Select a Market Report to Read:

- National Market Update Overview

- Bay Area Report

- North Bay Report

- East Bay Report

- Silicon Valley Report

- San Francisco Report

Quick Take

- The Bay Area real estate market in June shows a clear bifurcation between San Francisco's surging prices and widespread declines in other regions' condo markets.

- Inventory levels have reached local peaks across most regions and are beginning to decline, with the sharpest drawdowns occurring in the North Bay and San Francisco.

- Despite inventory reductions, listings are spending significantly more time on the market throughout the Bay Area, with condos experiencing particularly dramatic increases in market time.

- The market continues to strongly favor single-family homes over condos, with the condo market presenting substantial opportunities for buyers across all regions.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

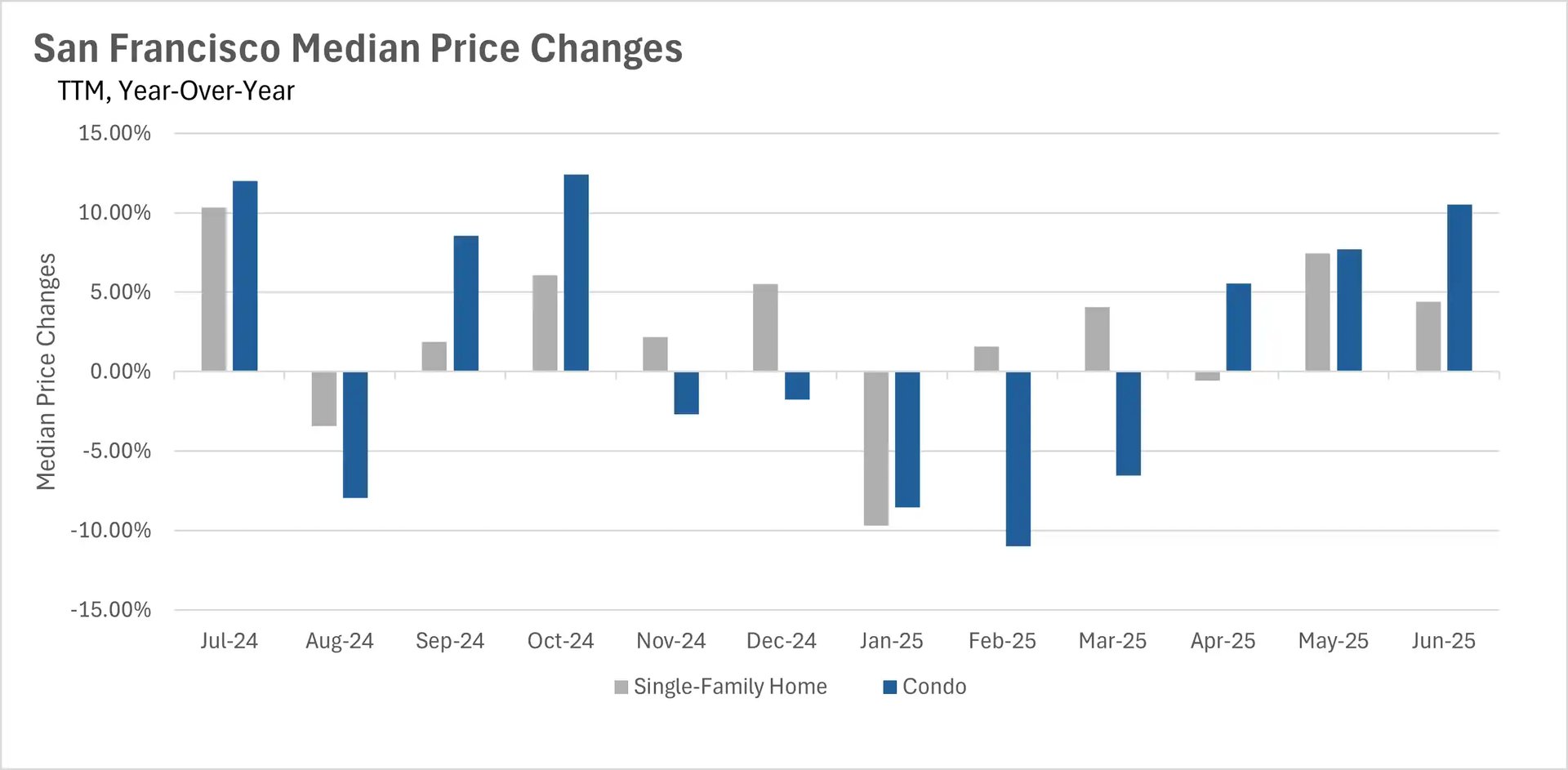

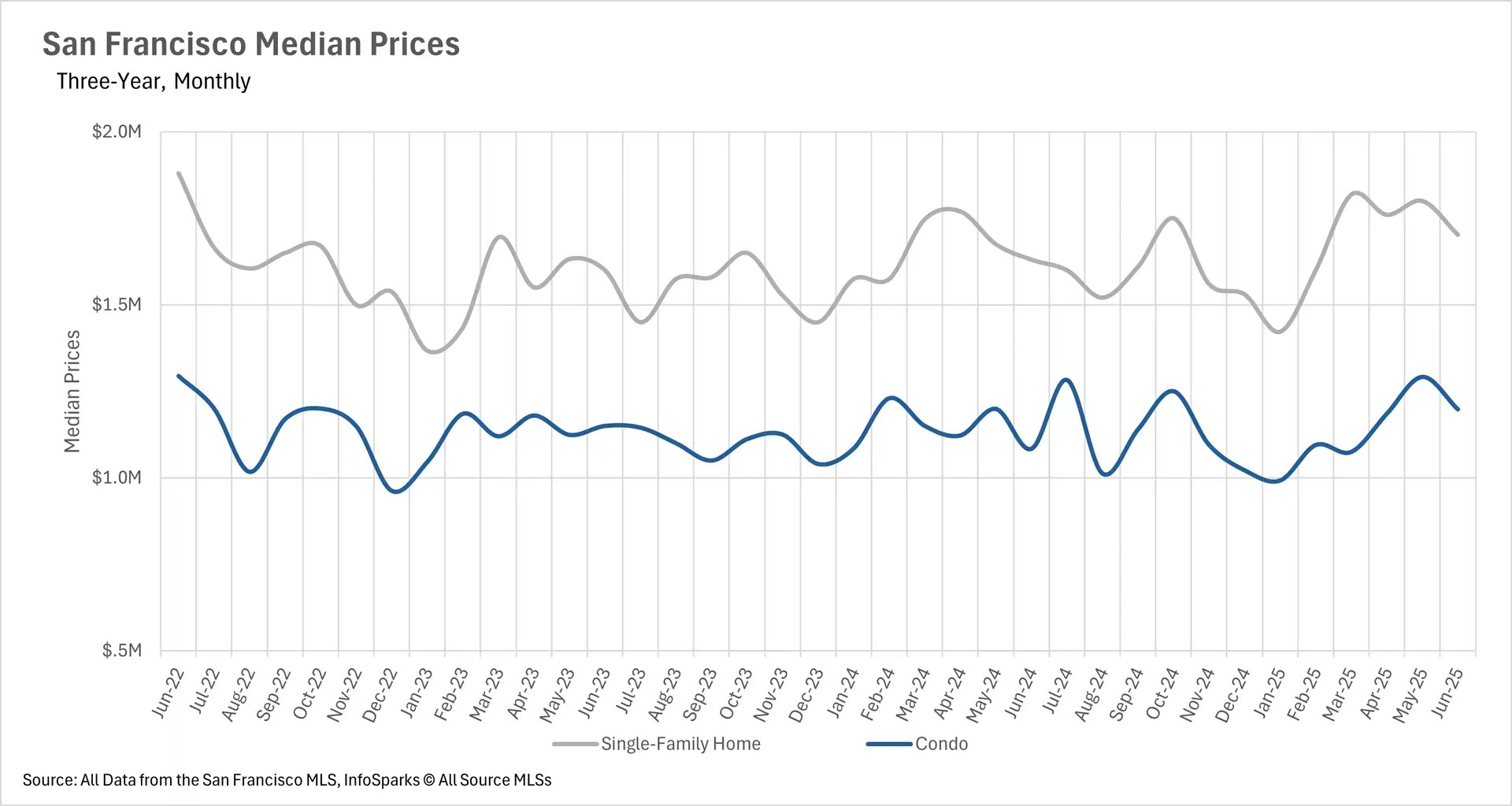

San Francisco leads price appreciation while condo markets struggle regionwide

