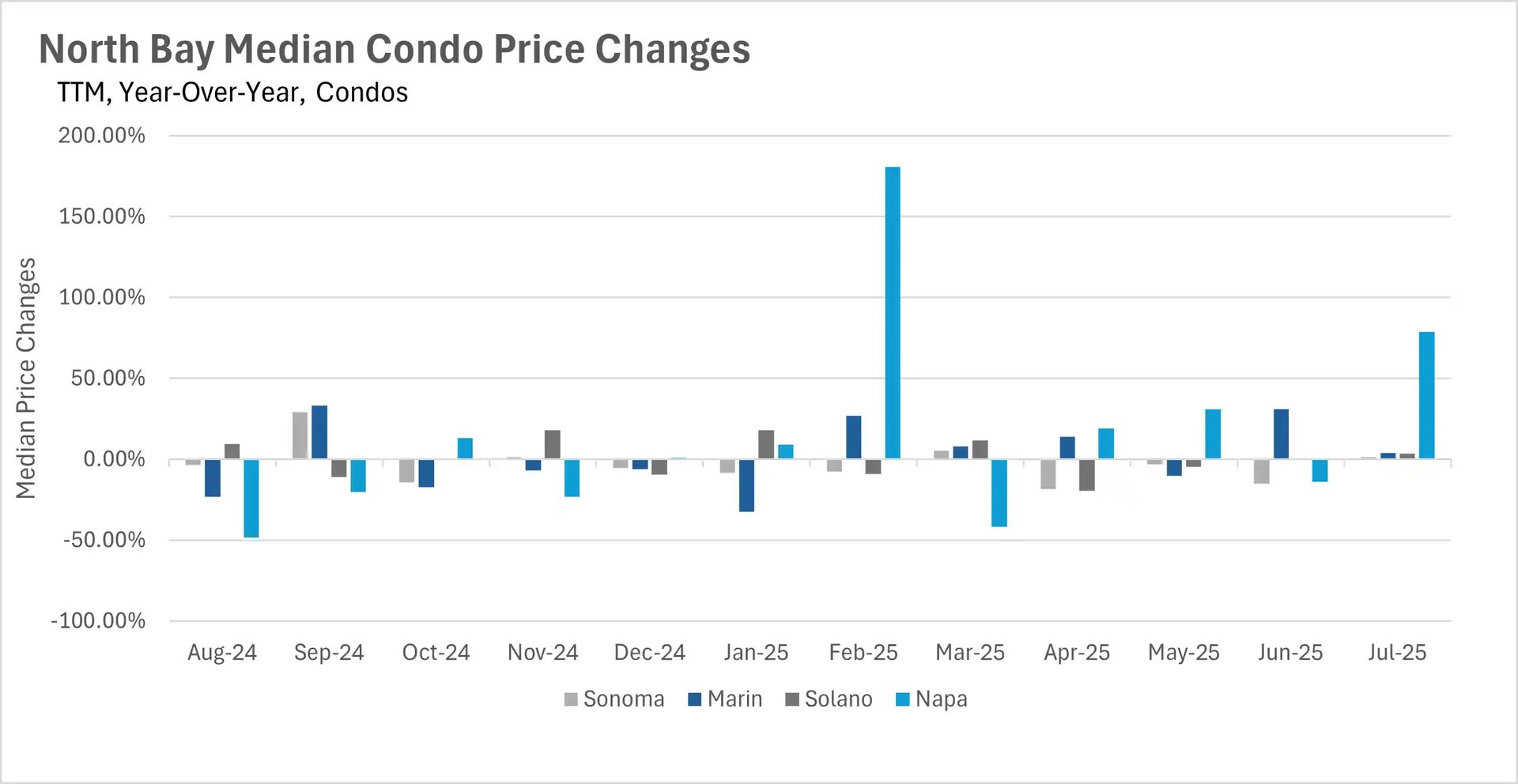

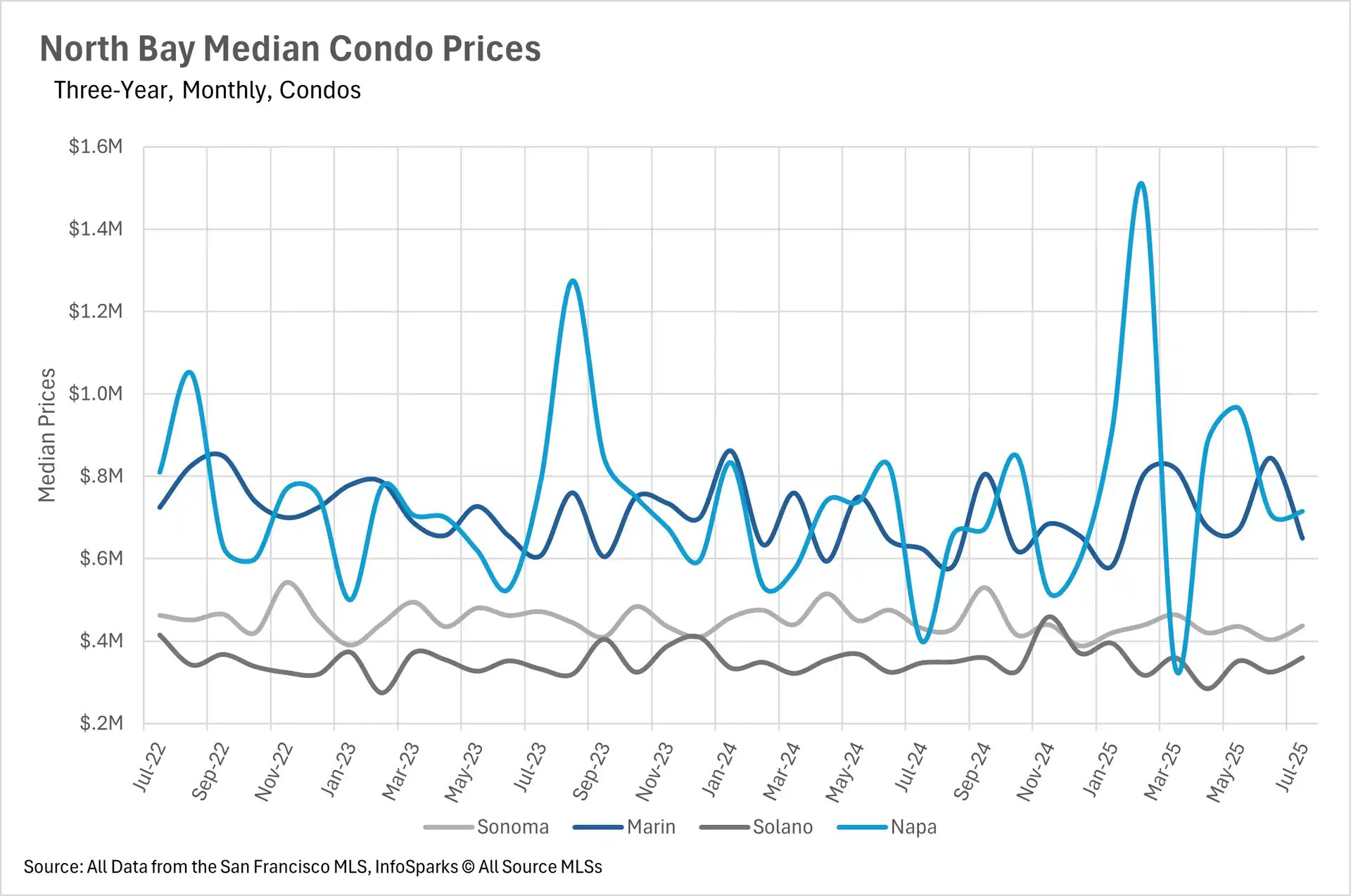

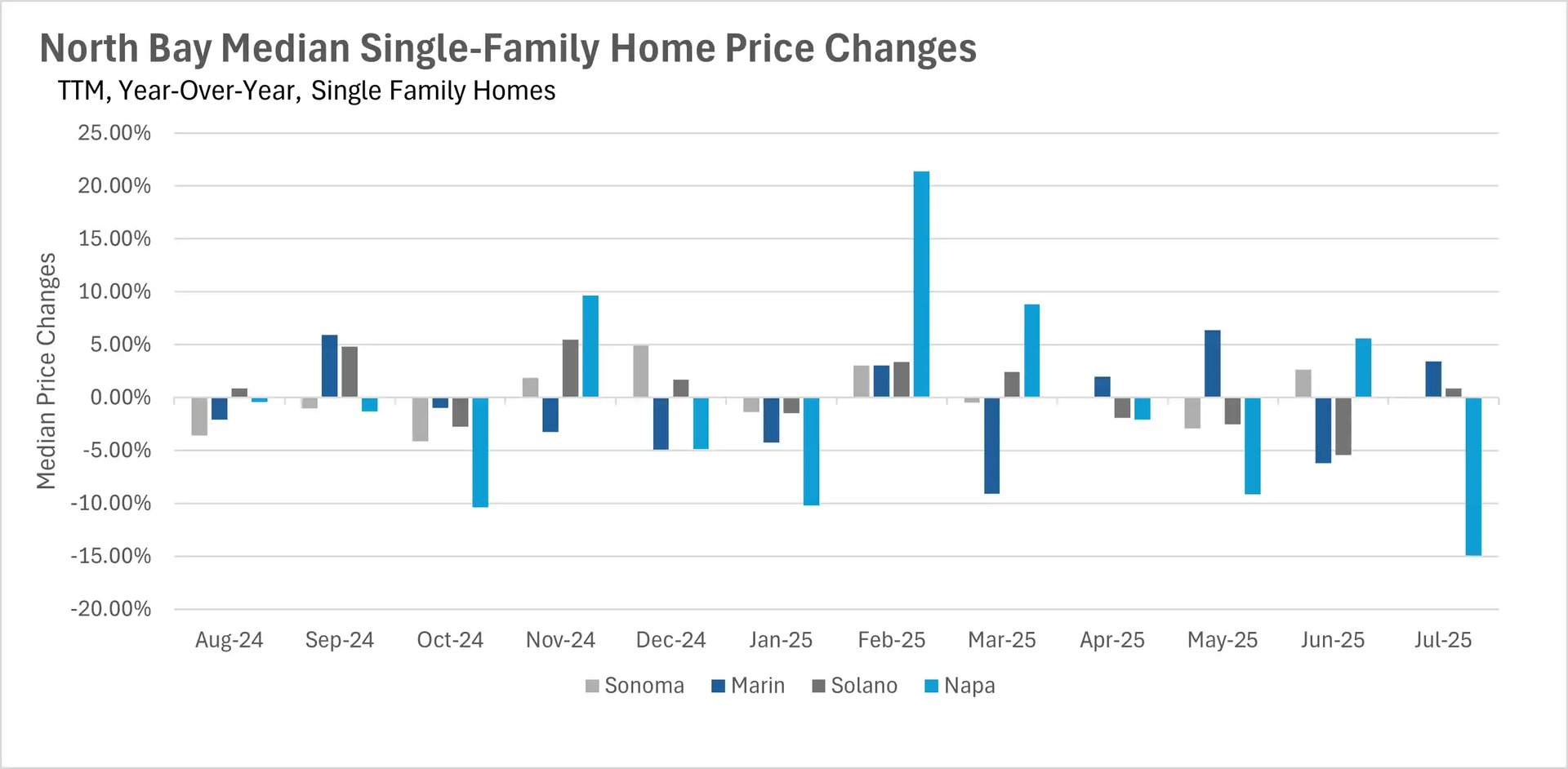

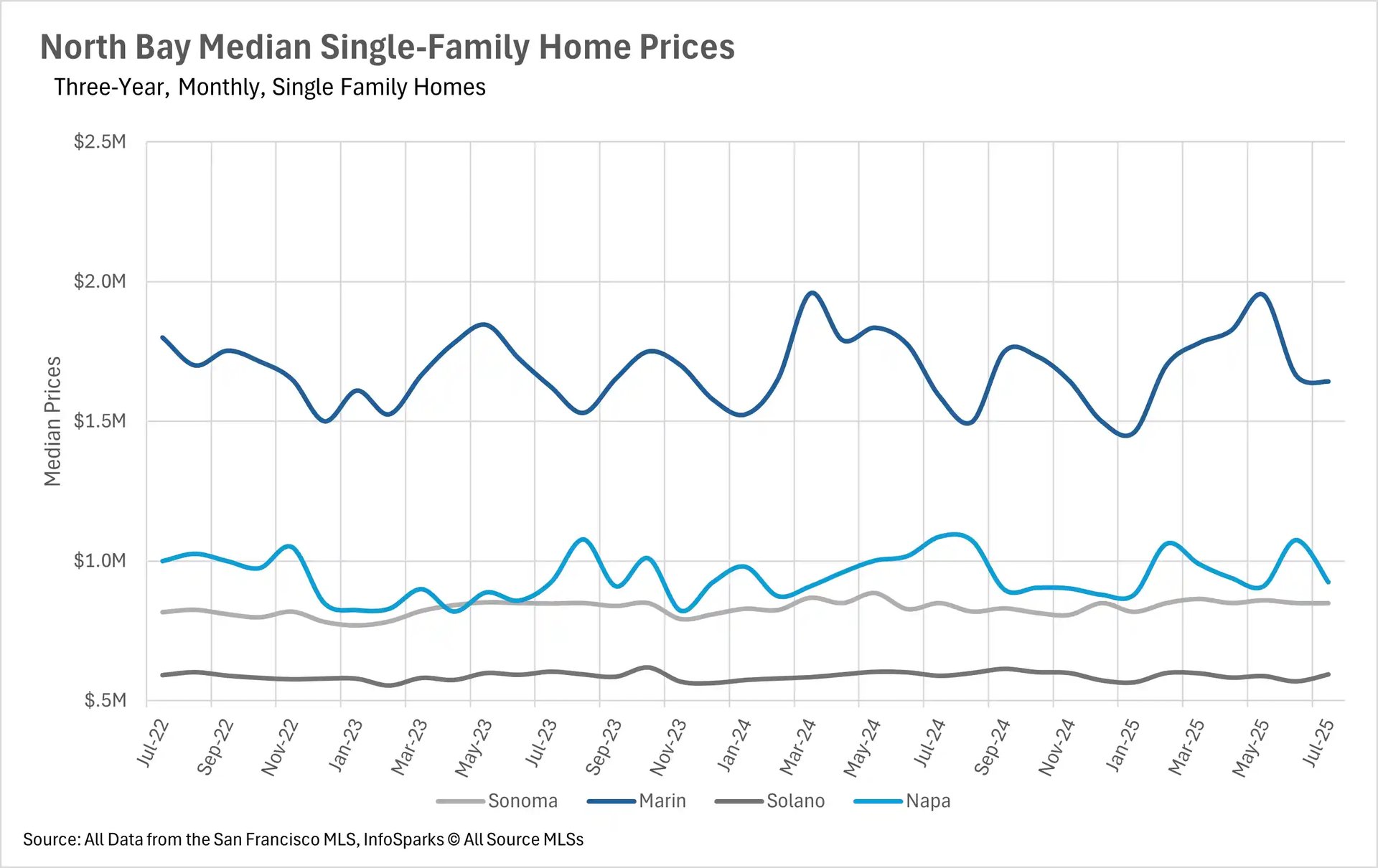

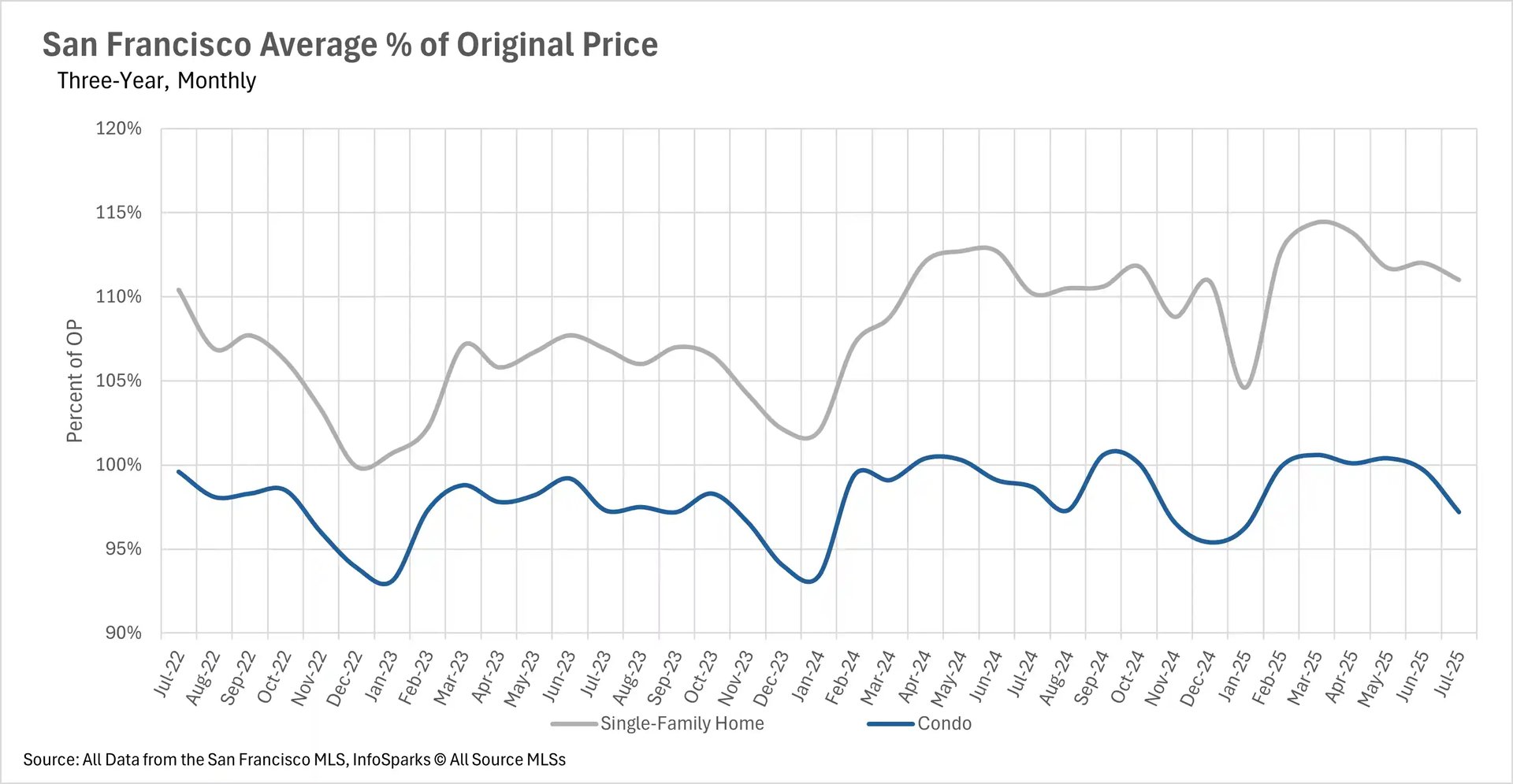

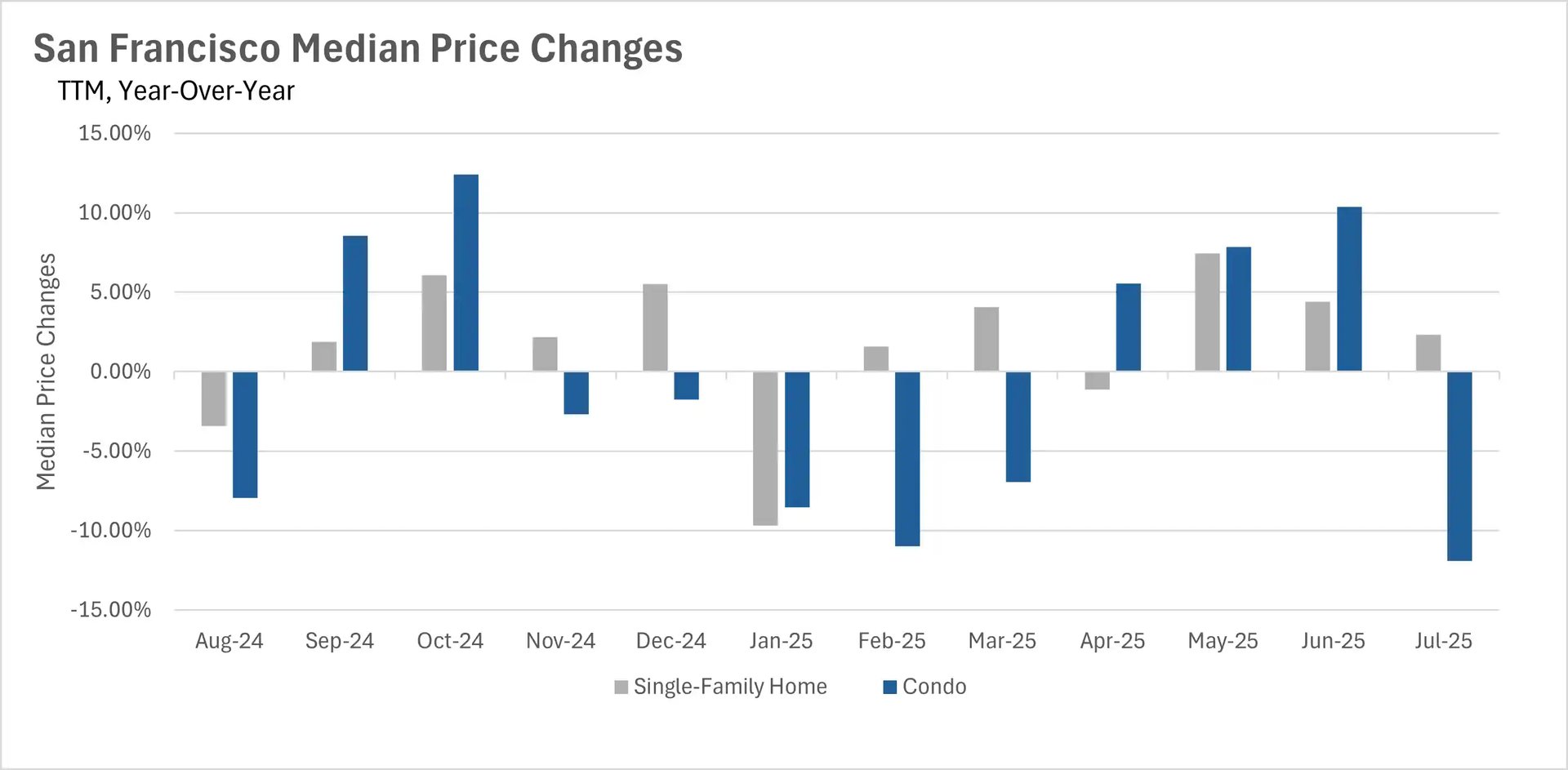

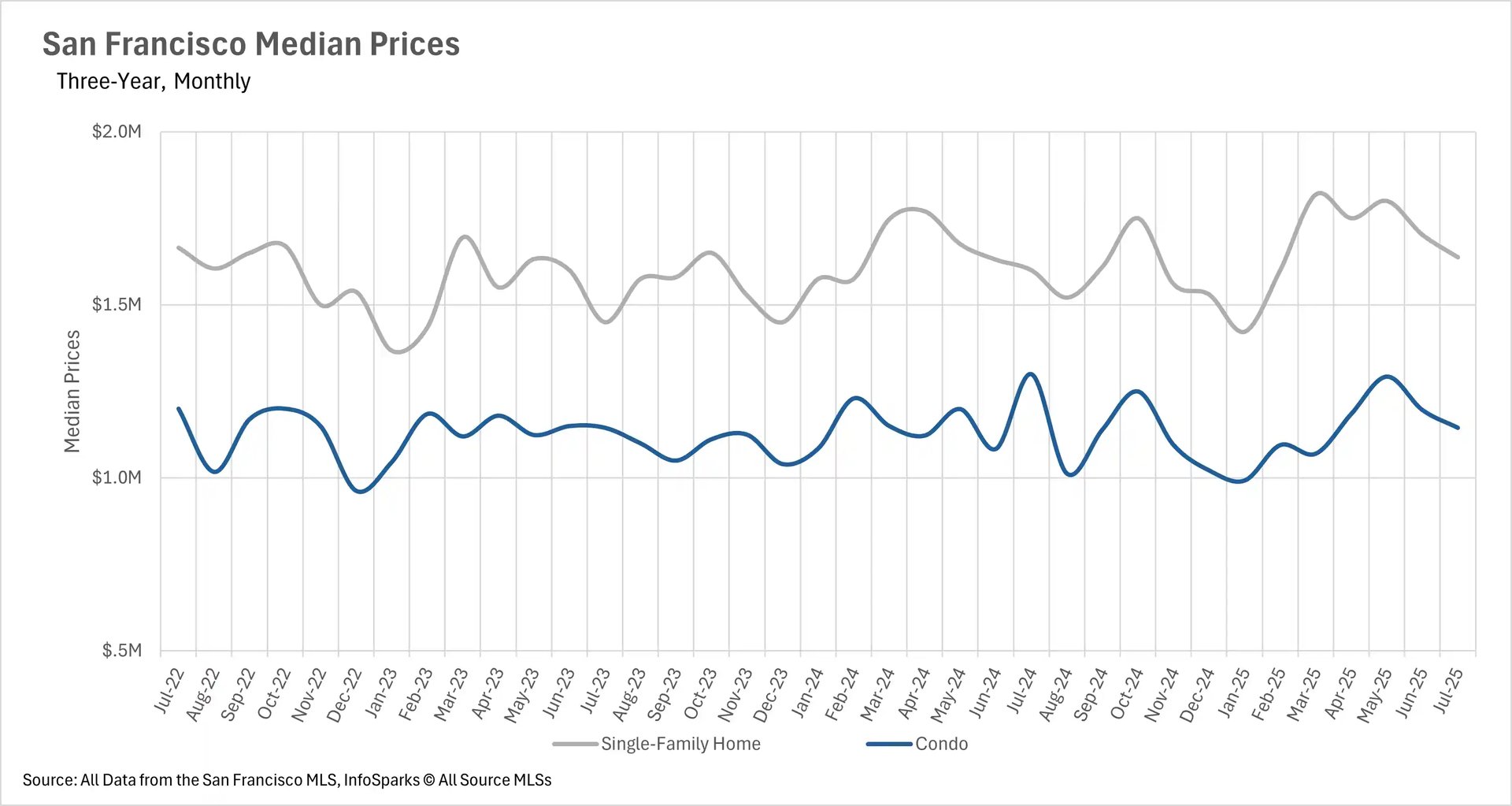

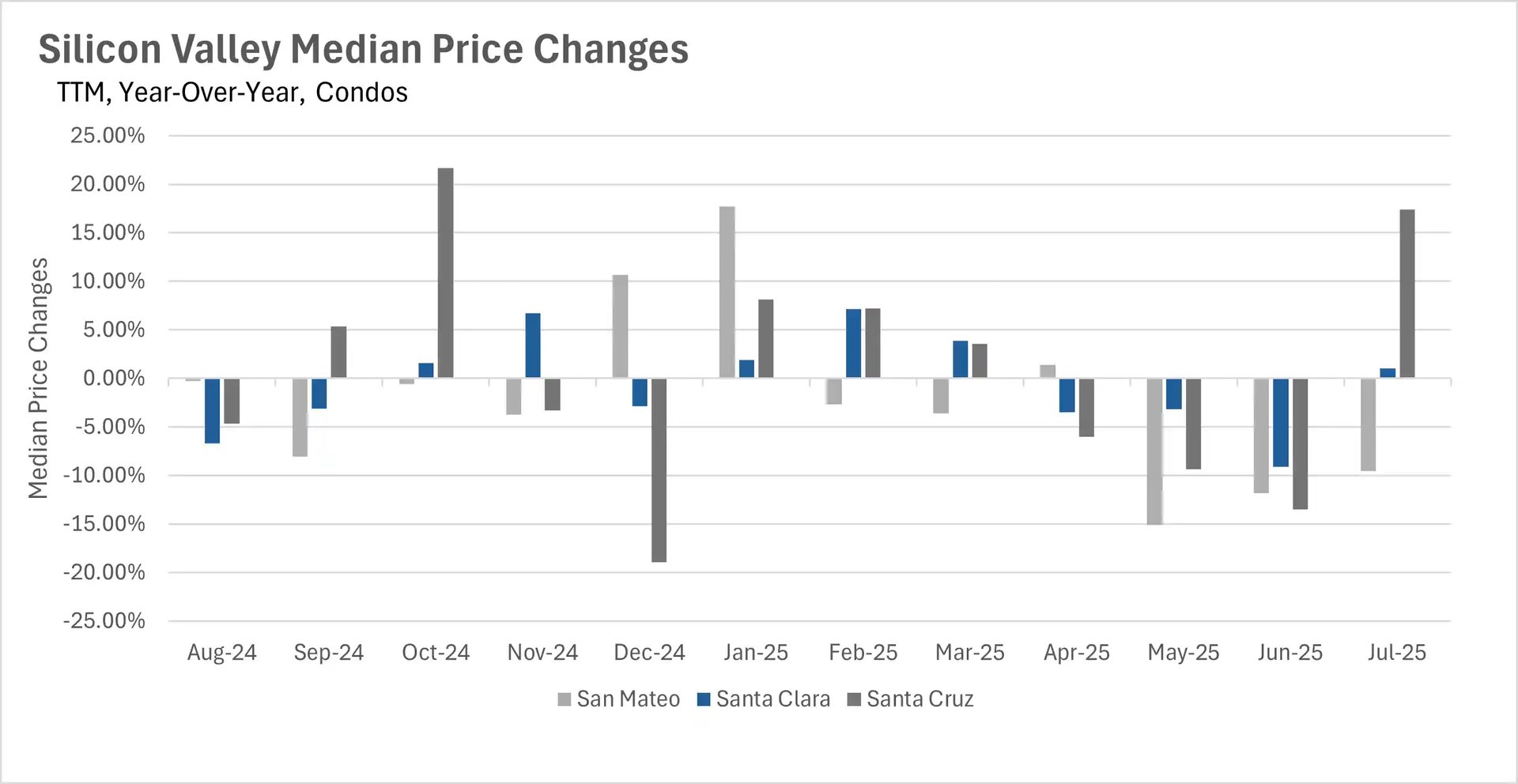

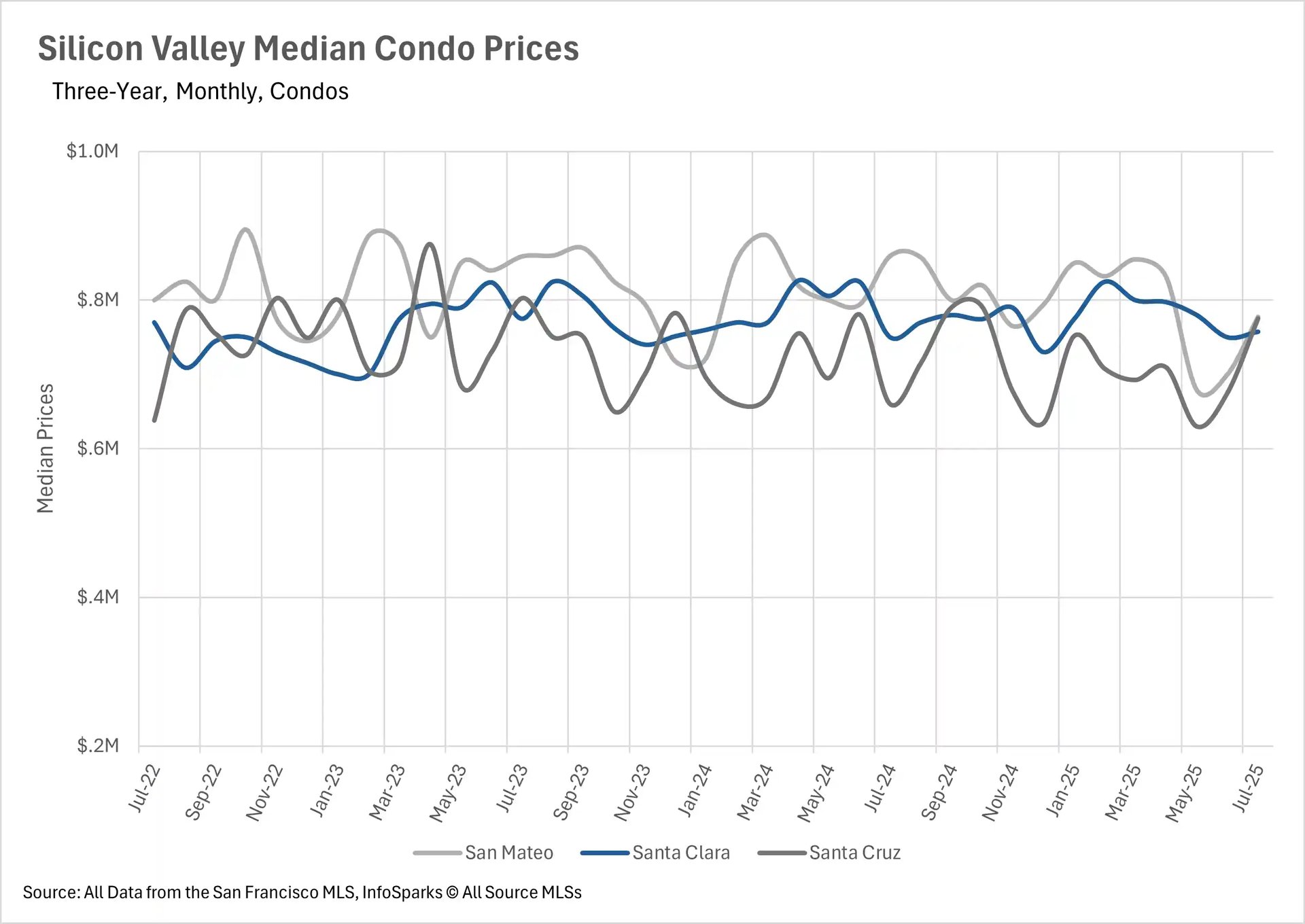

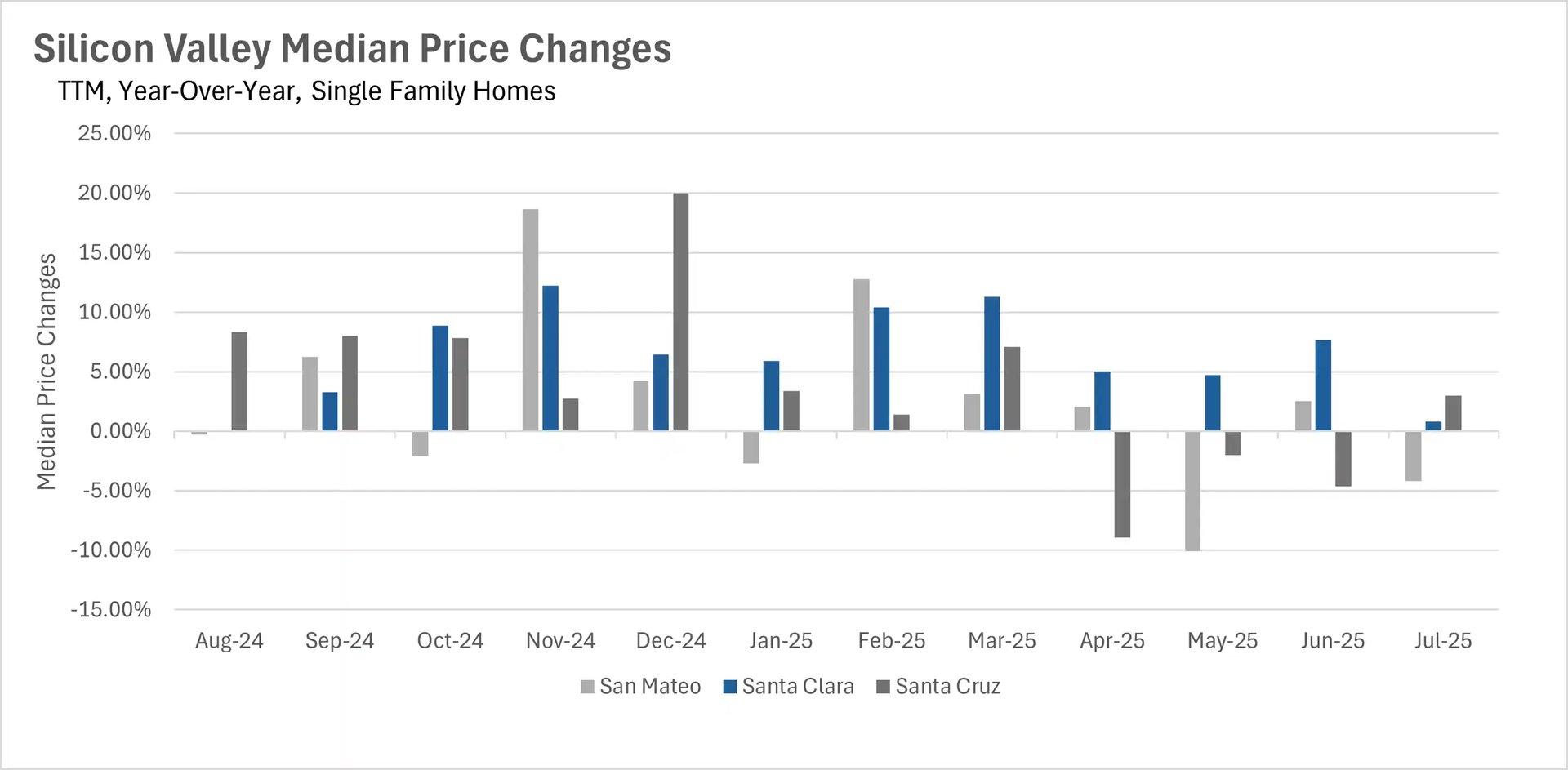

