Select a Market Report to Read:

The Local Lowdown

Quick Take:

- Median sale prices for condos continue to lag where they were last year.

- Inventories are surprisingly static on a year-over-year basis

- Listings are spending a lot more time on the market than they were last year.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

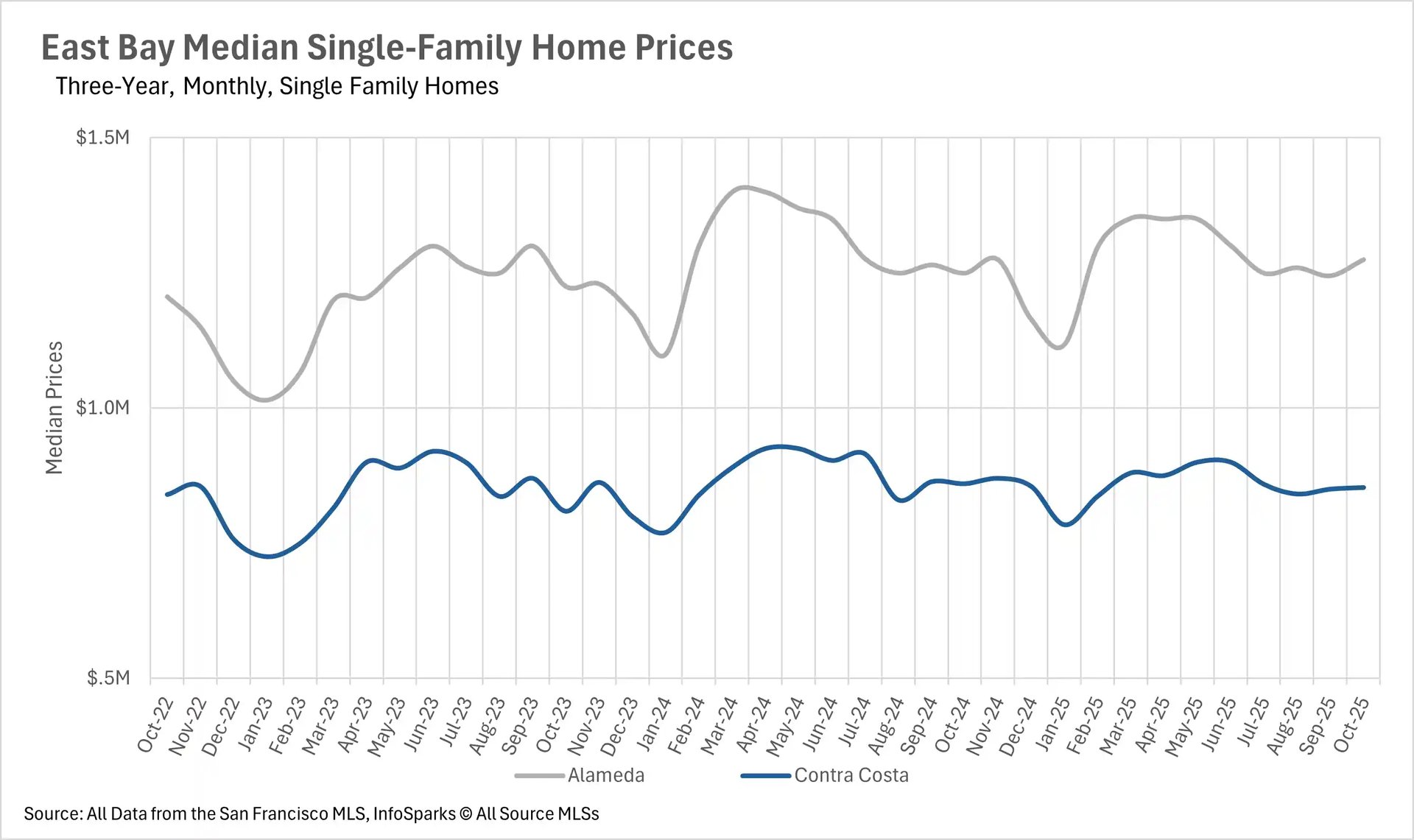

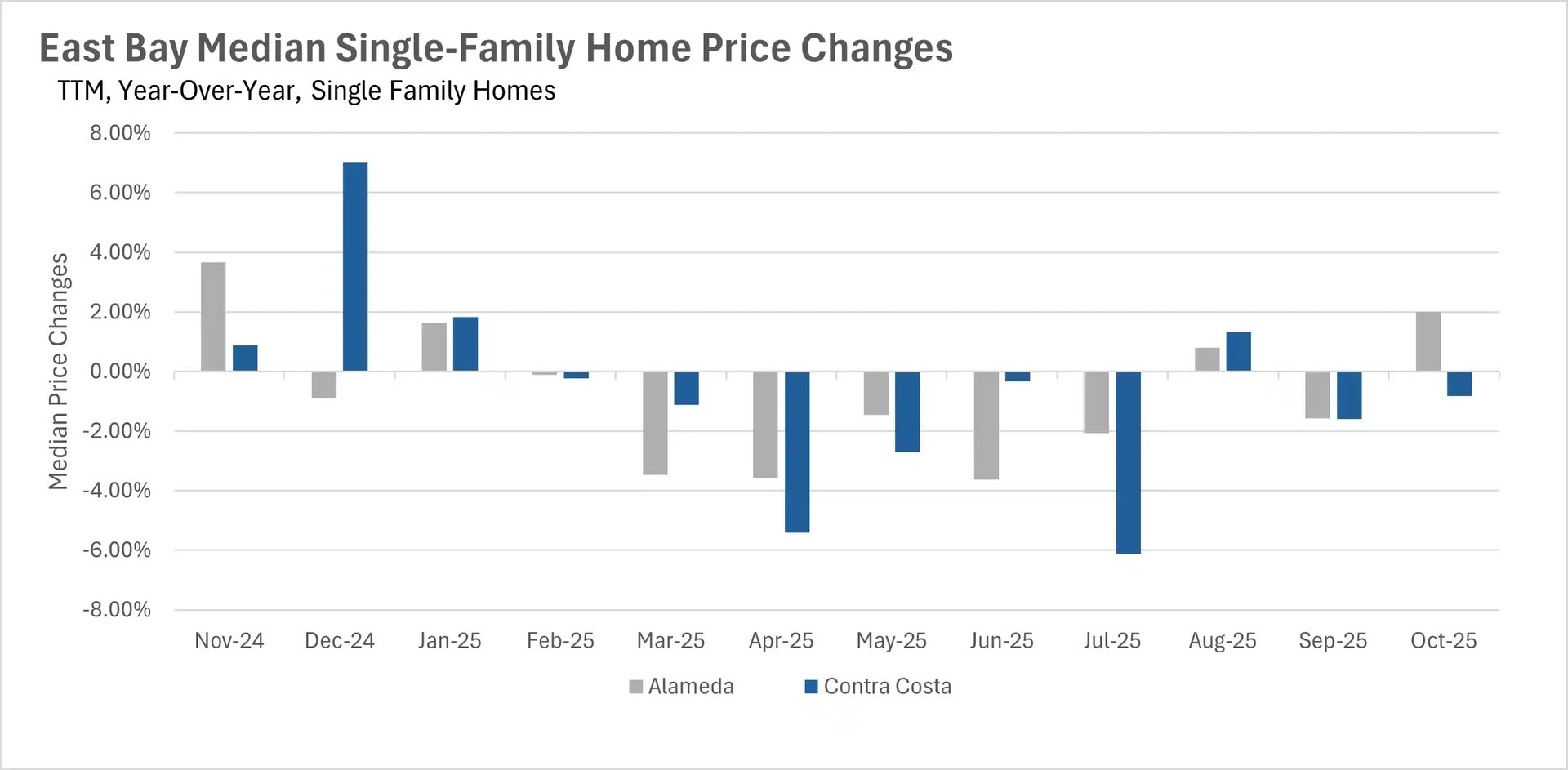

Little change in single-family home pricing, but condos continue to lag

There was very little change in the single-family home market in the month of October, with the median sale price increasing by 2.00% in Alameda County, and decreasing by 0.81% in Contra Costa County. However, there were some movements in the condo market. This month, the condo market extended its losing streak, as the median condo in Alameda County sold for 9.38% less than it did last year, and the median condo in Contra Costa County sold for 7.69% less than last year. Although these are drastic year-over-year decreases, the market is overall fairly stable, with homes holding their value in the band they’ve created for themselves over the past 8-10 months.