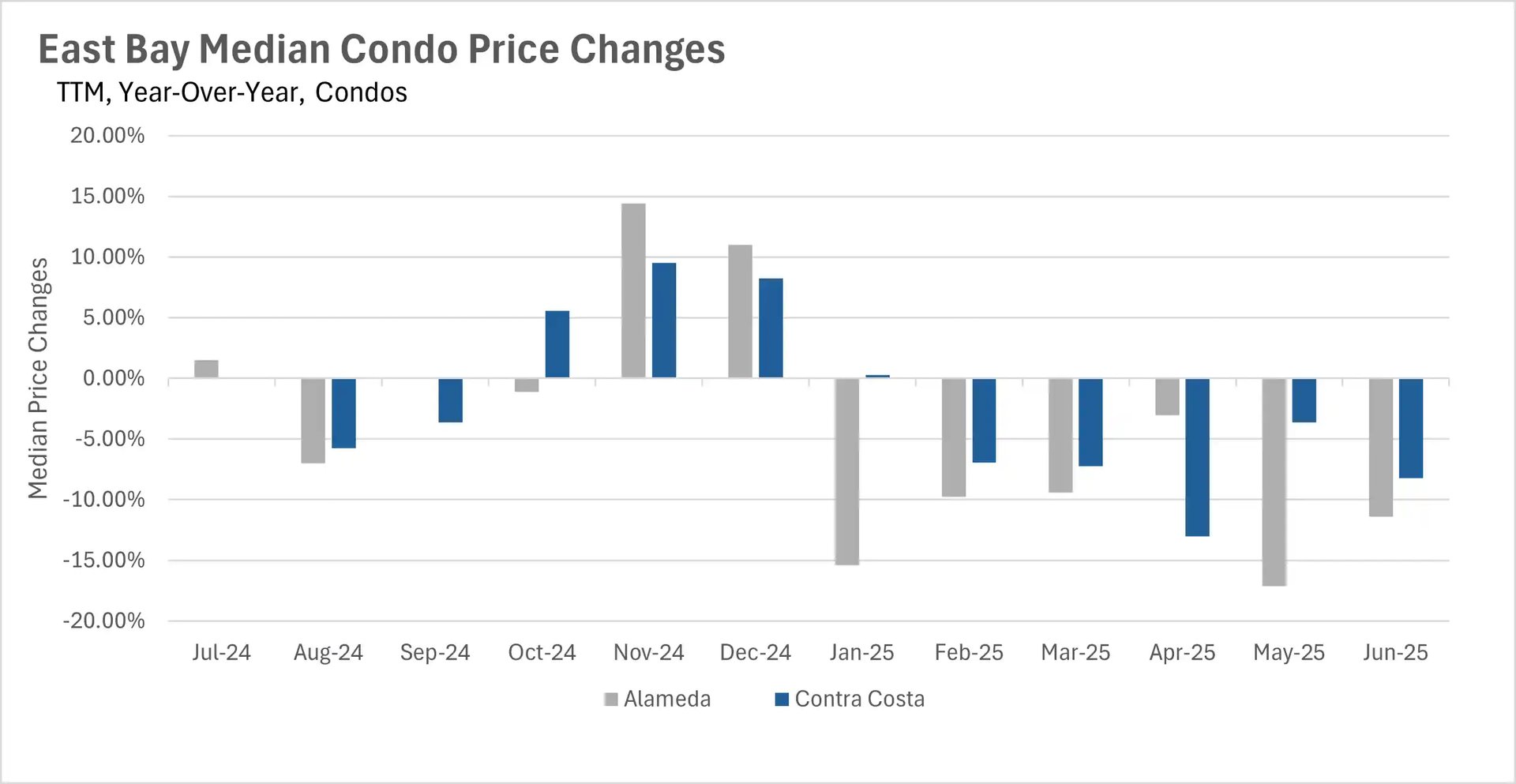

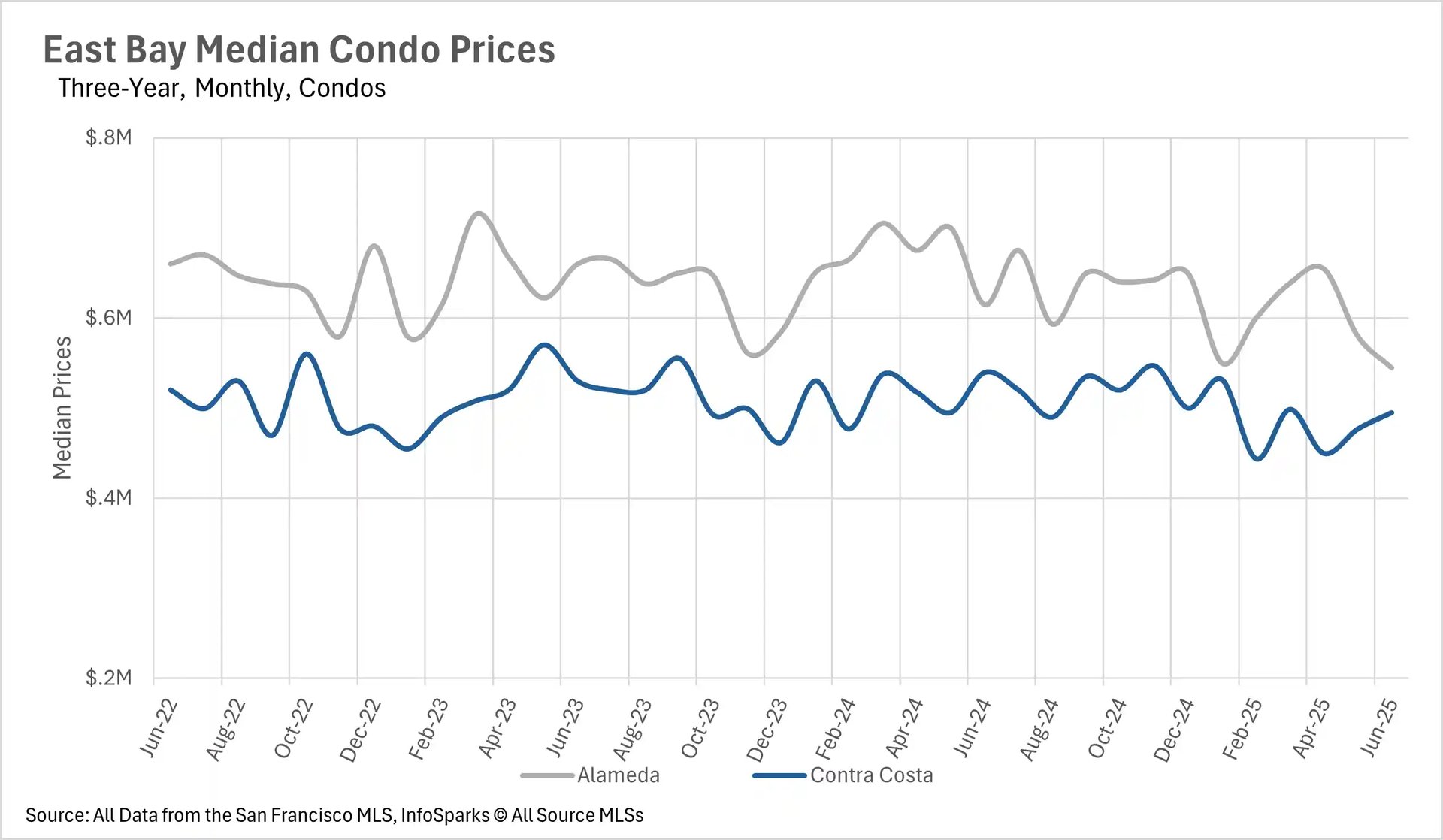

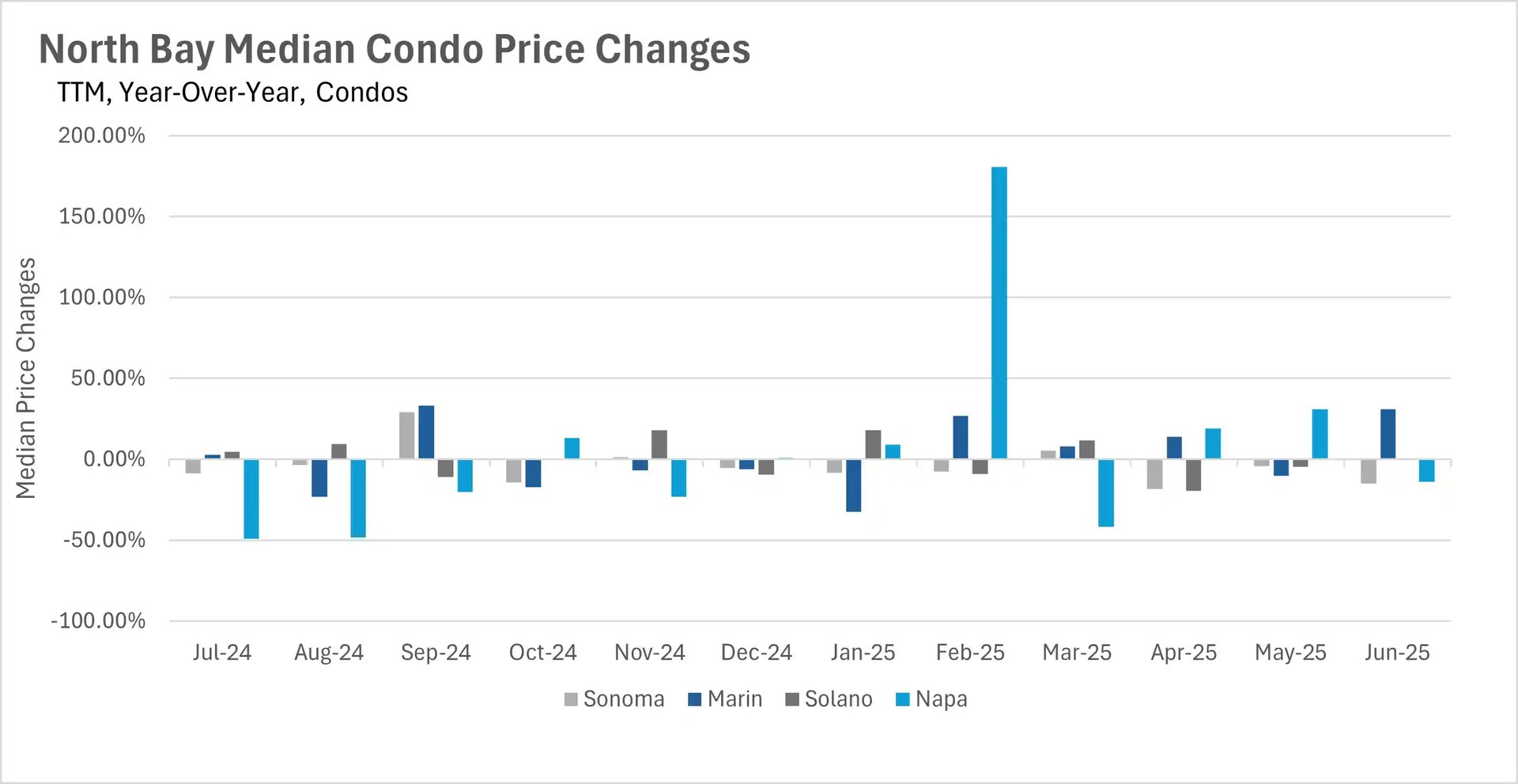

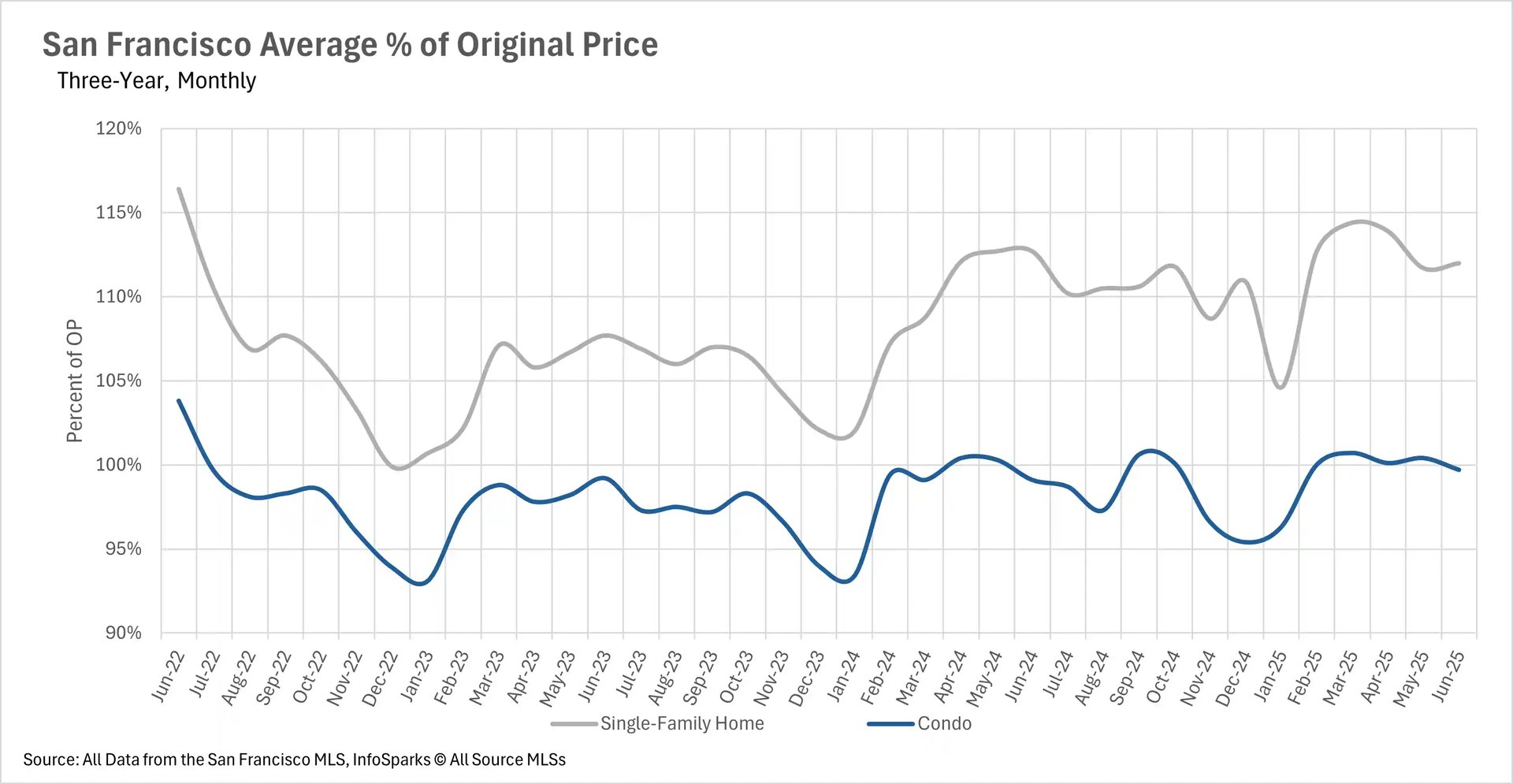

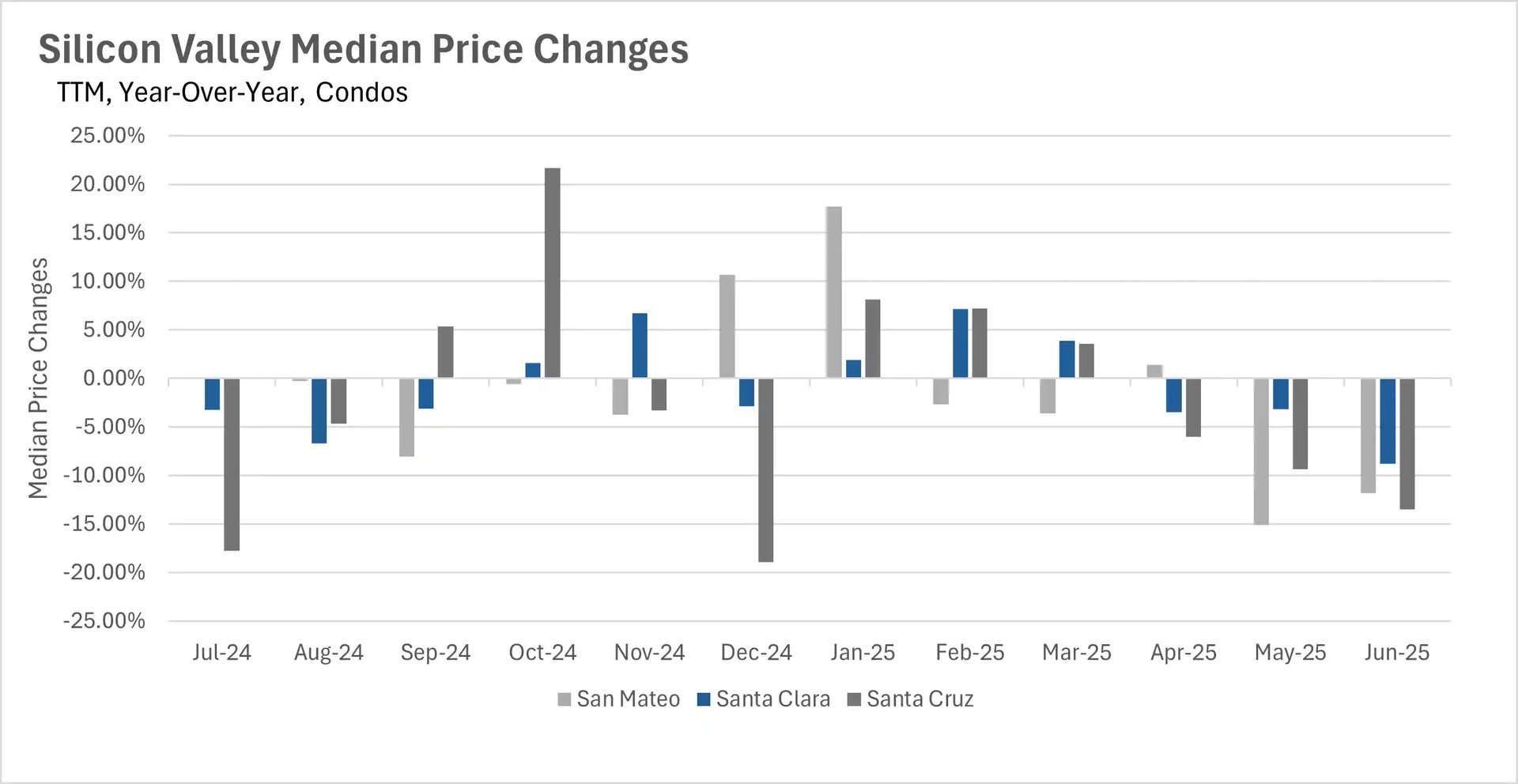

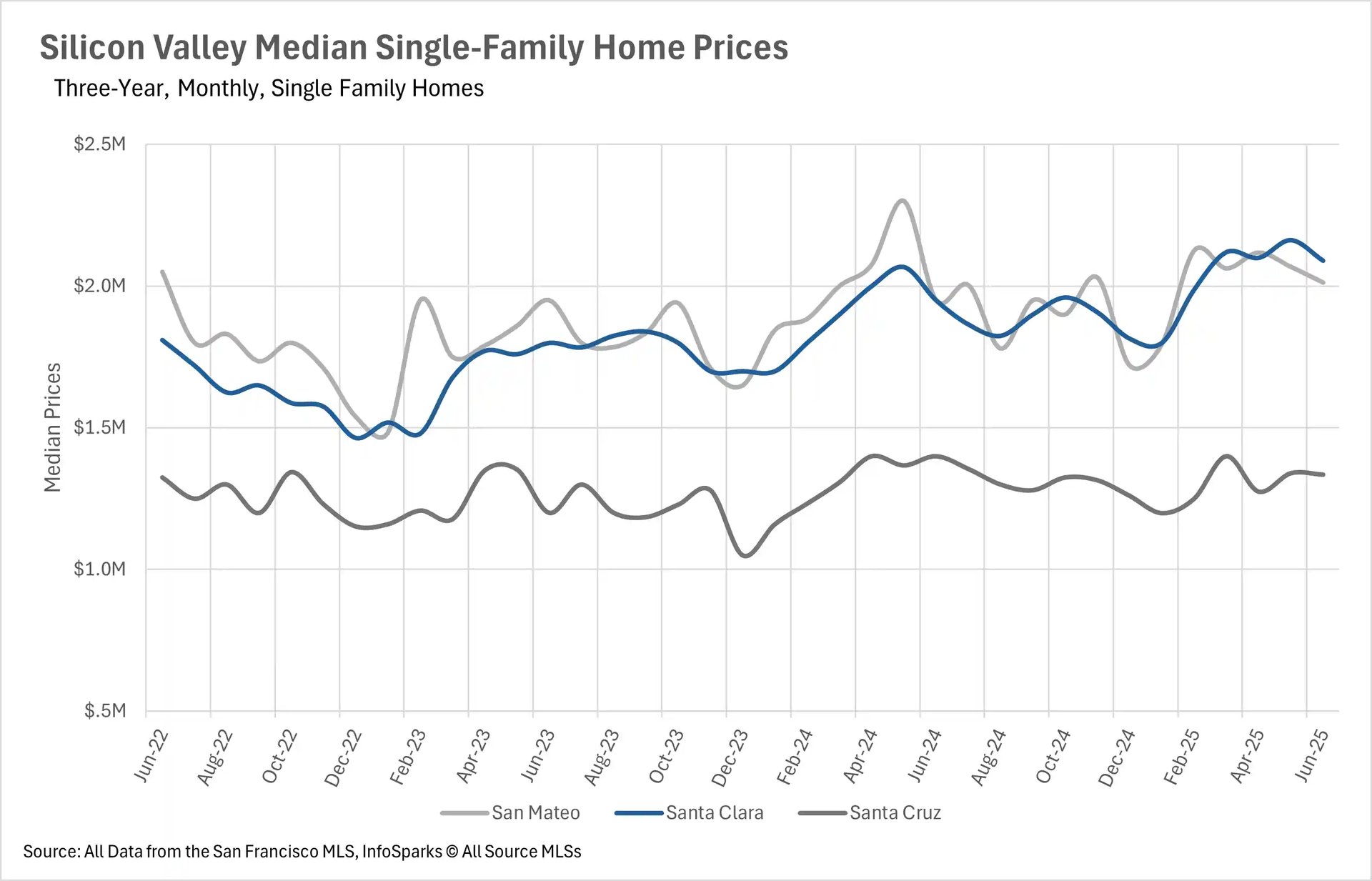

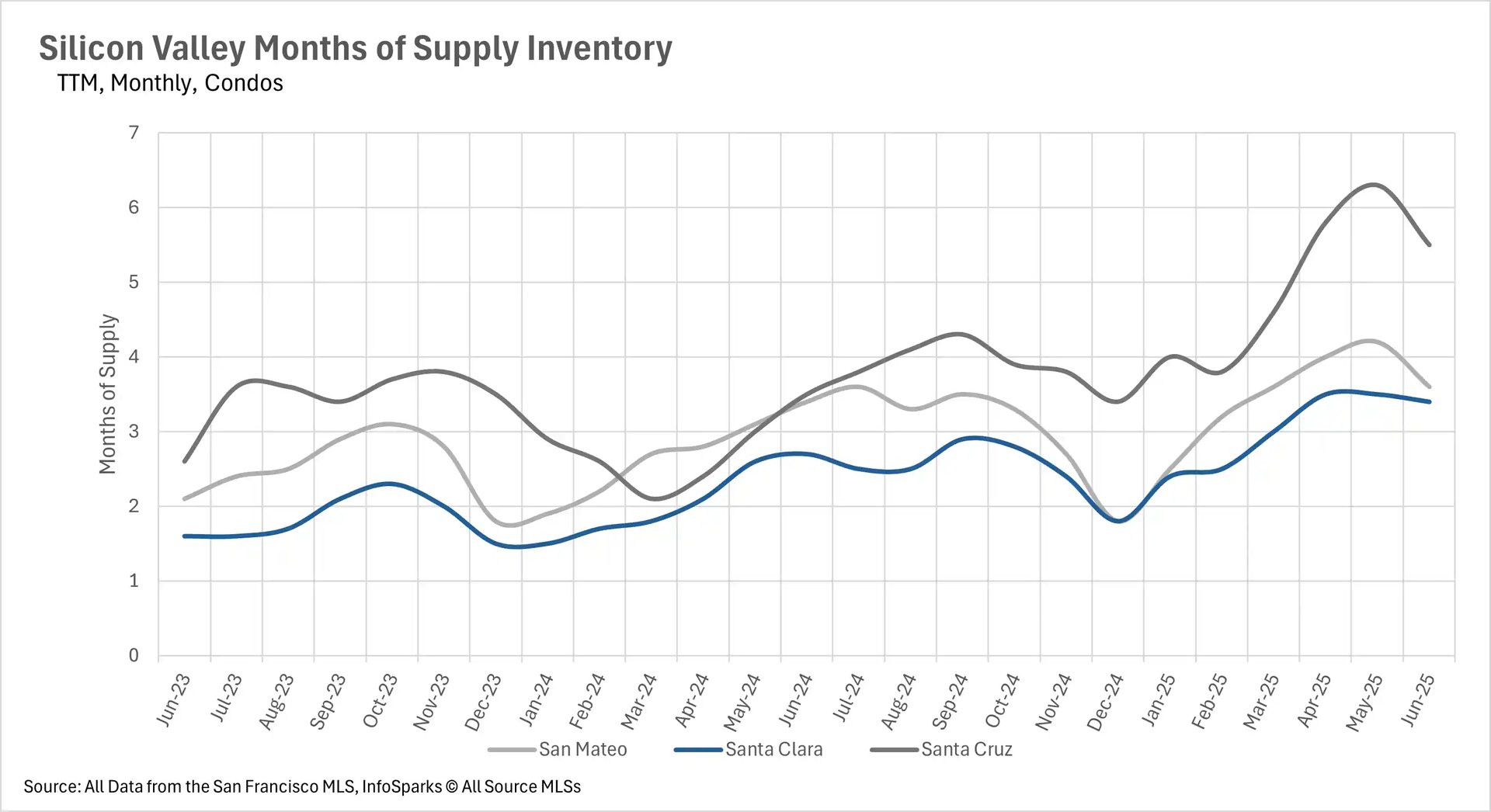

June showcased San Francisco's continued dominance in the Bay Area real estate market, with single-family home prices rising 4.42% year-over-year and condos surging an impressive 10.52% - marking over a year of consistent growth. This stands in stark contrast to the broader Bay Area, where condo markets are experiencing significant stress. The East Bay recorded its fifth consecutive month of year-over-year condo price declines, with condos down 11.41% in Alameda County and 8.25% in Contra Costa County. Silicon Valley's condo market also continued its downward trajectory for the third straight month, with Santa Clara County down 8.79%, San Mateo County declining 11.84%, and Santa Cruz County experiencing a dramatic 13.52% drop.