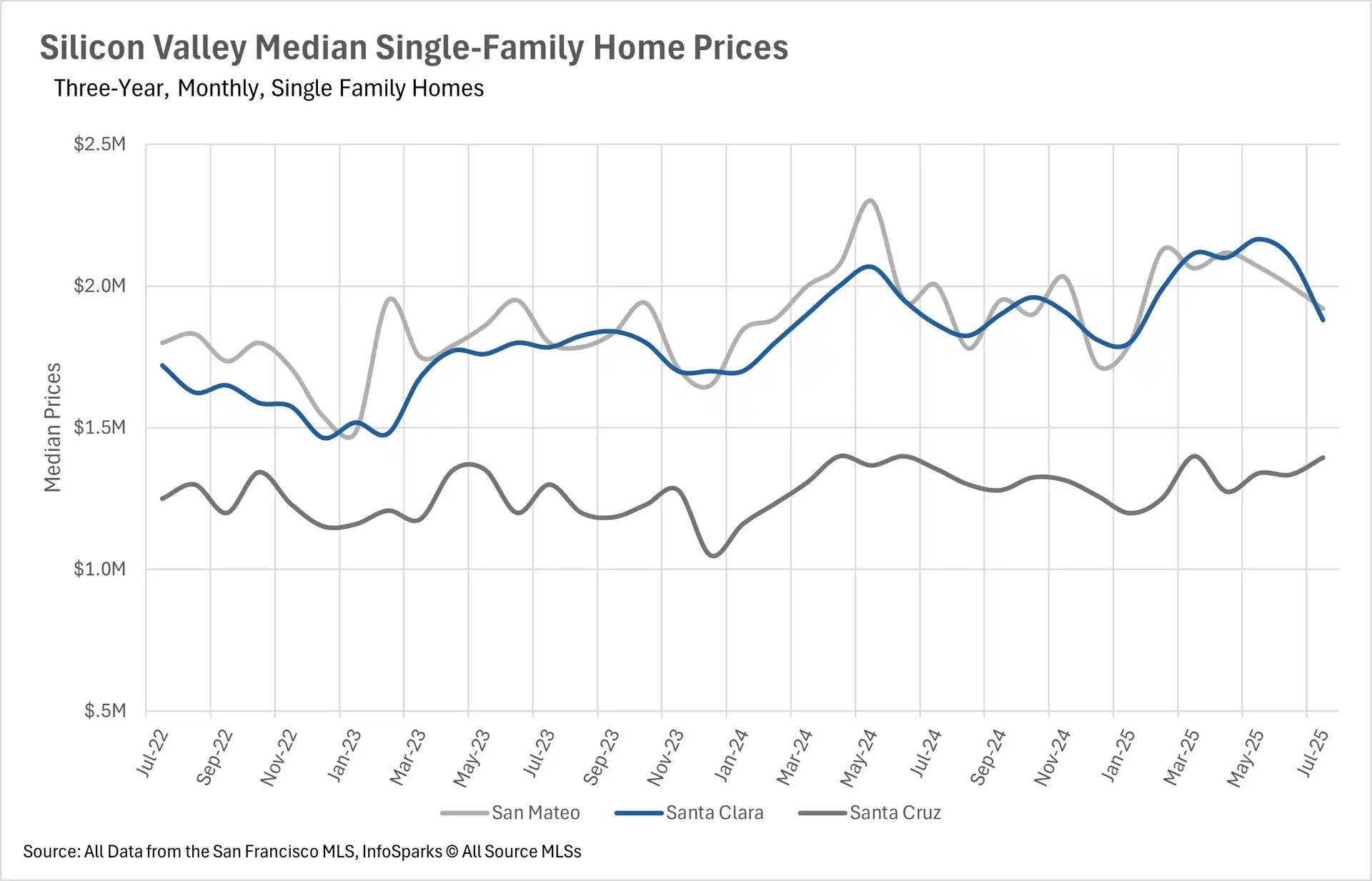

The Bay Area's real estate market is displaying stark regional differences in price performance. Silicon Valley continues to demonstrate remarkable resilience, with Santa Clara County single-family homes maintaining their impressive growth streak for over 12 months without a single year-over-year decline. In contrast, the East Bay has experienced six consecutive months of median sale price decreases, with single-family homes down 2.08% and 6.56% year-over-year in Alameda and Contra Costa Counties respectively. San Francisco and the North Bay fall somewhere in between, with San Francisco single-family homes up 2.34% year-over-year and relatively stable conditions across most North Bay counties, though Napa County stands out with a notable 14.94% decline in single-family home prices.