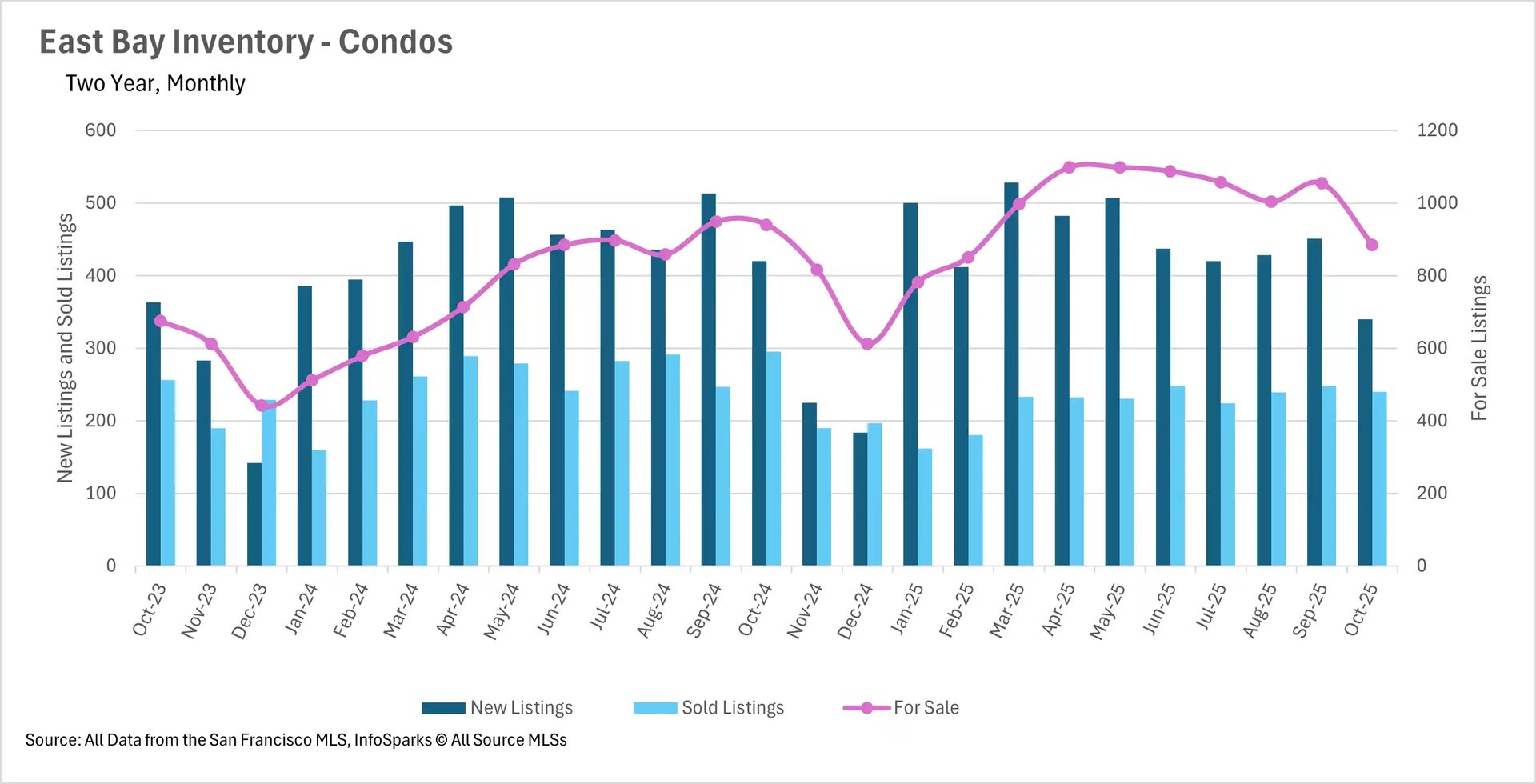

Some interesting developments in condo market inventory levels

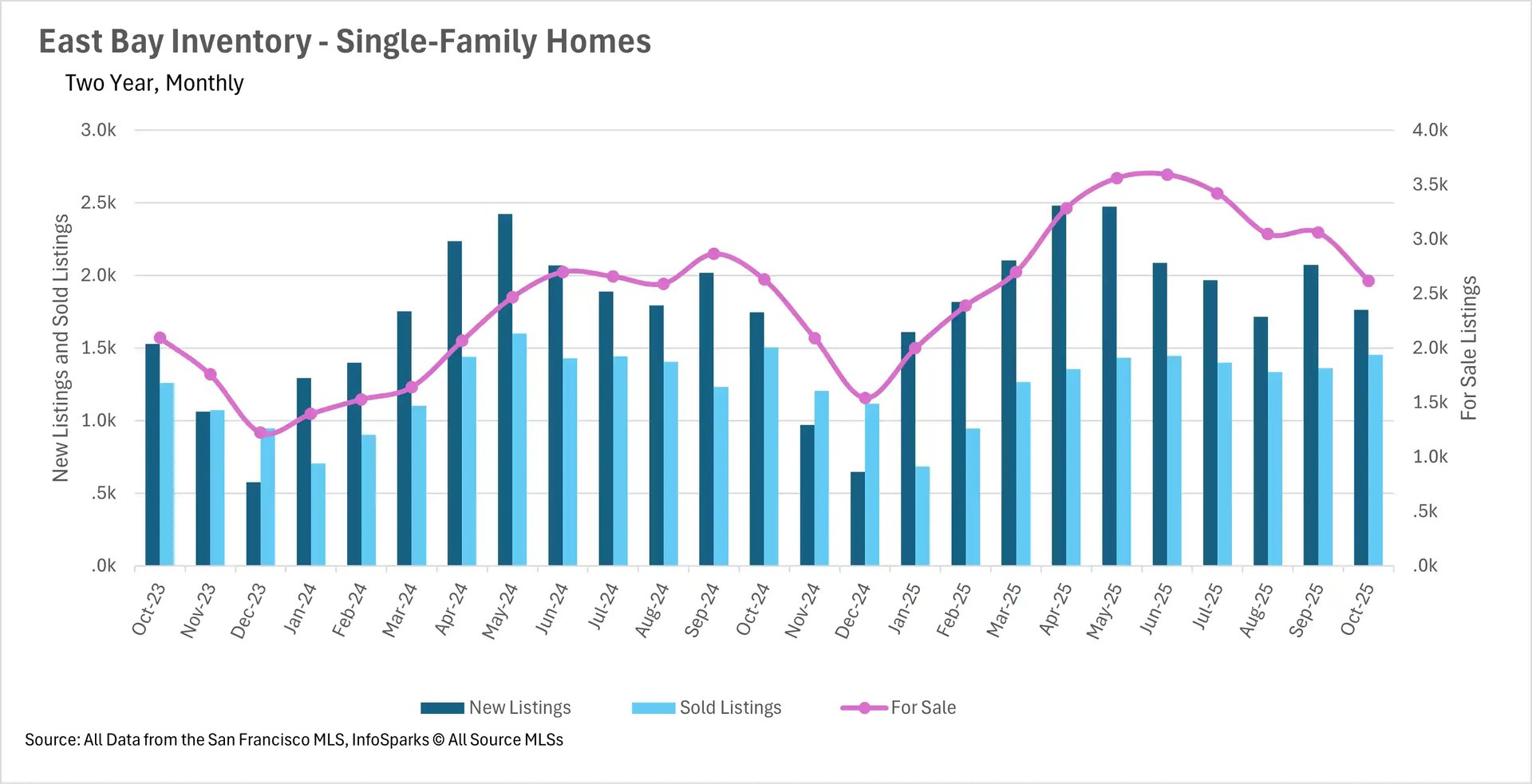

Once again, things were more or less business as usual in the single-family home market this month. However, the condo market saw some interesting developments in terms of inventory levels. In the month of October, we saw 19.05% fewer condos listed, and 18.64% fewer condos sold. Active inventory also decreased by 5.85% on a year-over-year basis. It’ll be important to pay attention to how this market evolves over the seasonally slow winter months, as dwindling inventories might drive prices up over time.