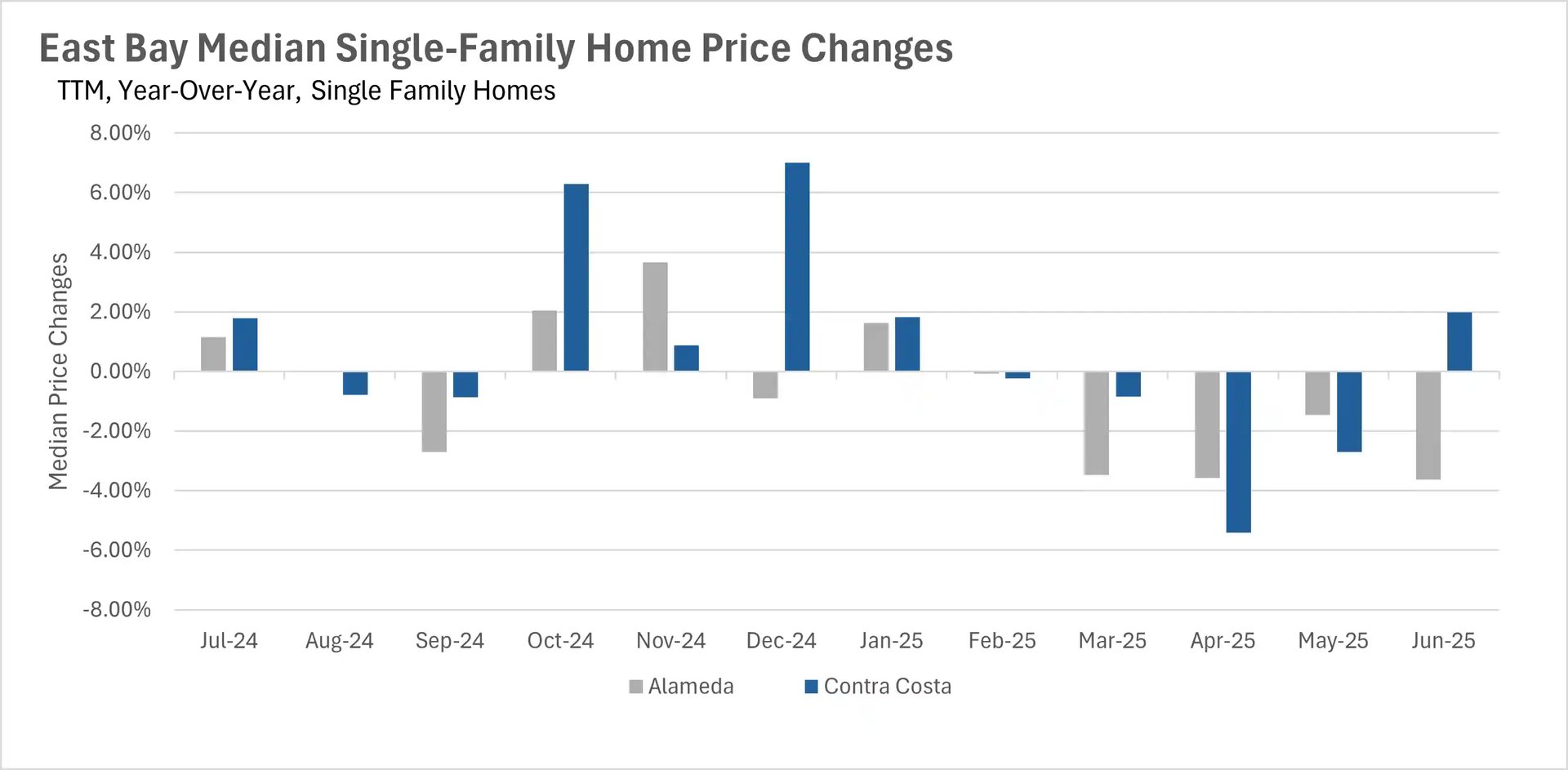

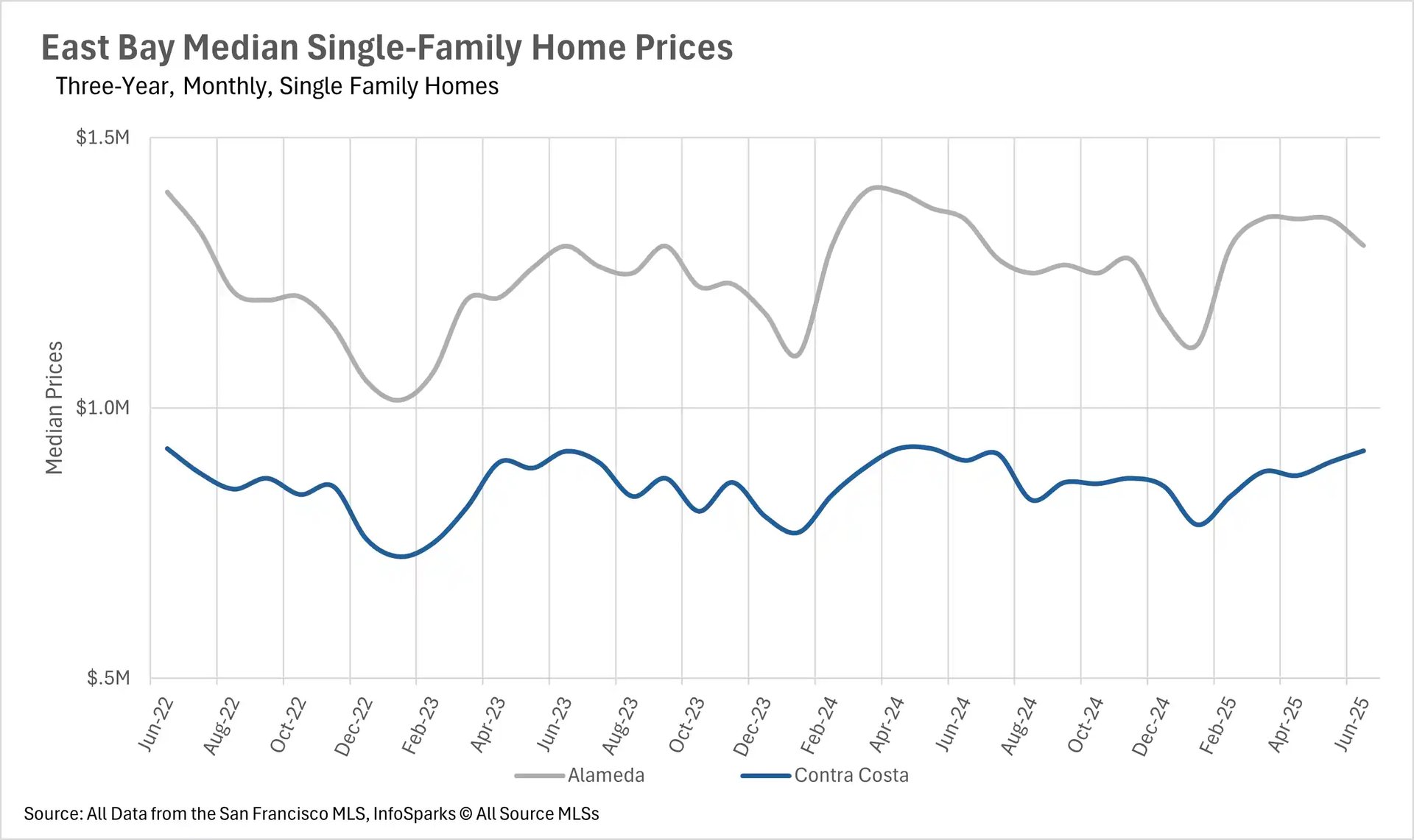

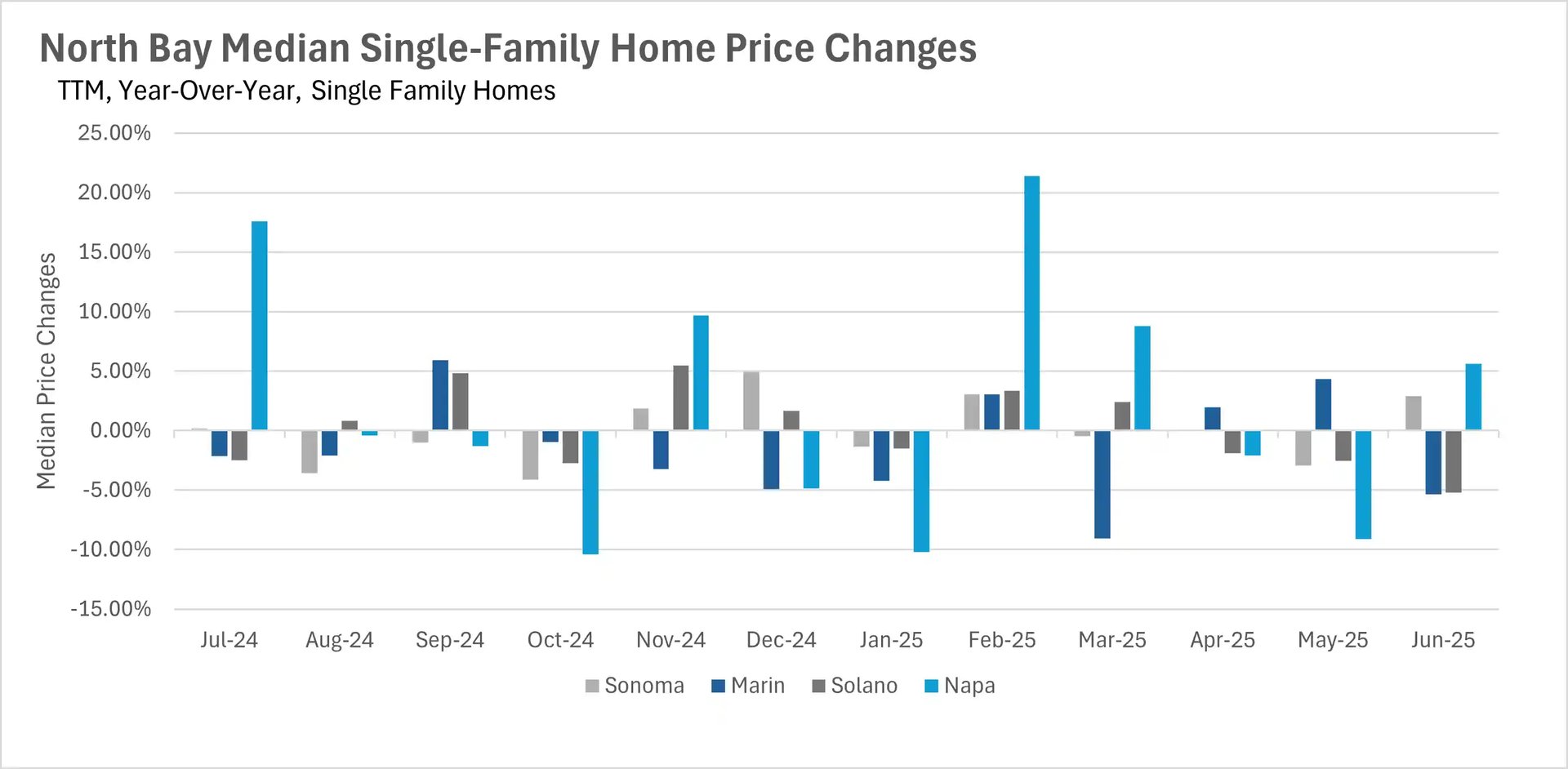

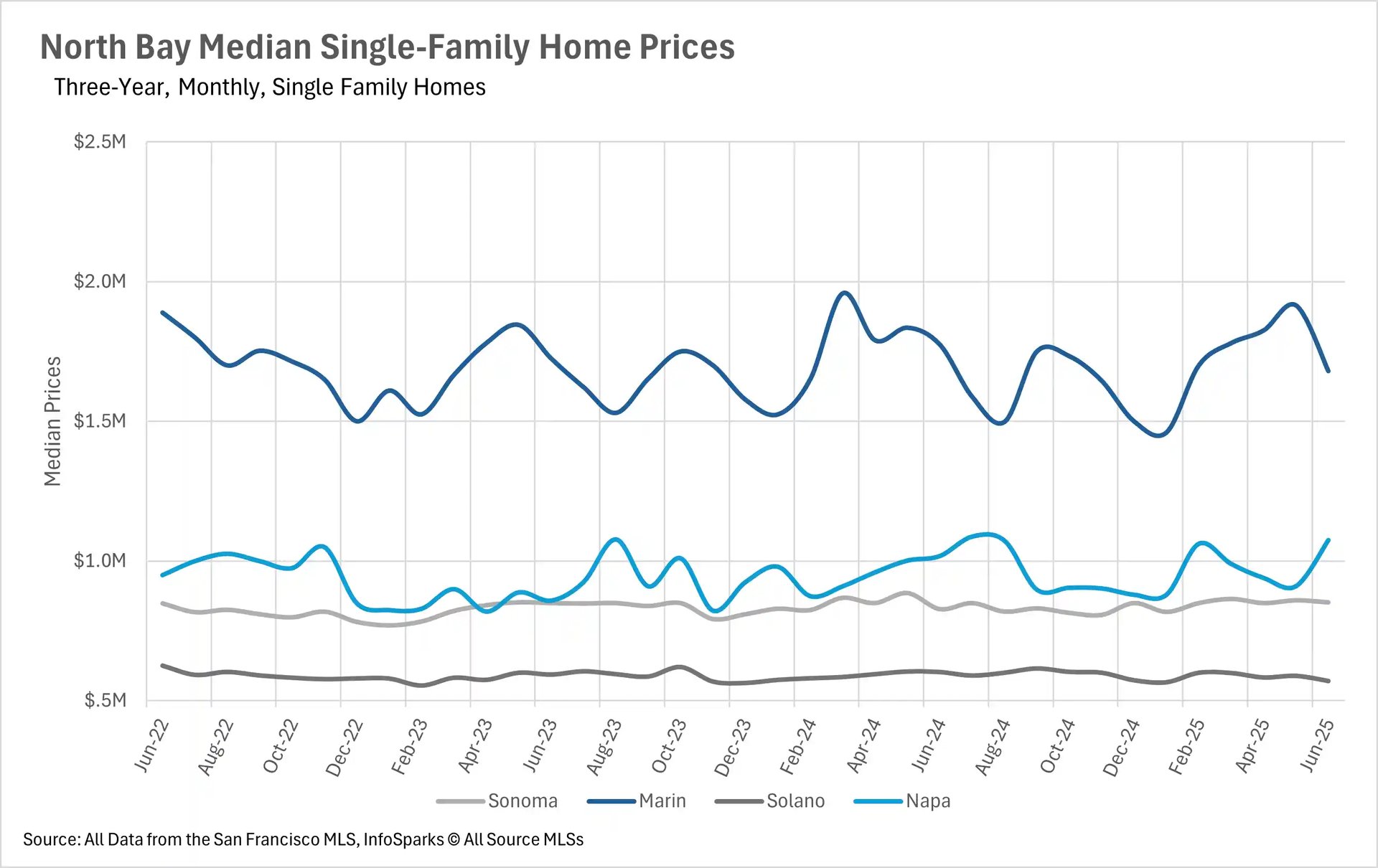

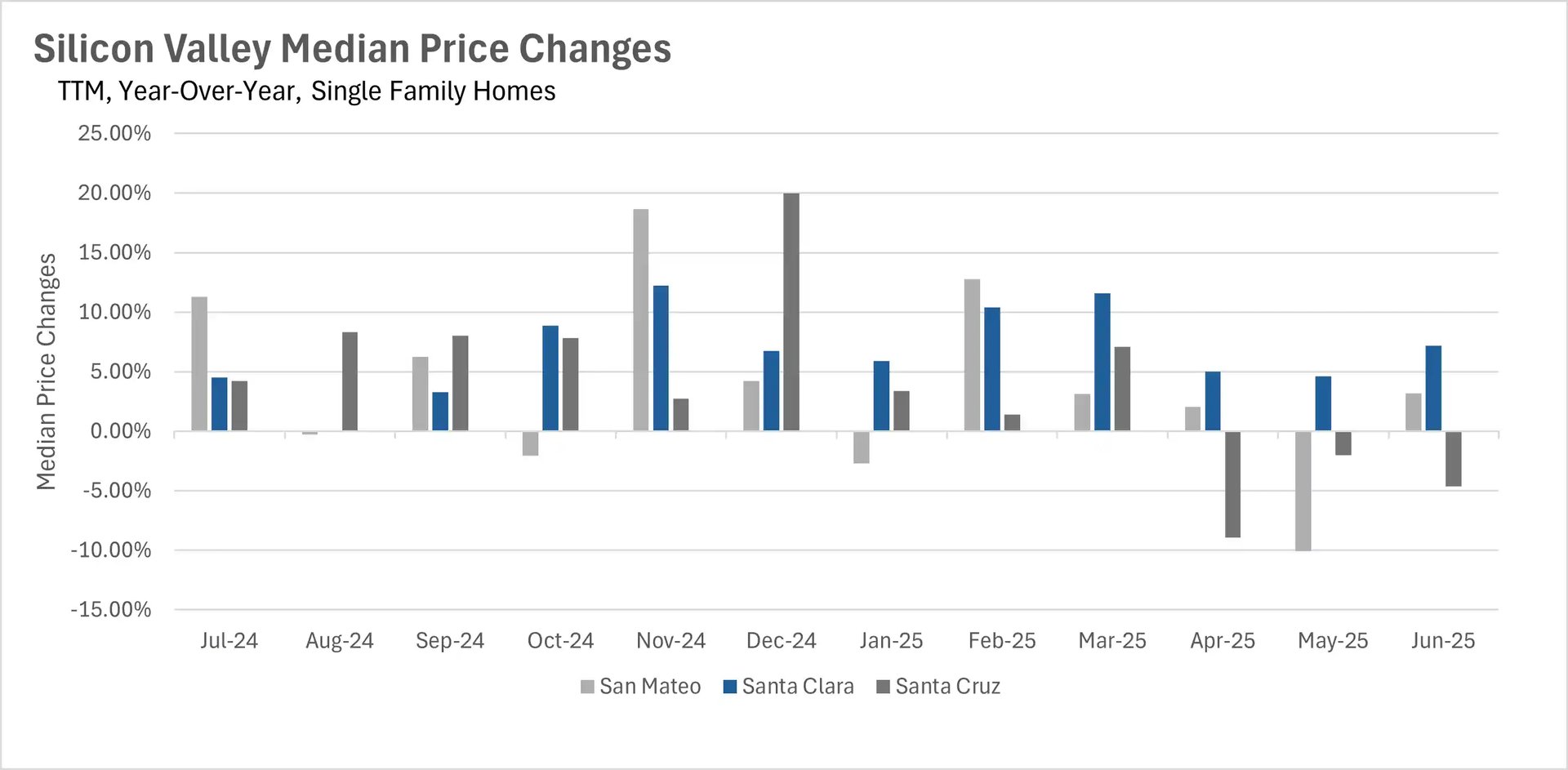

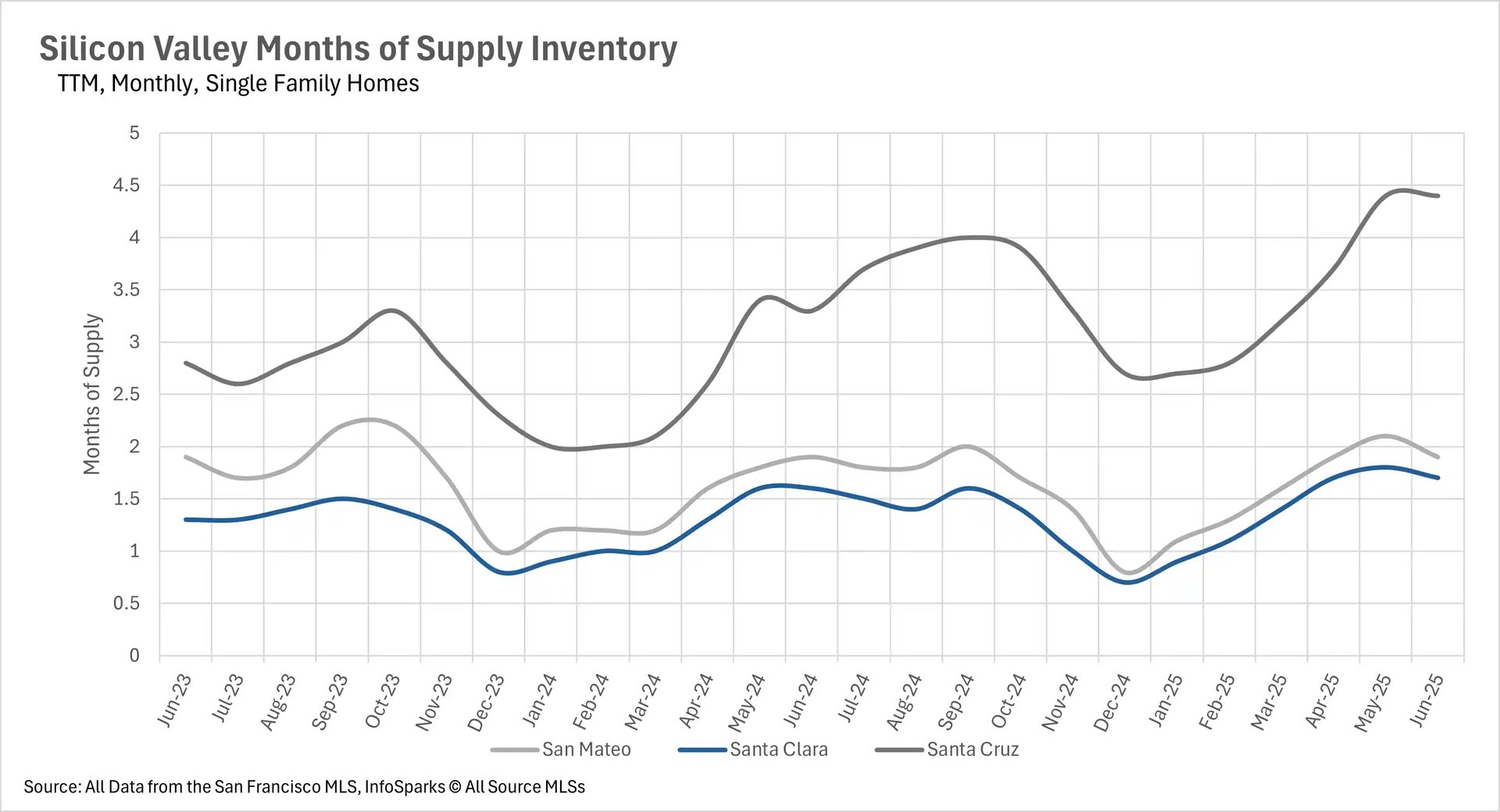

The North Bay showed the most stability in single-family homes, with Sonoma County up 2.92% and Napa County rising 5.60%, though Solano and Marin Counties saw declines of 5.23% and 5.35% respectively. Single-family homes in Silicon Valley demonstrated resilience with San Mateo and Santa Clara Counties posting gains of 3.21% and 7.18%, while only Santa Cruz County declined by 4.64%. The East Bay's single-family market showed mixed results with Contra Costa County managing a modest 1.99% increase while Alameda County continued its five-month decline.