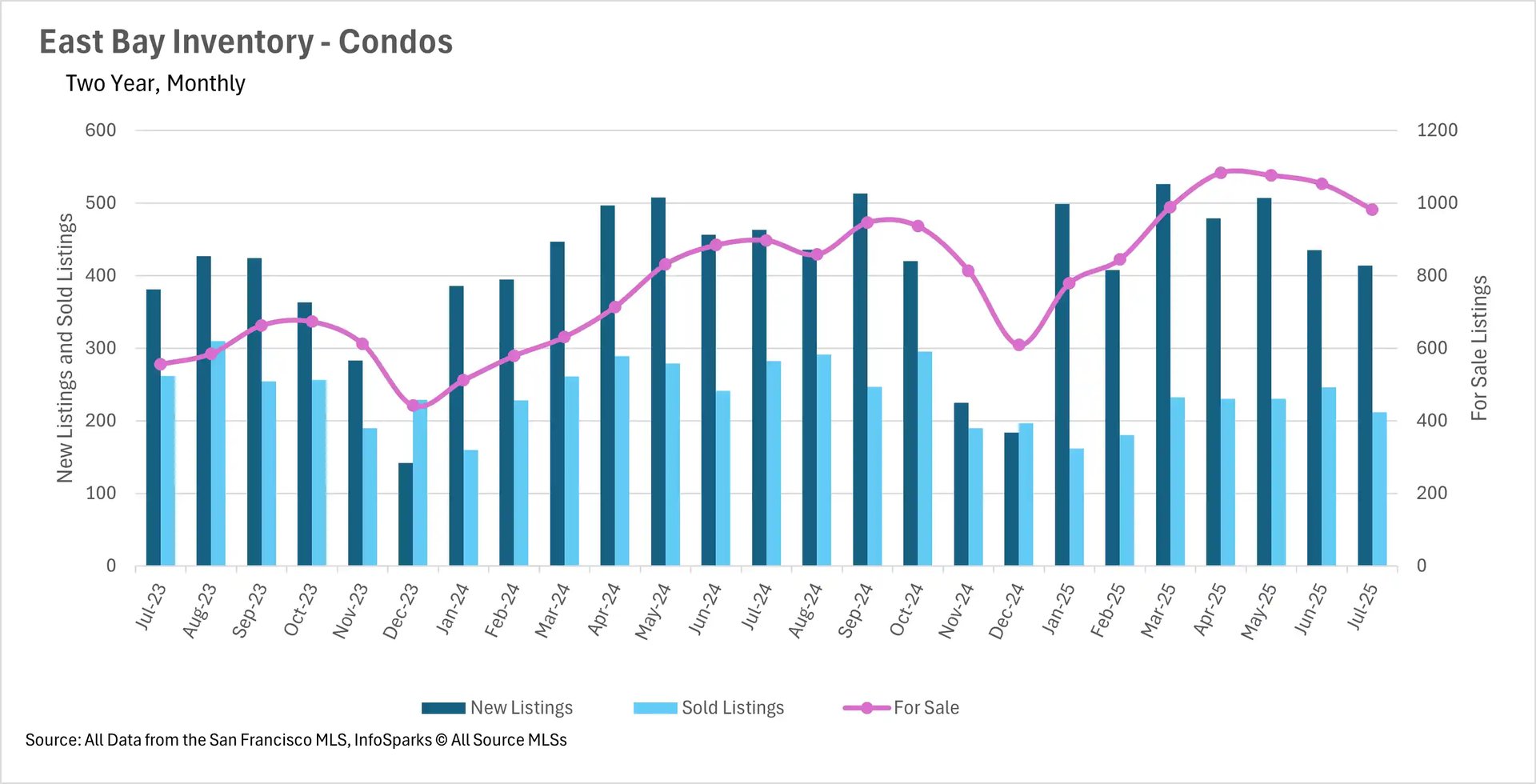

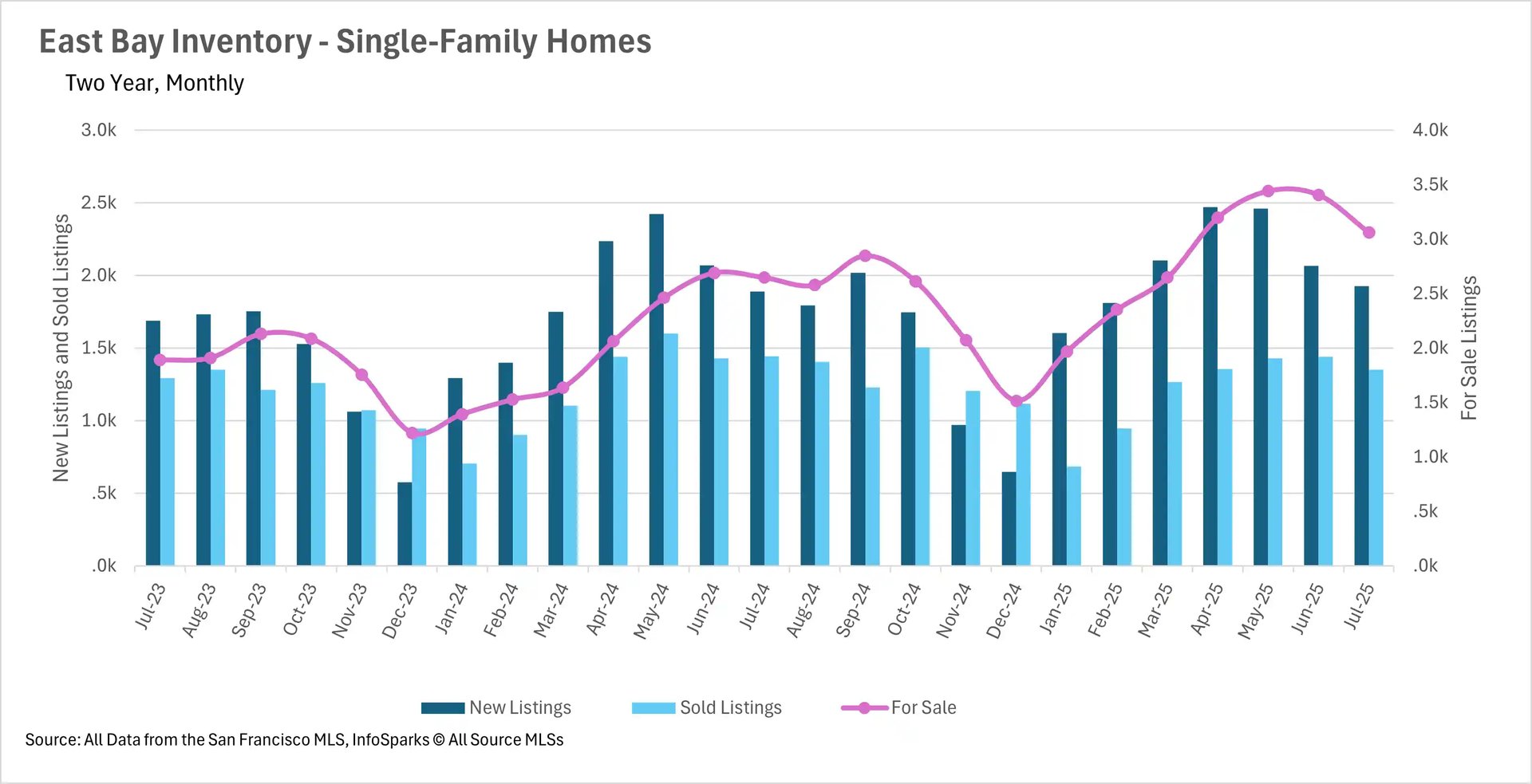

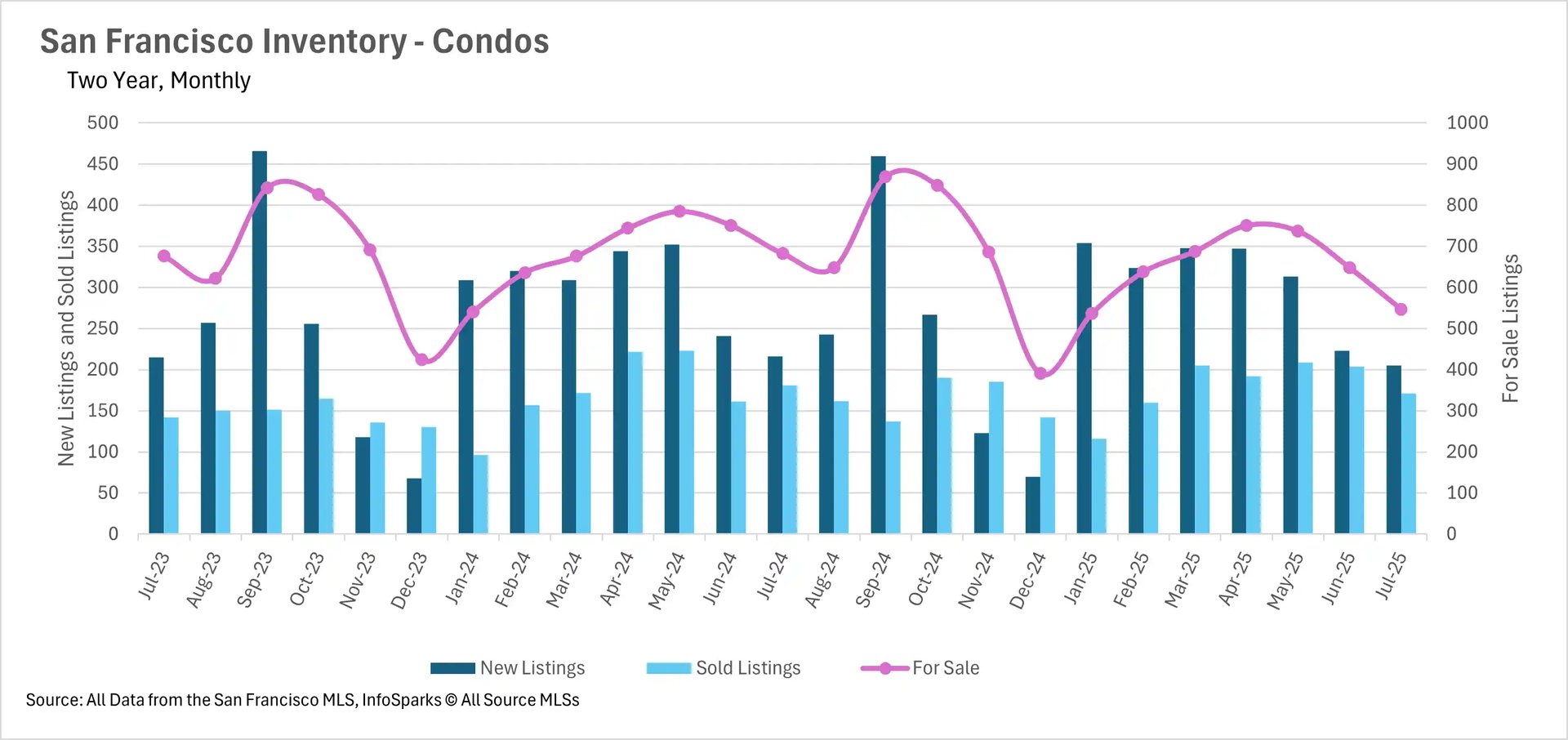

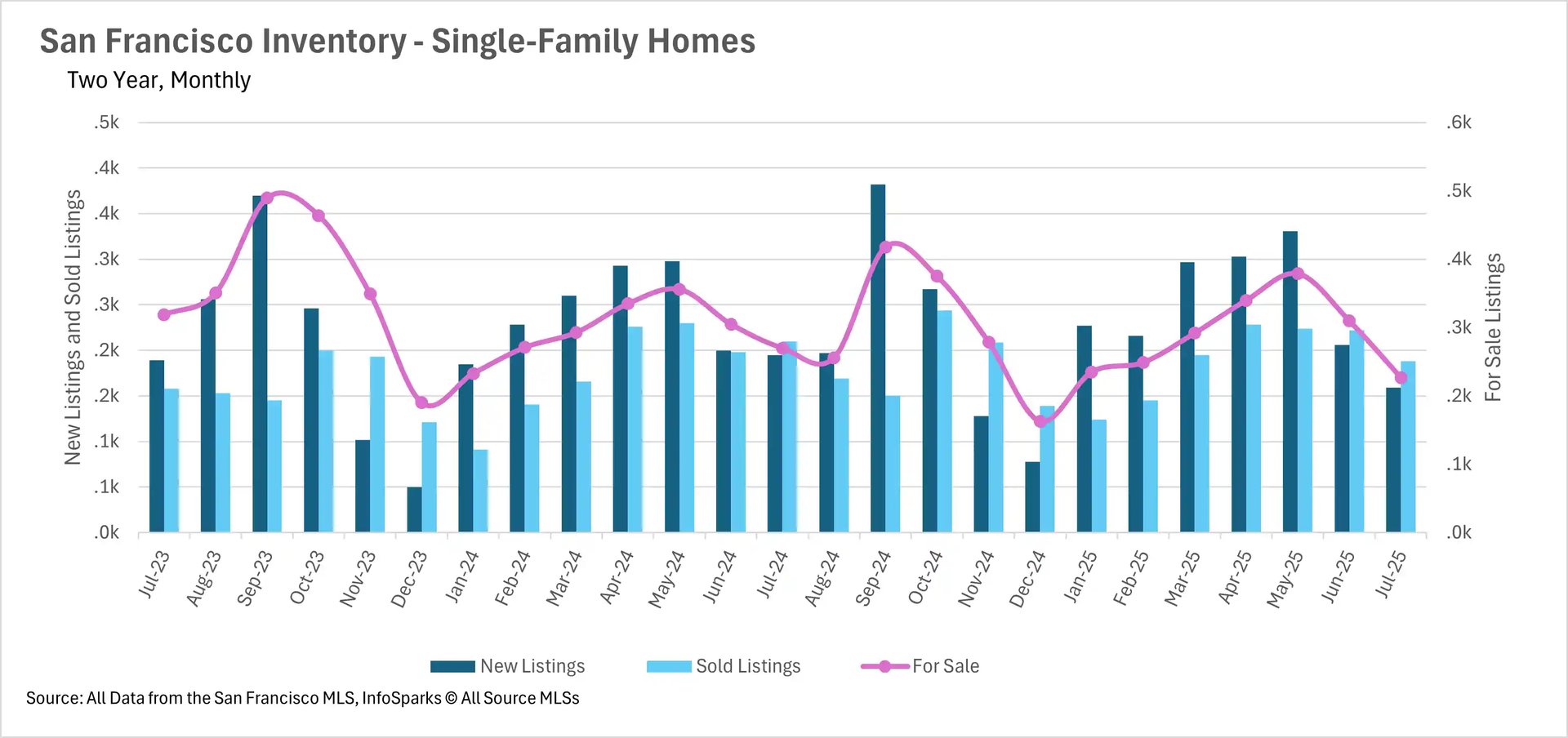

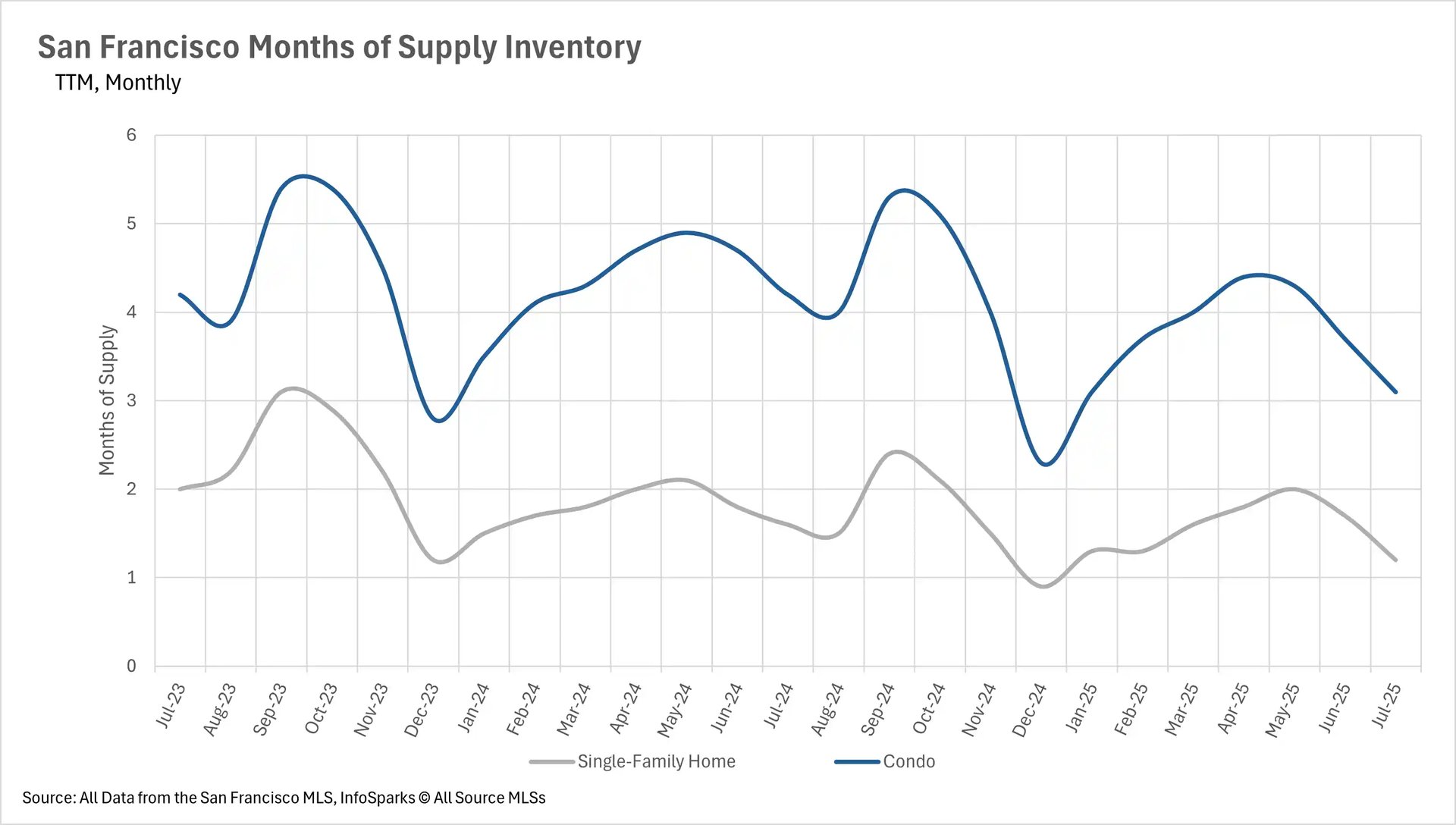