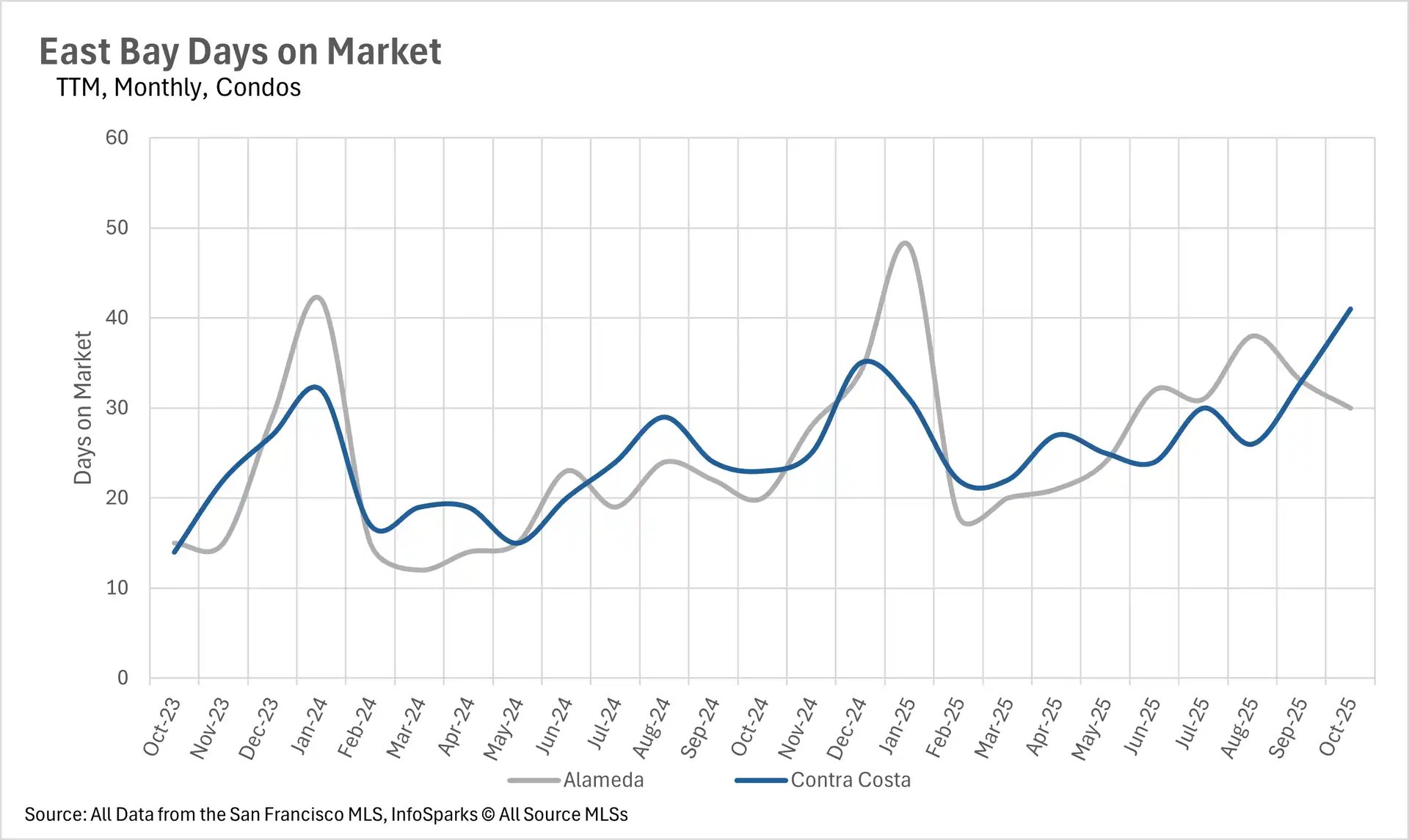

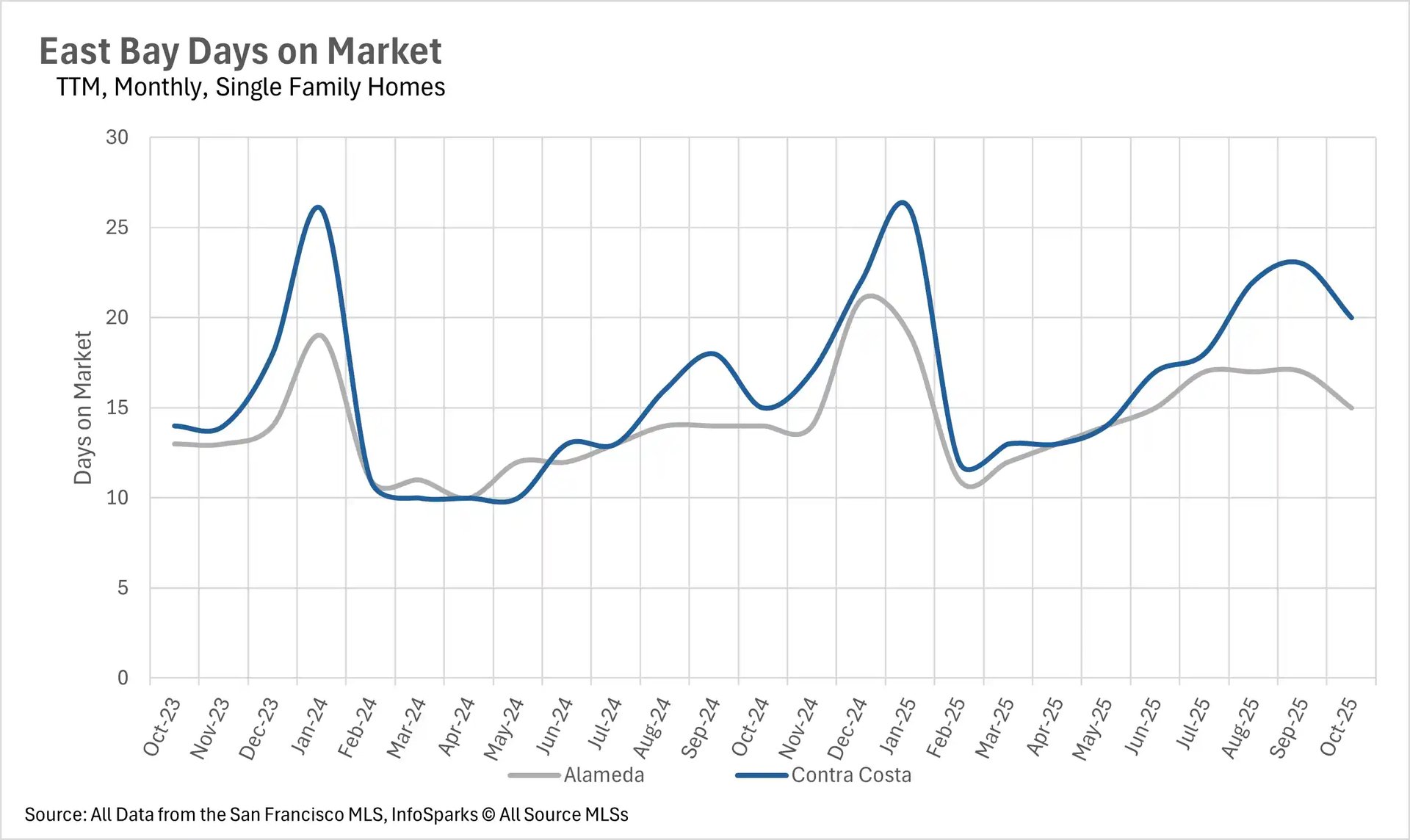

Listings are sitting for quite a bit longer than they did last year

In both the single-family and condo markets, listings are sitting on the market for quite a bit longer than they did around this time last year. The average single-family home in Alameda County saw a 7.14% increase in days on market on a year-over-year basis, which seems like a lot. However, these listings still move relatively quickly, with the average listing sold in 15 days. Contra Costa County single-family homes spend an average of 20 days on the market, representing a 33.33% increase year-over-year. When we turn to the condo market, listings are spending many more days on market, with the average listing in Alameda County selling in 30 days (a 50.00% increase year-over-year), and the average listing in Contra Costa County selling in 41 days (a 78.26% increase year-over-year)