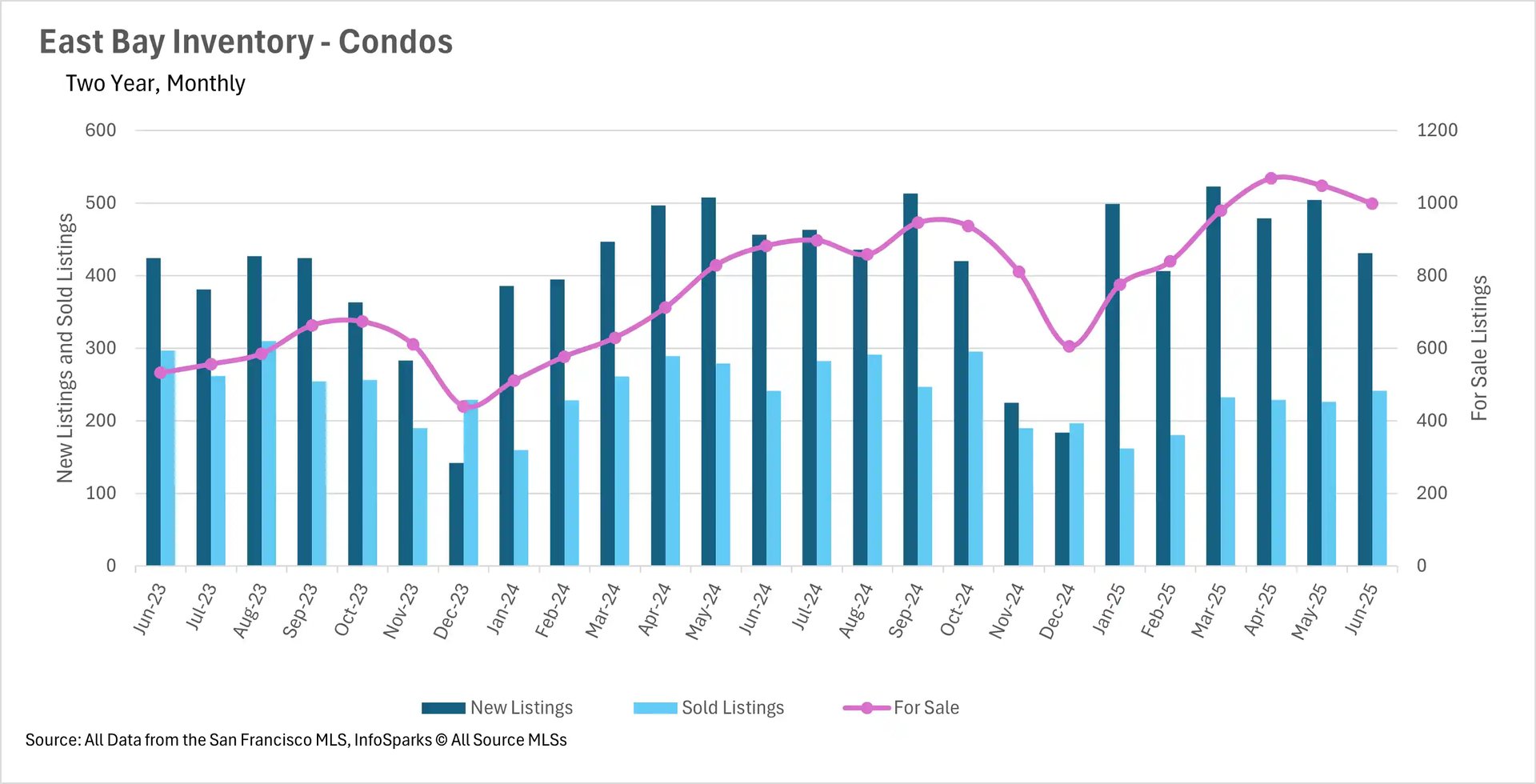

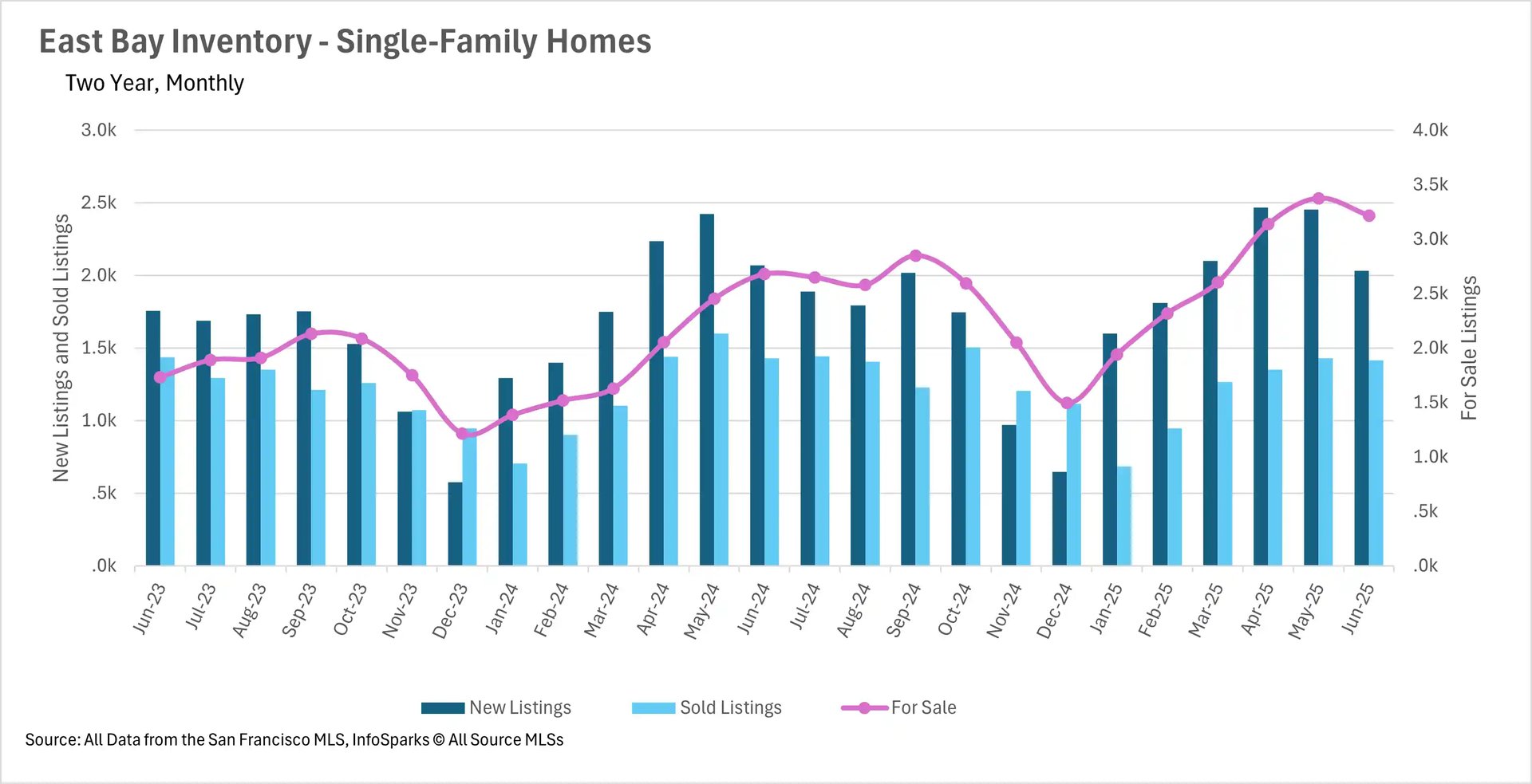

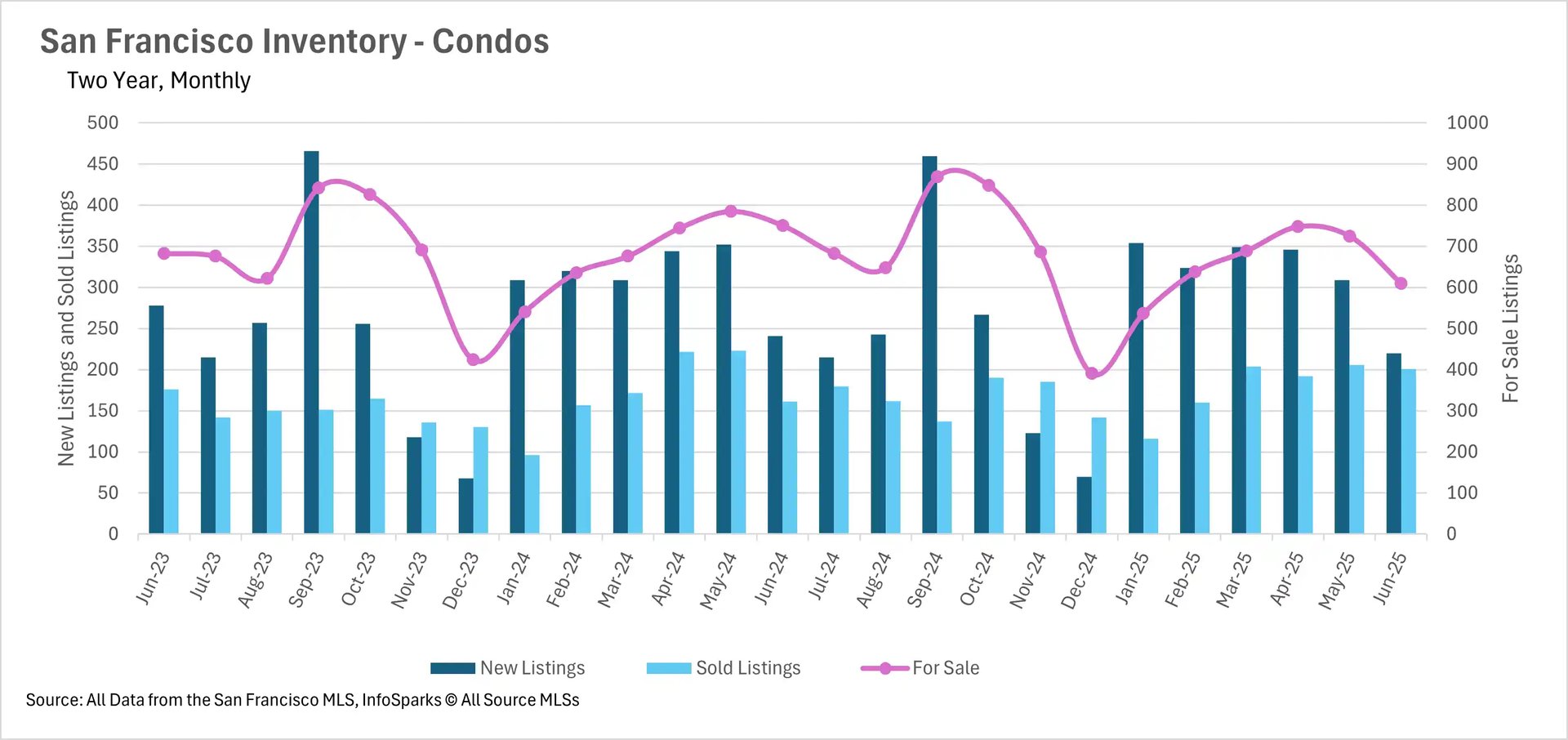