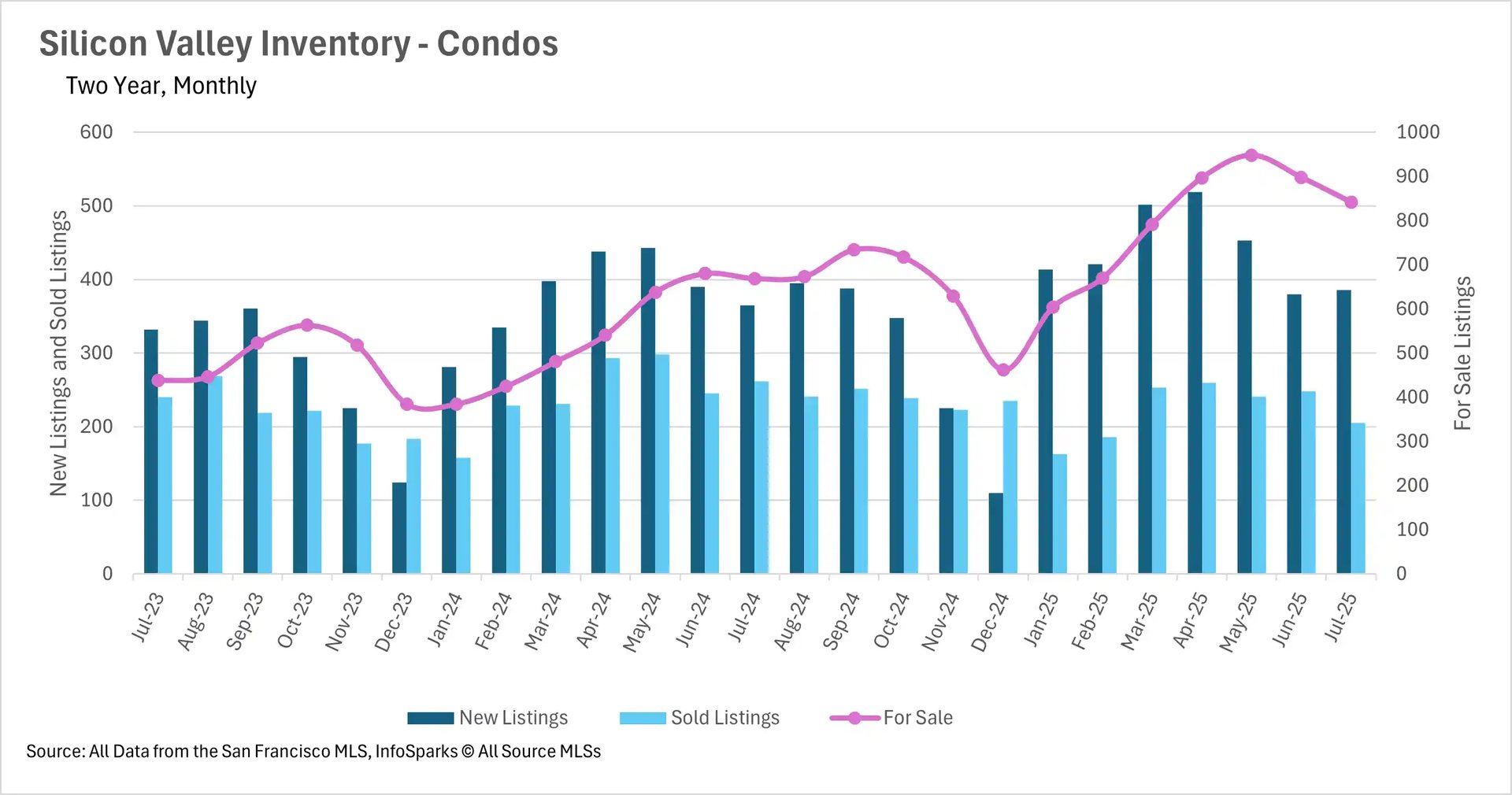

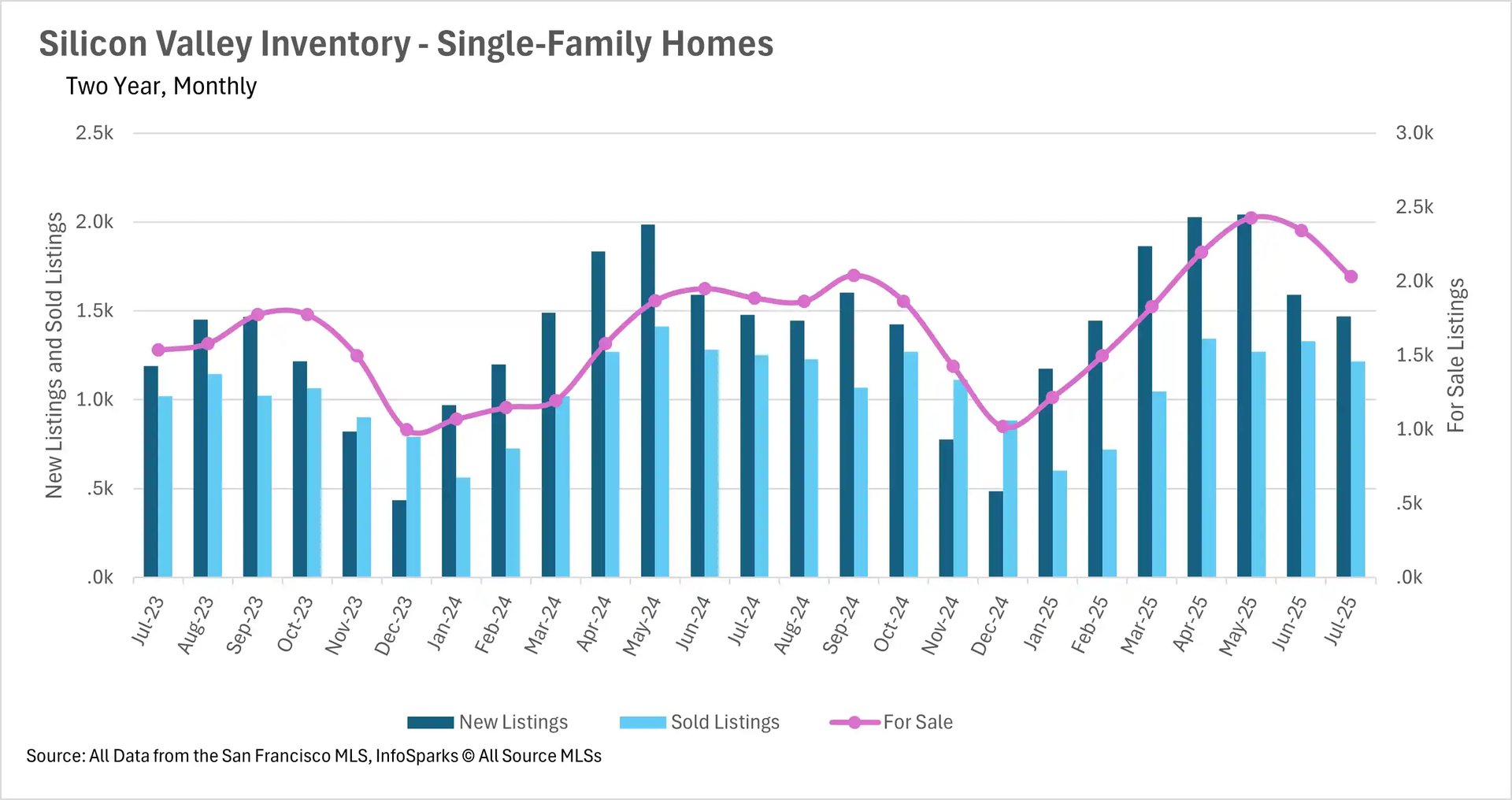

Inventory shortages persist in San Francisco while most regions see supply increases