The single-family market is still very competitive, while the condo market is more buyer-friendly

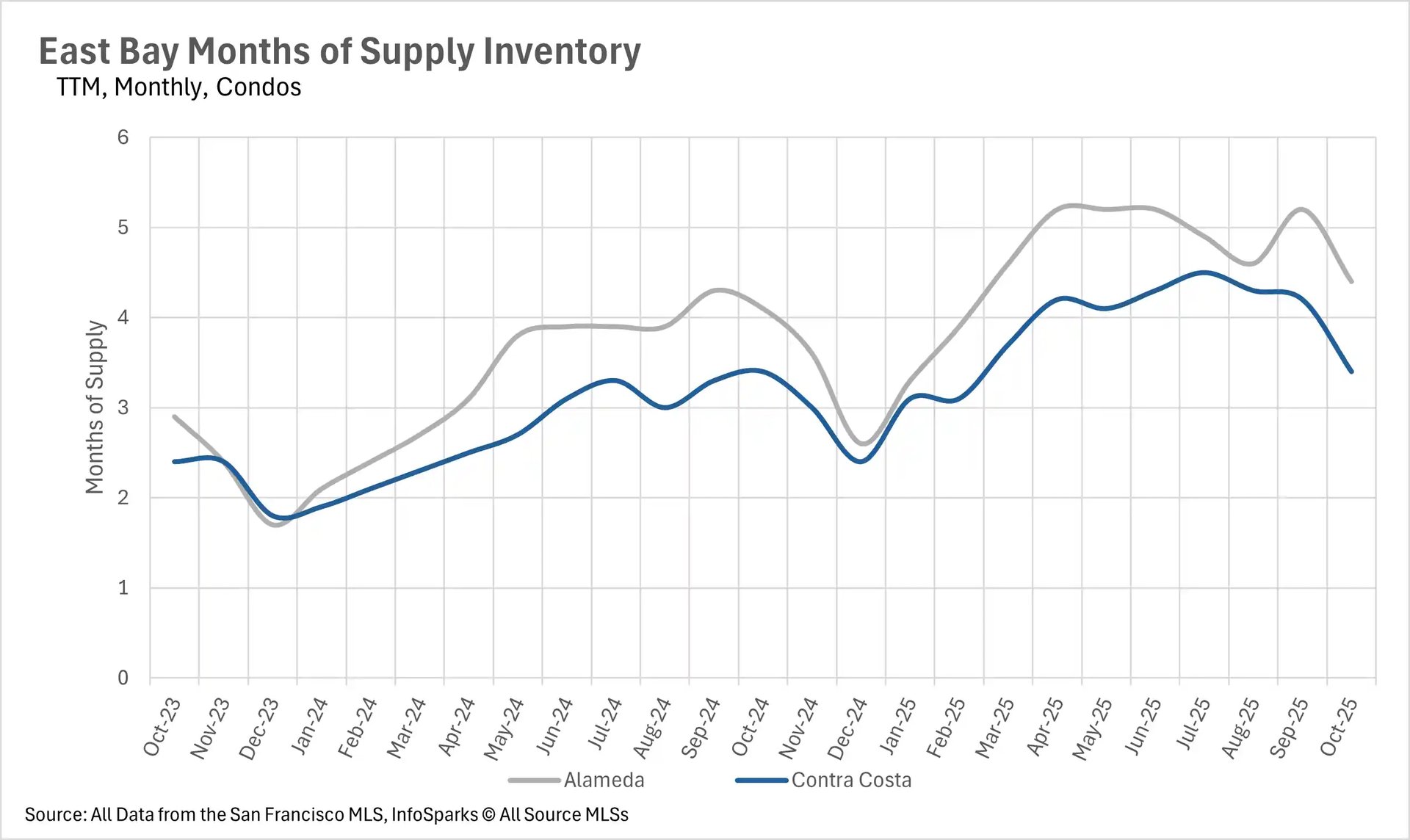

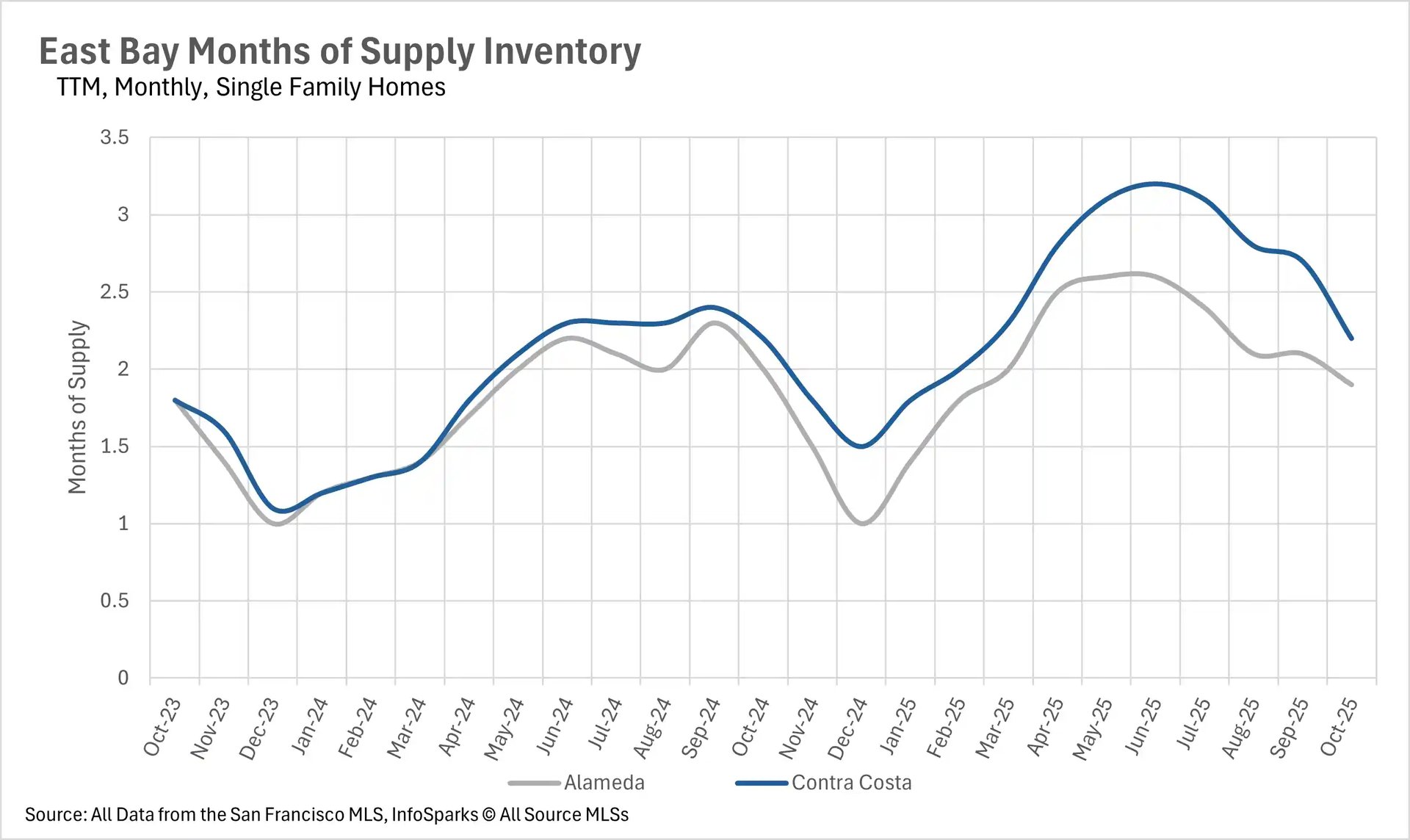

When determining whether a market is a buyers’ market or a sellers’ market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller’s market, whereas markets with more than three months of MSI are considered buyers’ markets.

As per usual, the single-family home market is much more competitive than the condo market. The East Bay is a seller's market when it comes to single-family homes, with Alameda County having 1.9 months of supply on the market, and Contra Costa County having 2.2 months. Whereas the East Bay condo market is a buyer's market, with 4.4 months of supply on the market in Alameda County and 3.4 months of supply on the market in Contra Costa County.