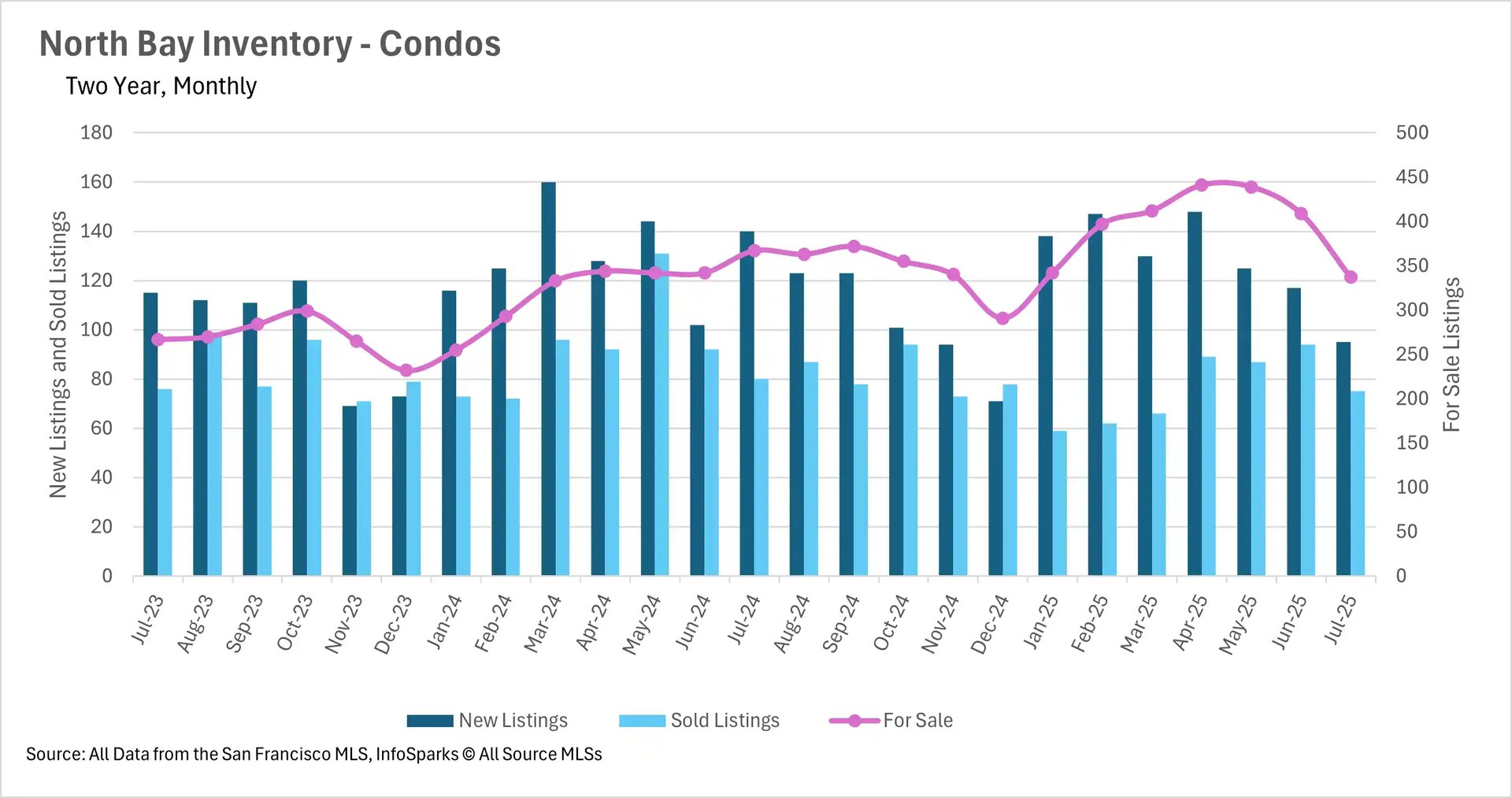

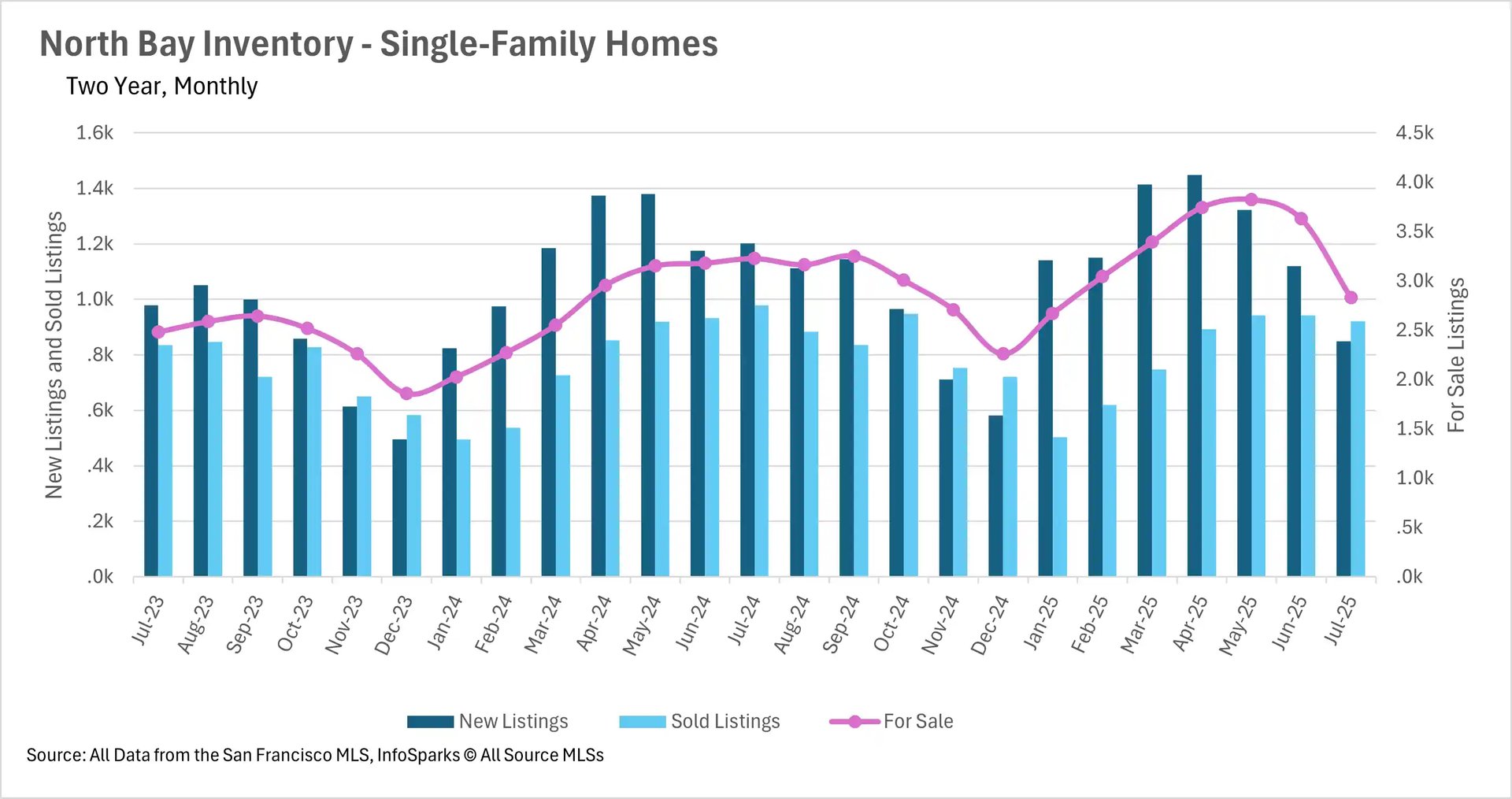

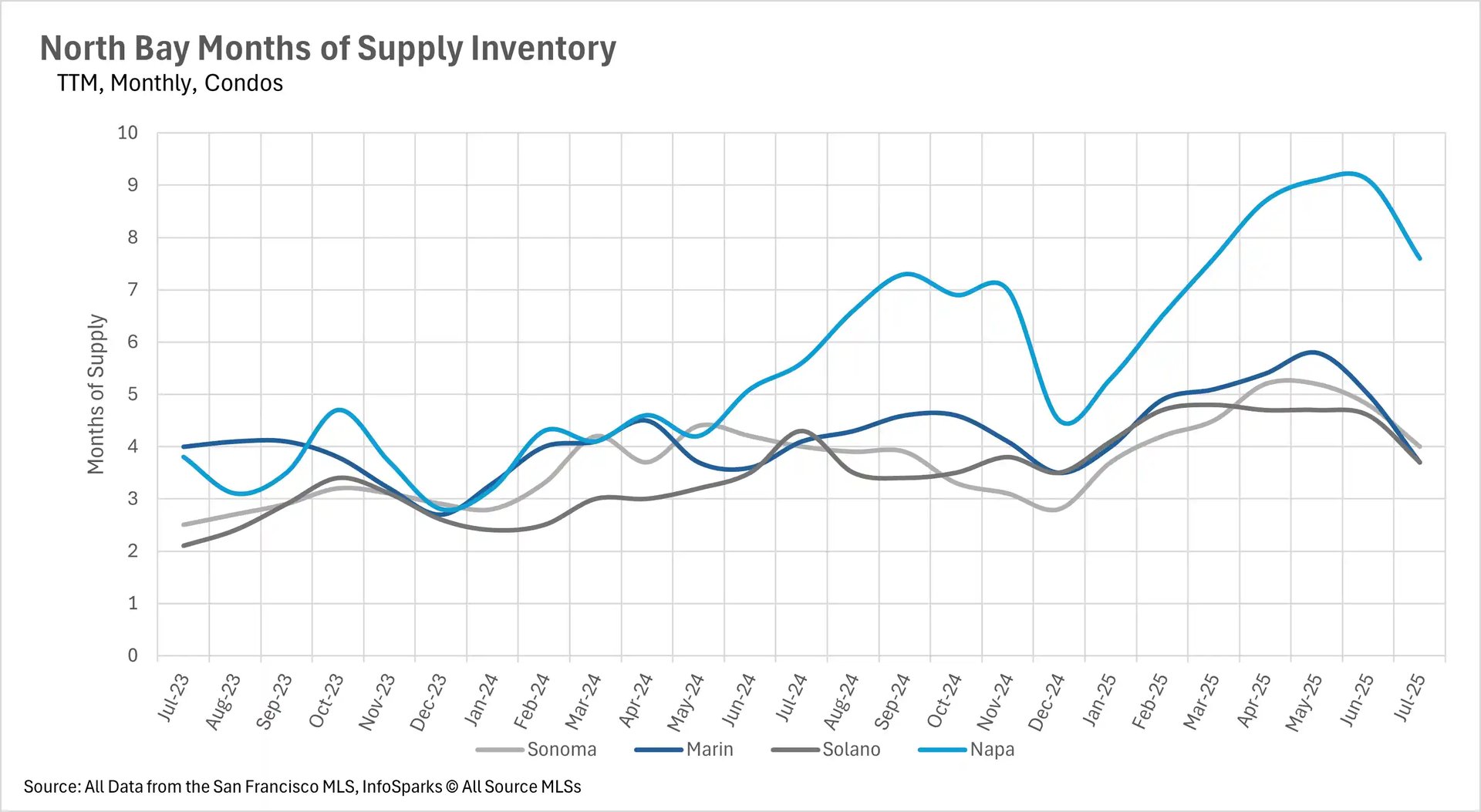

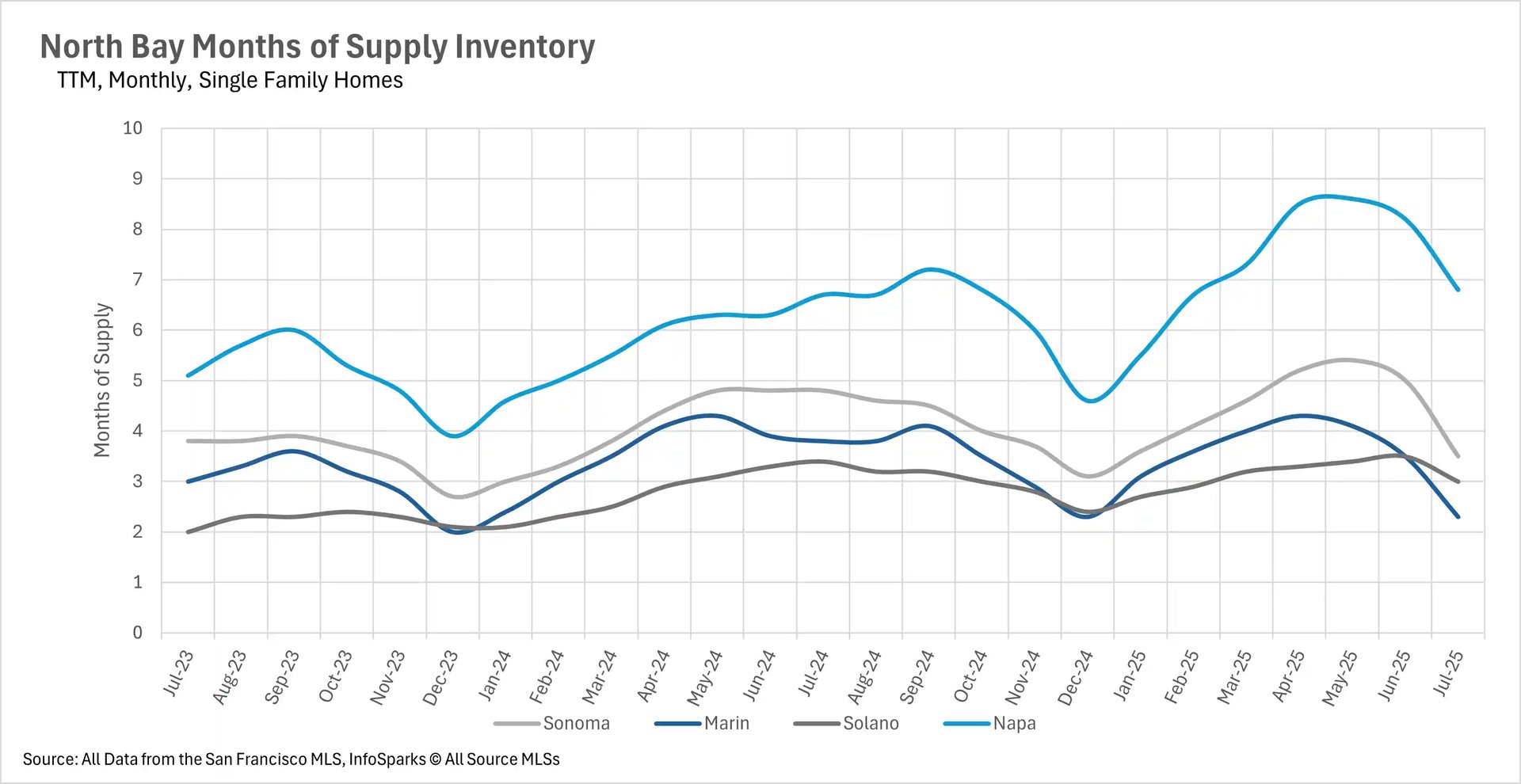

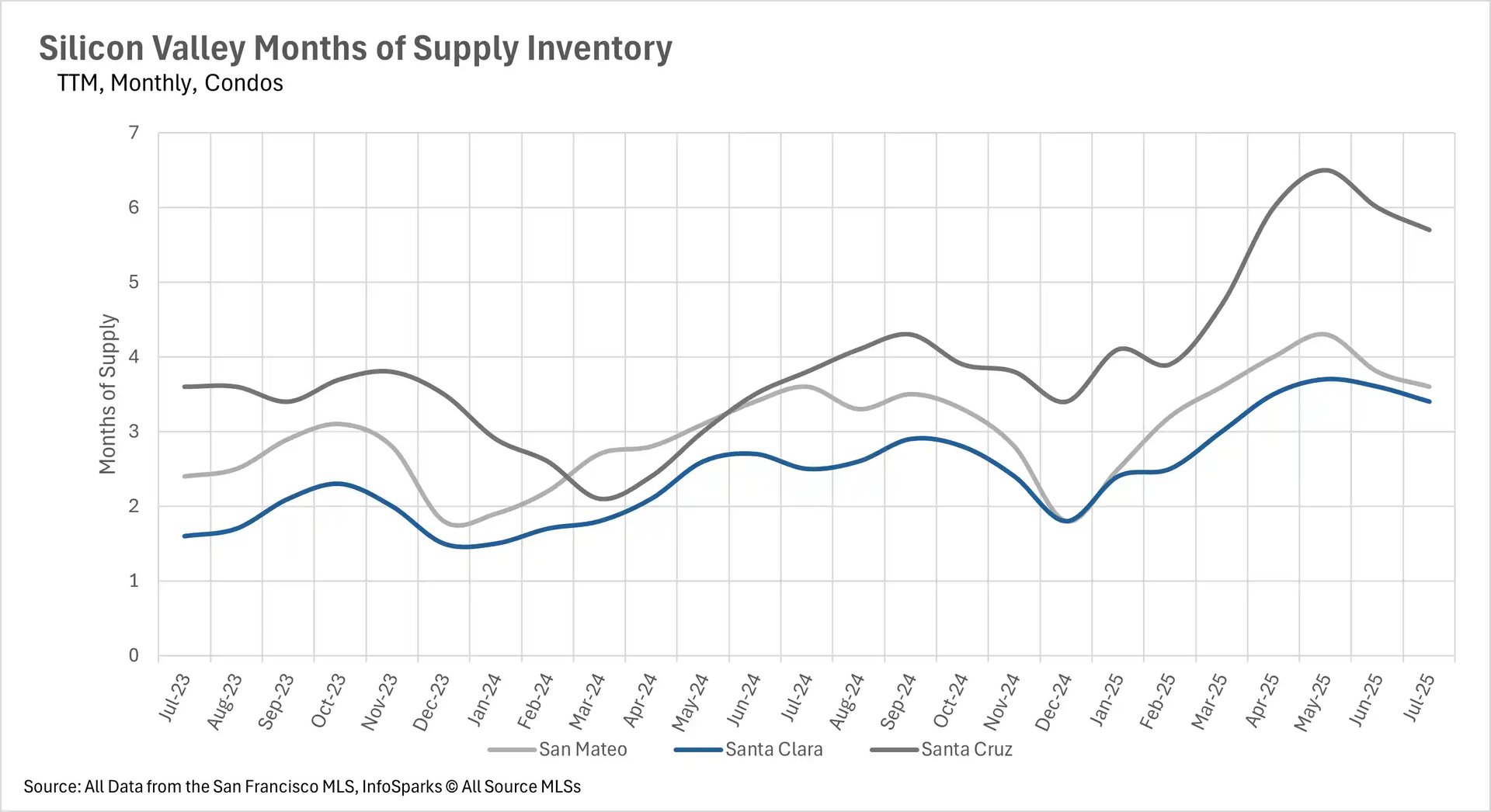

San Francisco's inventory crisis continues to deepen, with 15.93% less single-family inventory and 19.91% fewer condos available compared to last year. This stands in sharp contrast to Silicon Valley, where inventories have grown 7.63% for single-family homes and 25.86% for condos year-over-year. The East Bay is experiencing similar inventory growth with a 15.68% increase in active single-family listings, while the North Bay has seen dramatic month-over-month inventory drops of 21.98% for single-family homes, largely attributed to record-low levels of new listings in July.

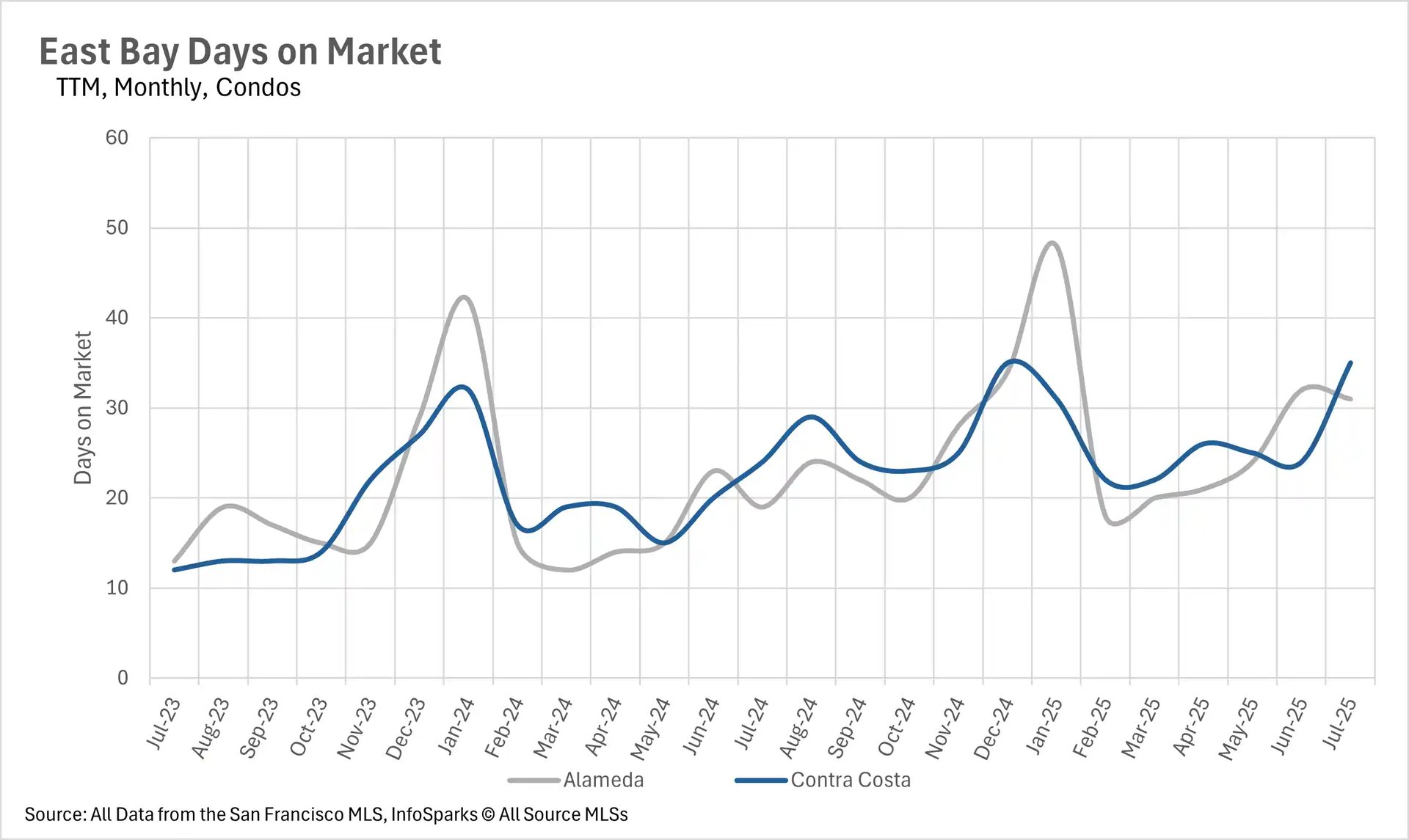

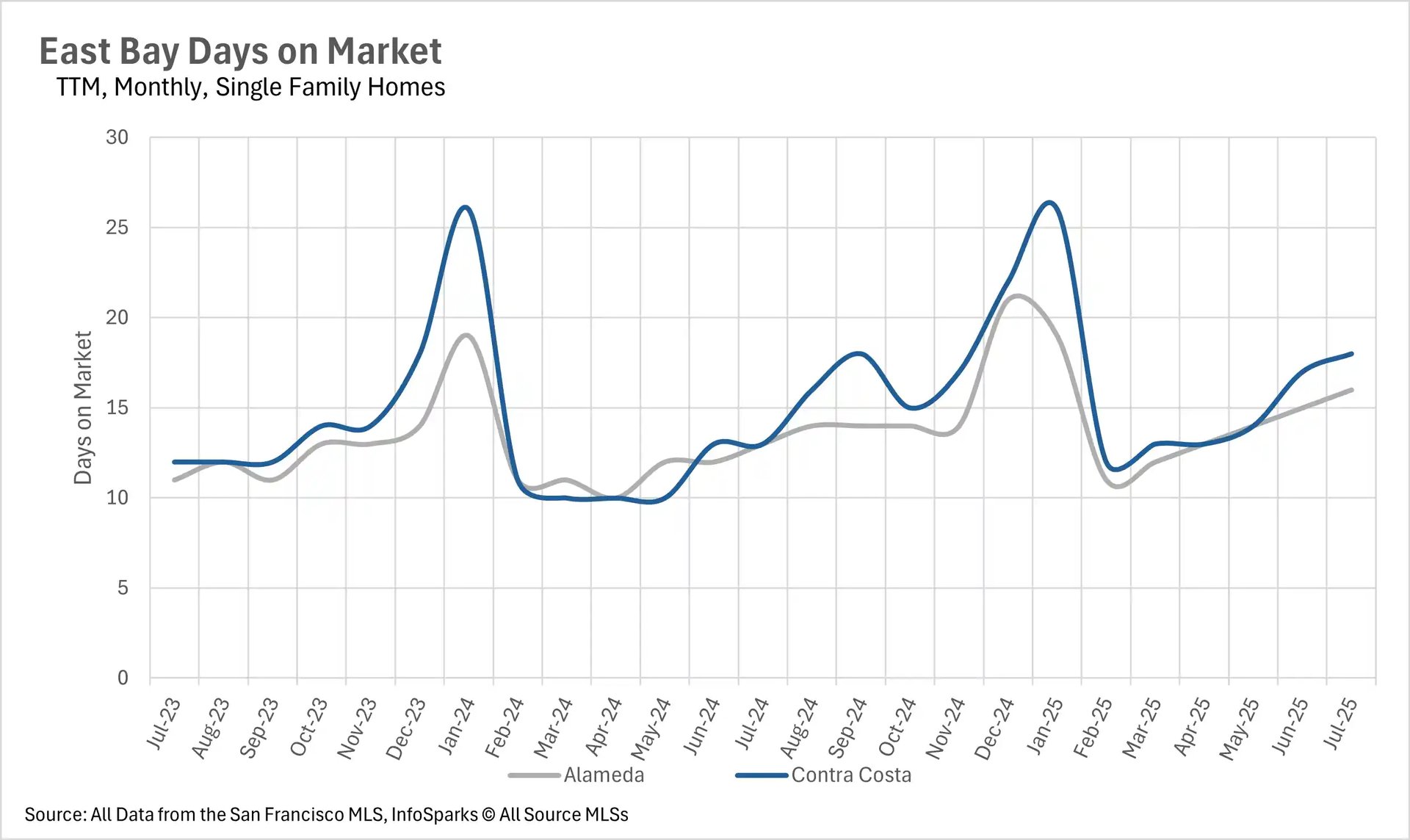

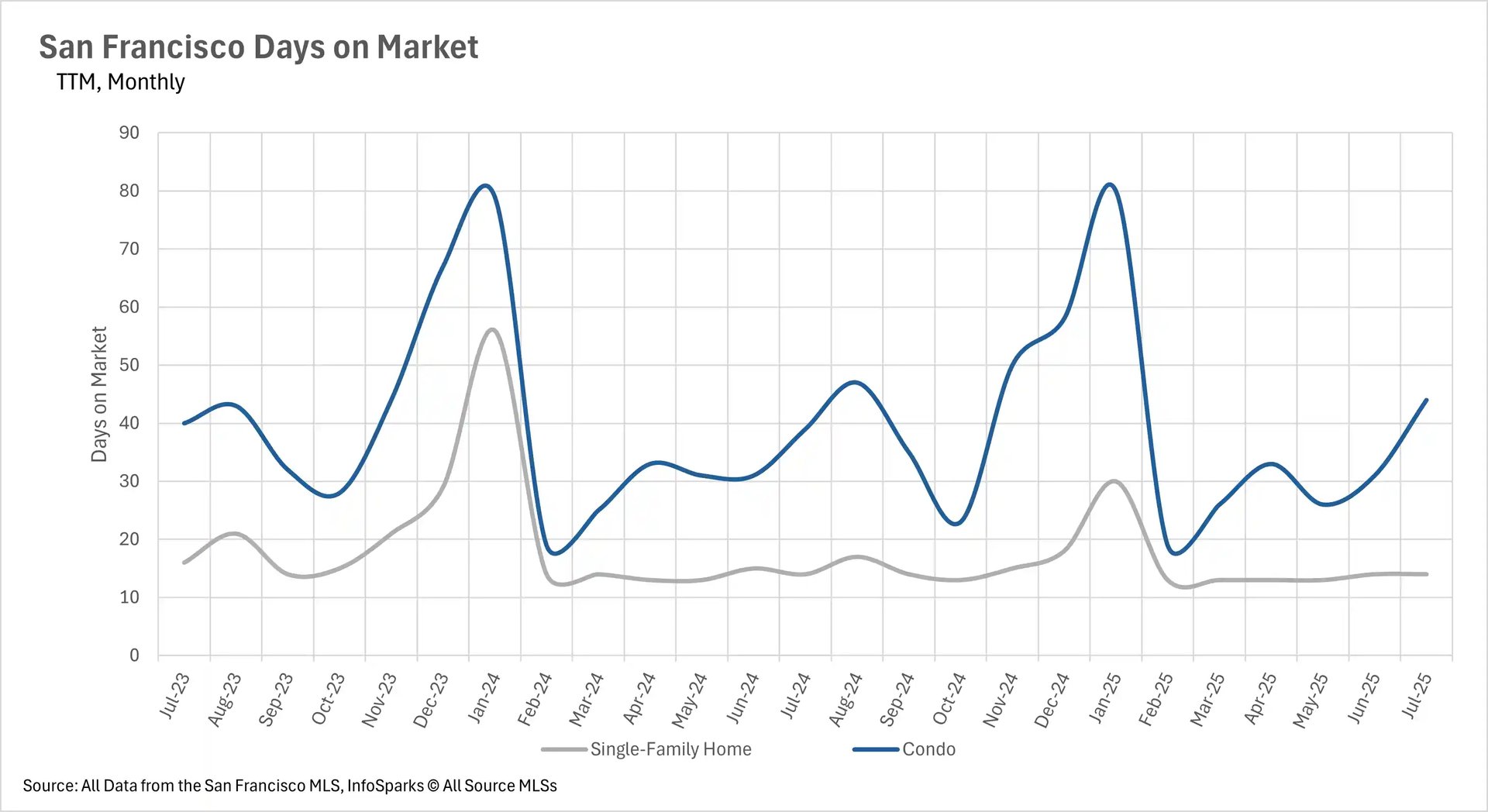

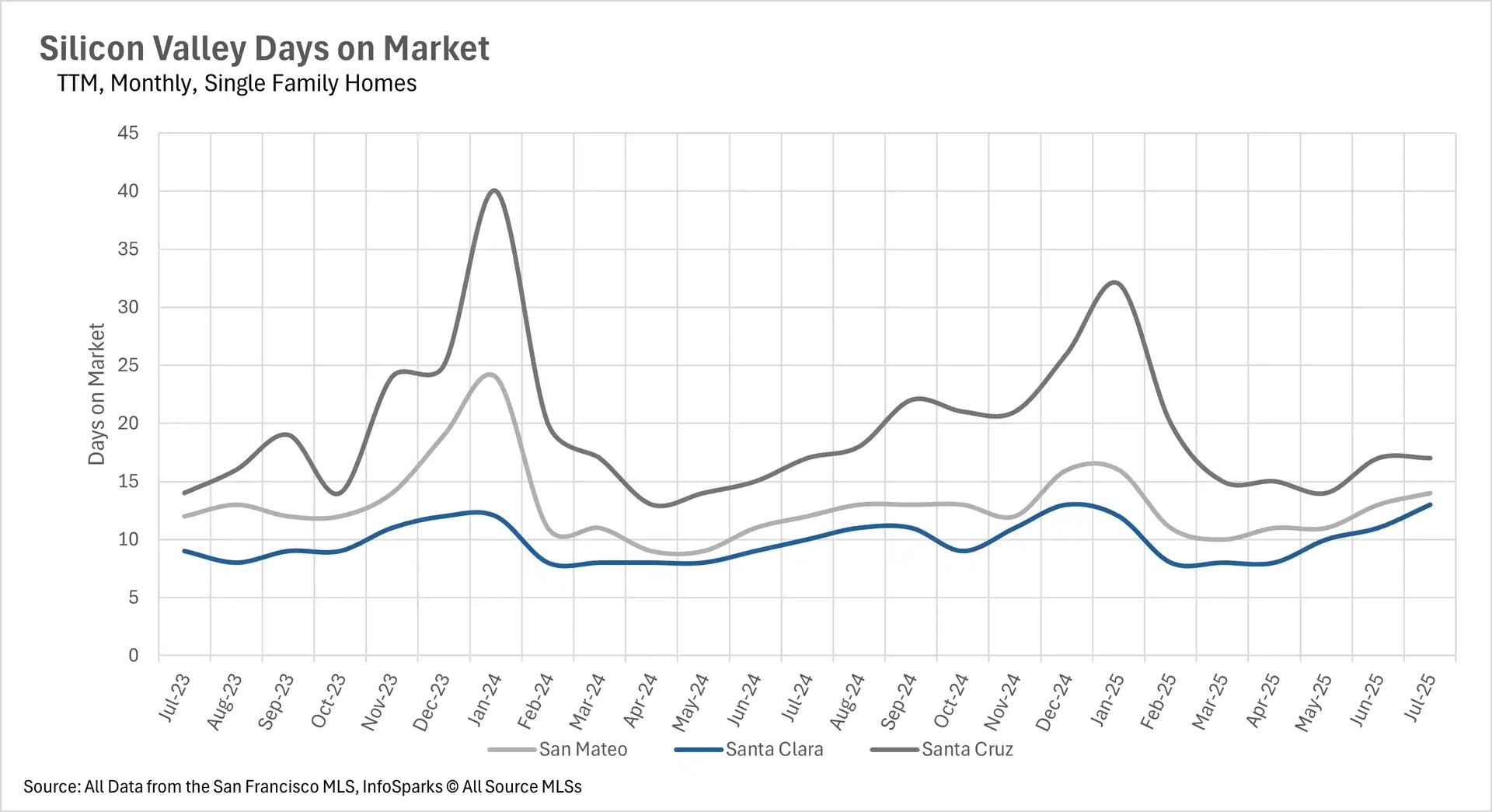

Extended time on market becomes the new normal across regions

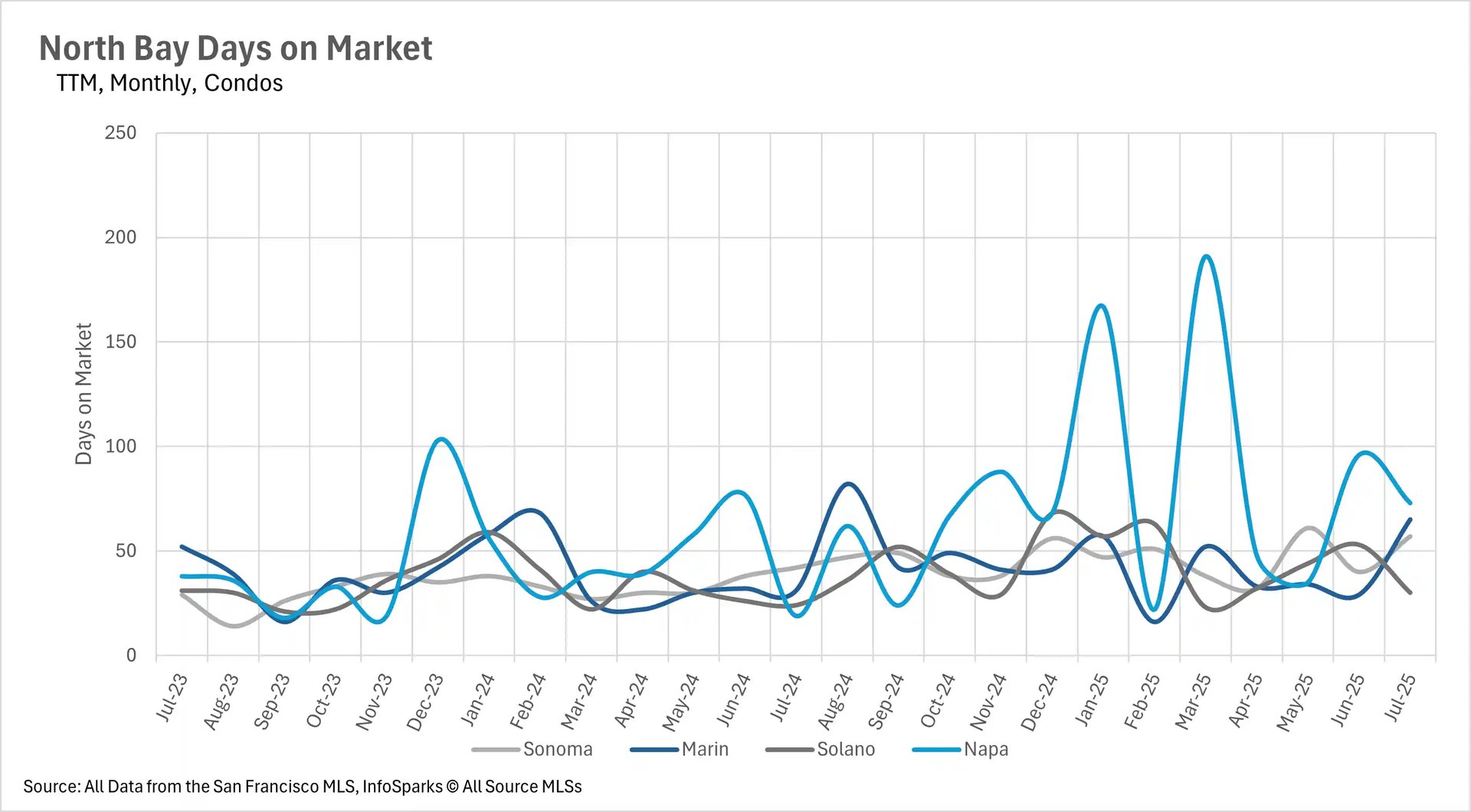

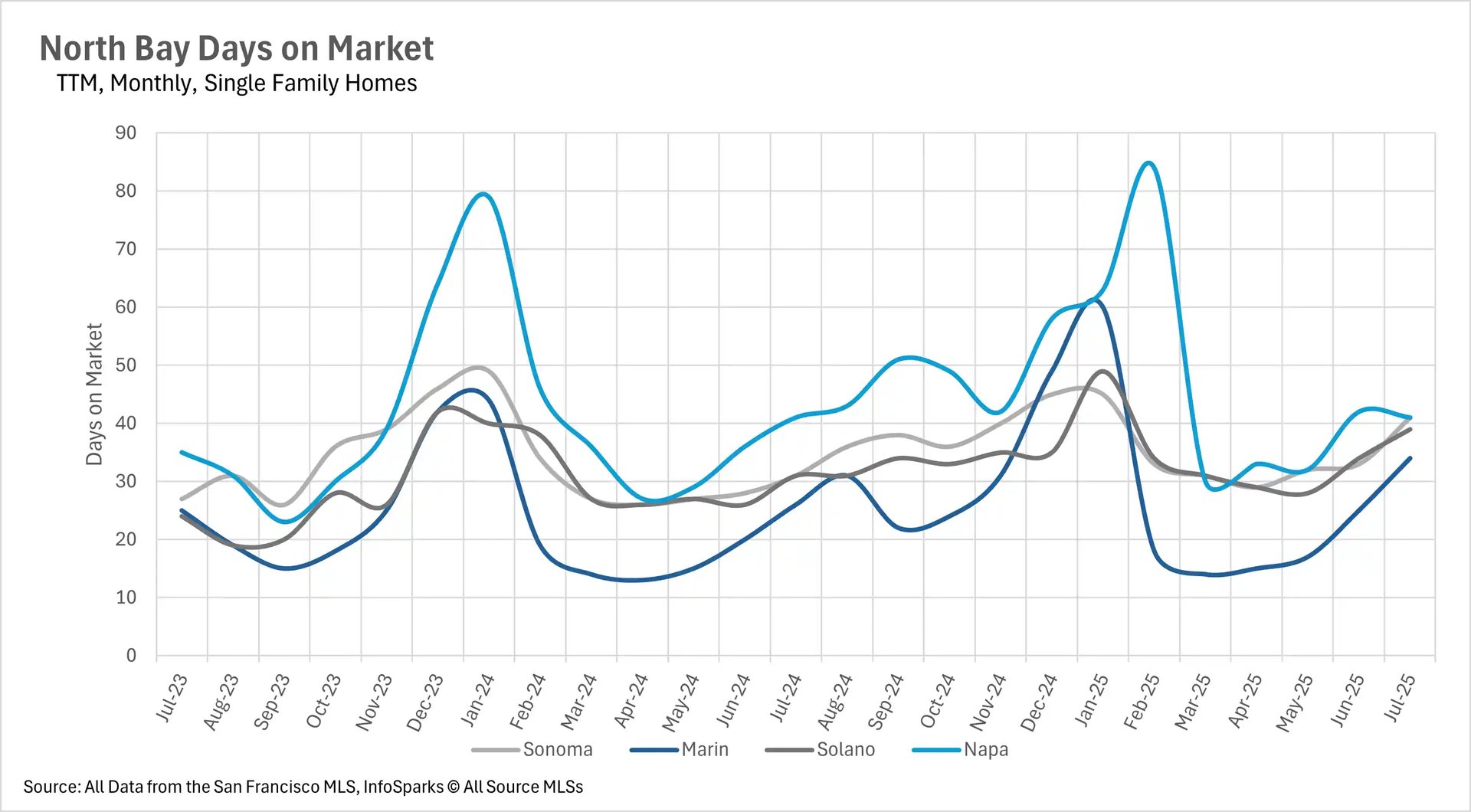

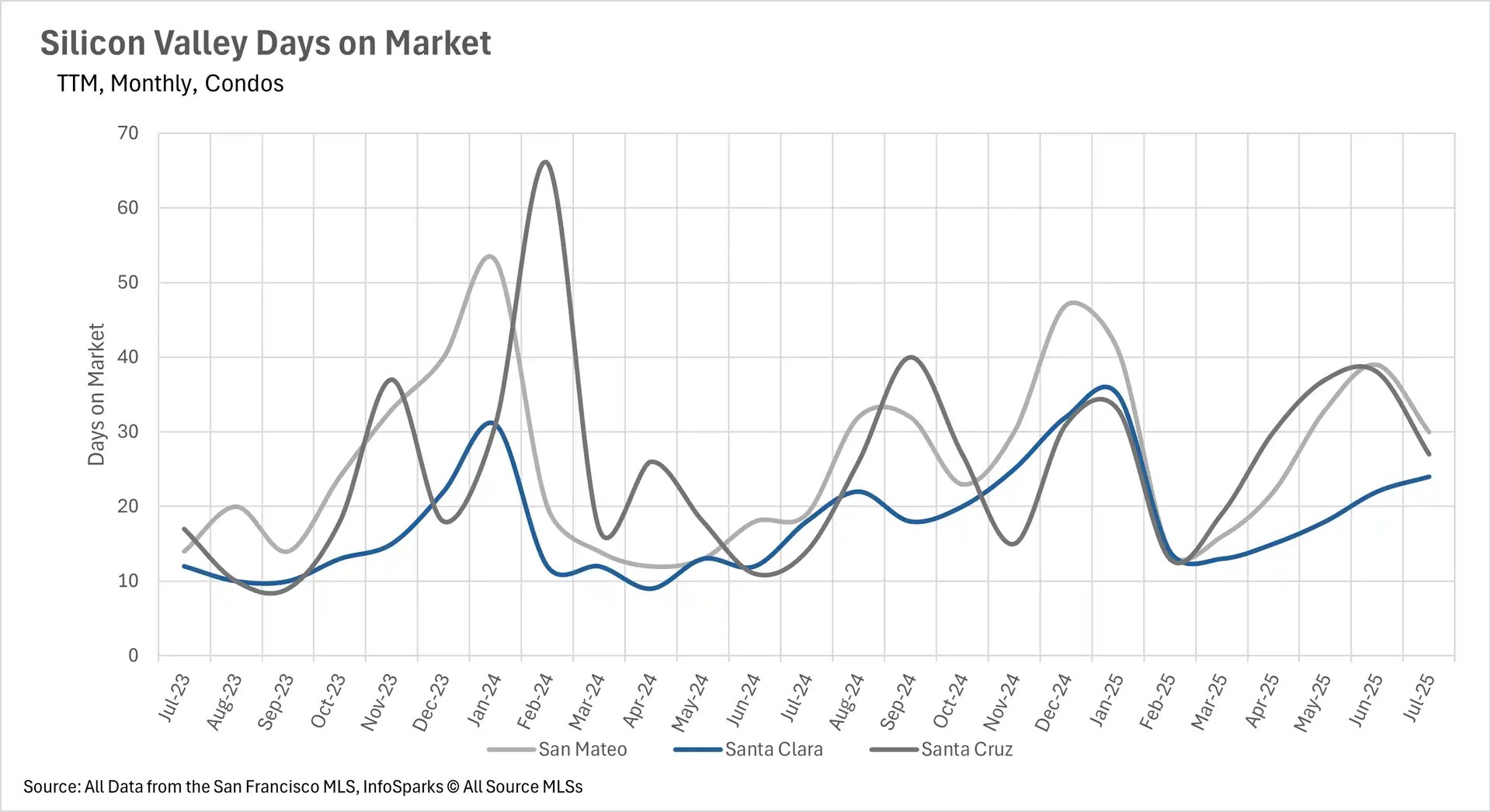

Despite varying inventory conditions, one consistent trend emerges across the Bay Area: homes are taking longer to sell. The East Bay has seen particularly dramatic increases, with single-family homes now spending 16-18 days on market compared to 13 days last year, while condos are taking 31-35 days versus 19-24 days in 2024. Silicon Valley homes are still selling quickly at under 2.5 weeks, but even this represents an increase from last year. The North Bay is experiencing 20-30% longer listing periods in most markets, with some areas like Marin and Napa County condos seeing dramatic increases of 109.68% and 284.21% respectively.

Market dynamics shift toward more balanced conditions

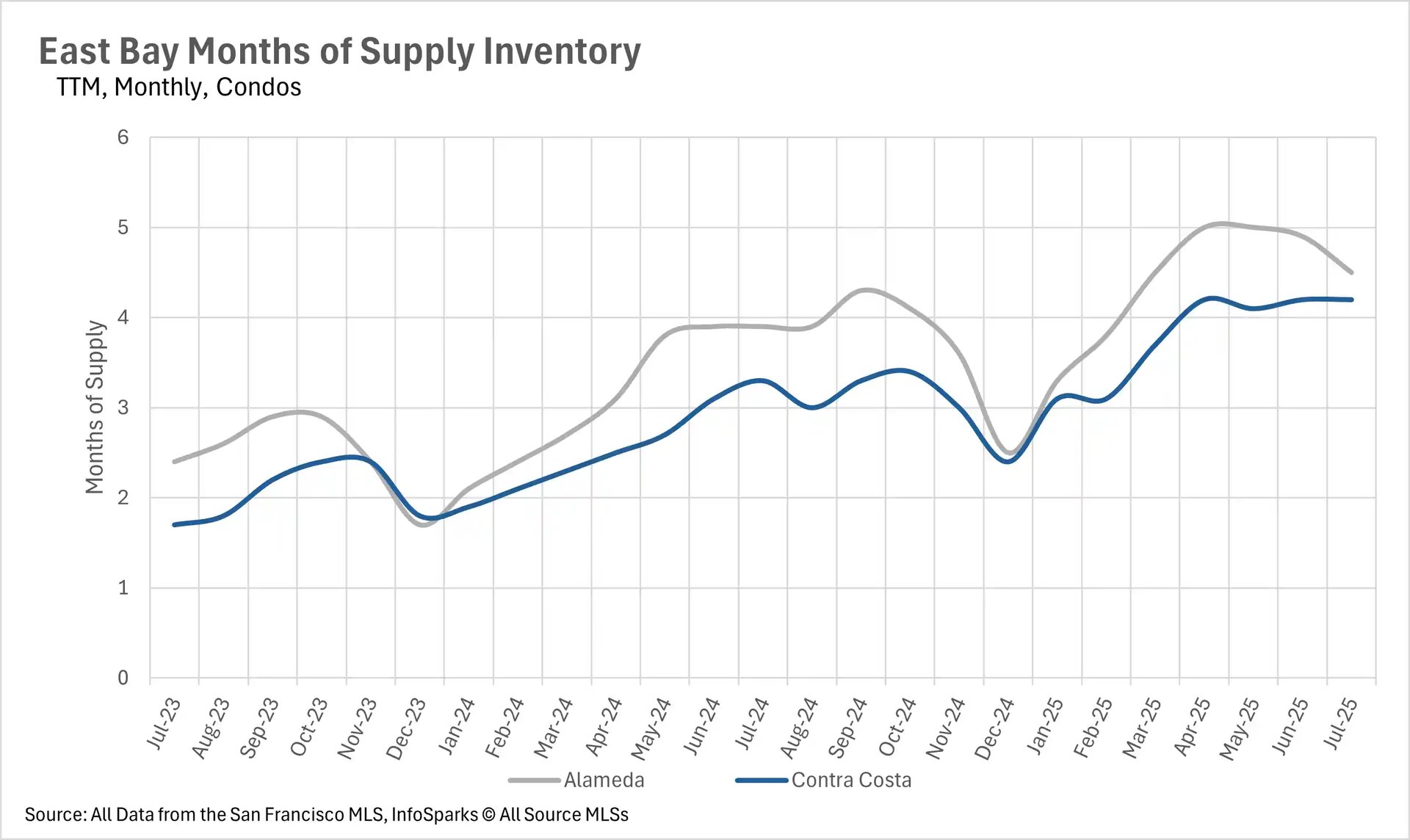

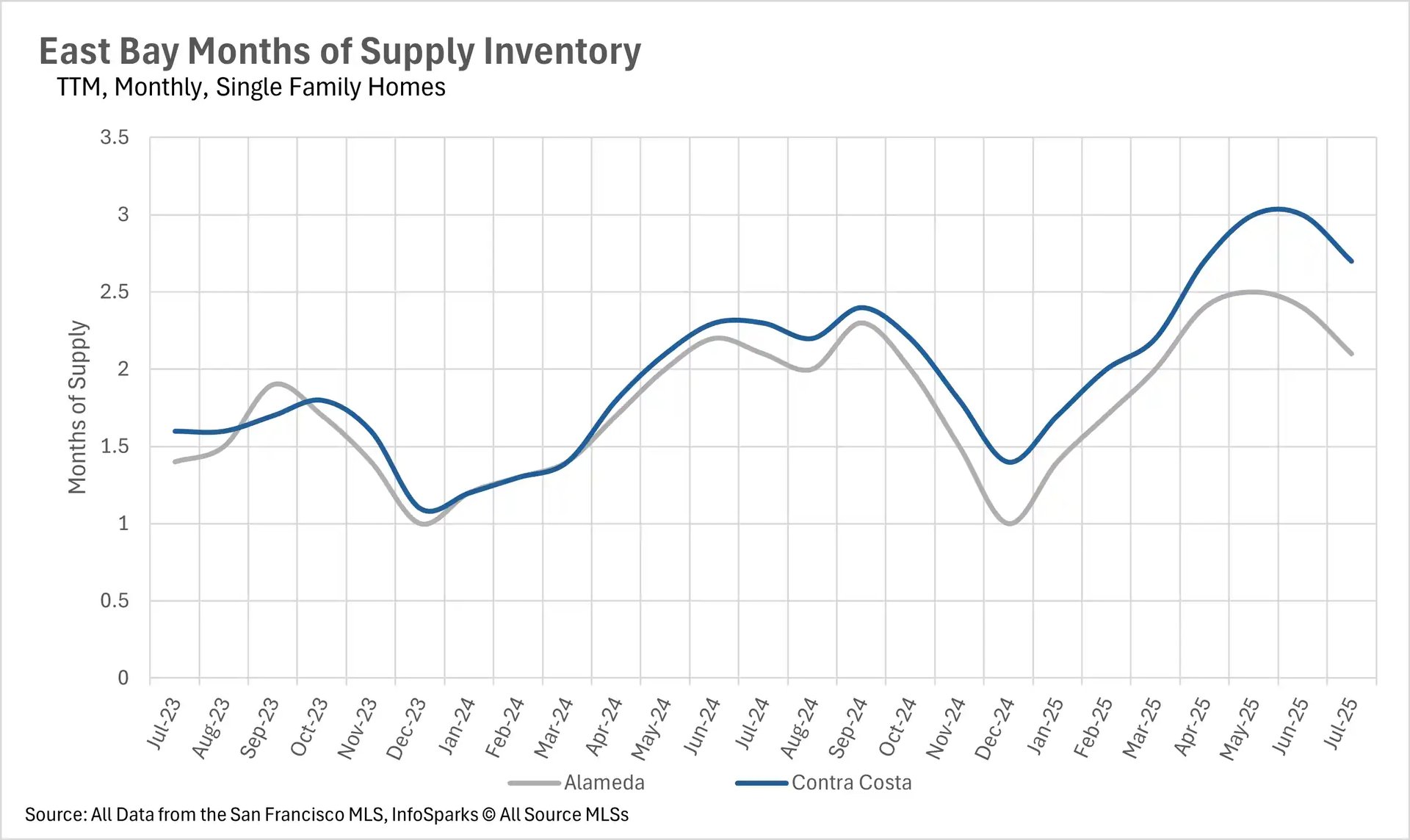

The changing inventory and pricing dynamics are reshaping market competitiveness across the Bay Area. San Mateo and Santa Clara Counties remain fiercely competitive sellers' markets with just 1.7 and 1.5 months of supply respectively. However, other areas are trending toward more balanced conditions, with Marin County's single-family market flipping to a sellers' market at 2.3 months of supply, while San Francisco's condo market is approaching balance at 3.1 months. The East Bay maintains sellers' market conditions for single-family homes despite falling prices, while condo markets across most regions have shifted to buyer-friendly conditions with 3.4 to 5.7 months of supply available.