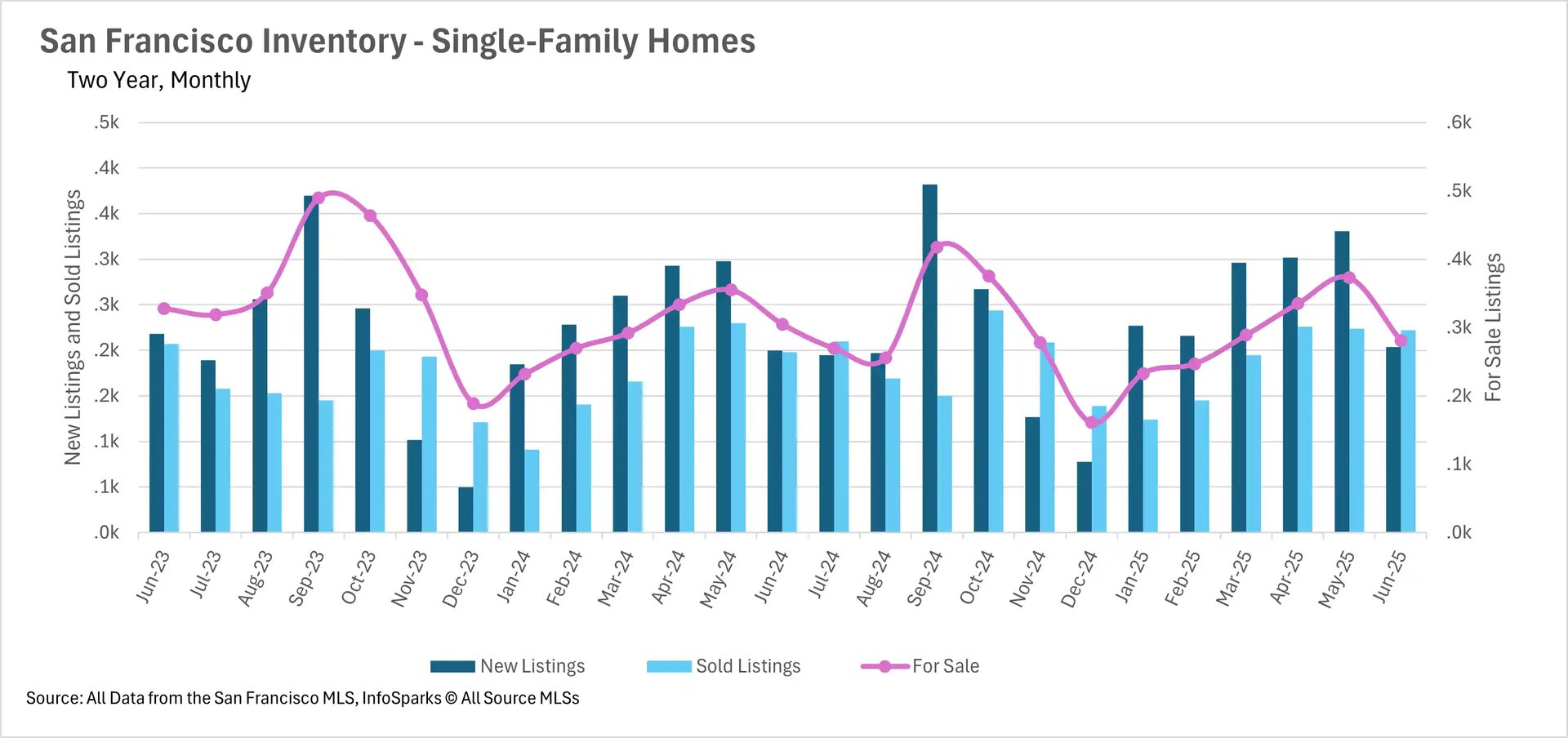

Regional inventory trends reveal market consolidation

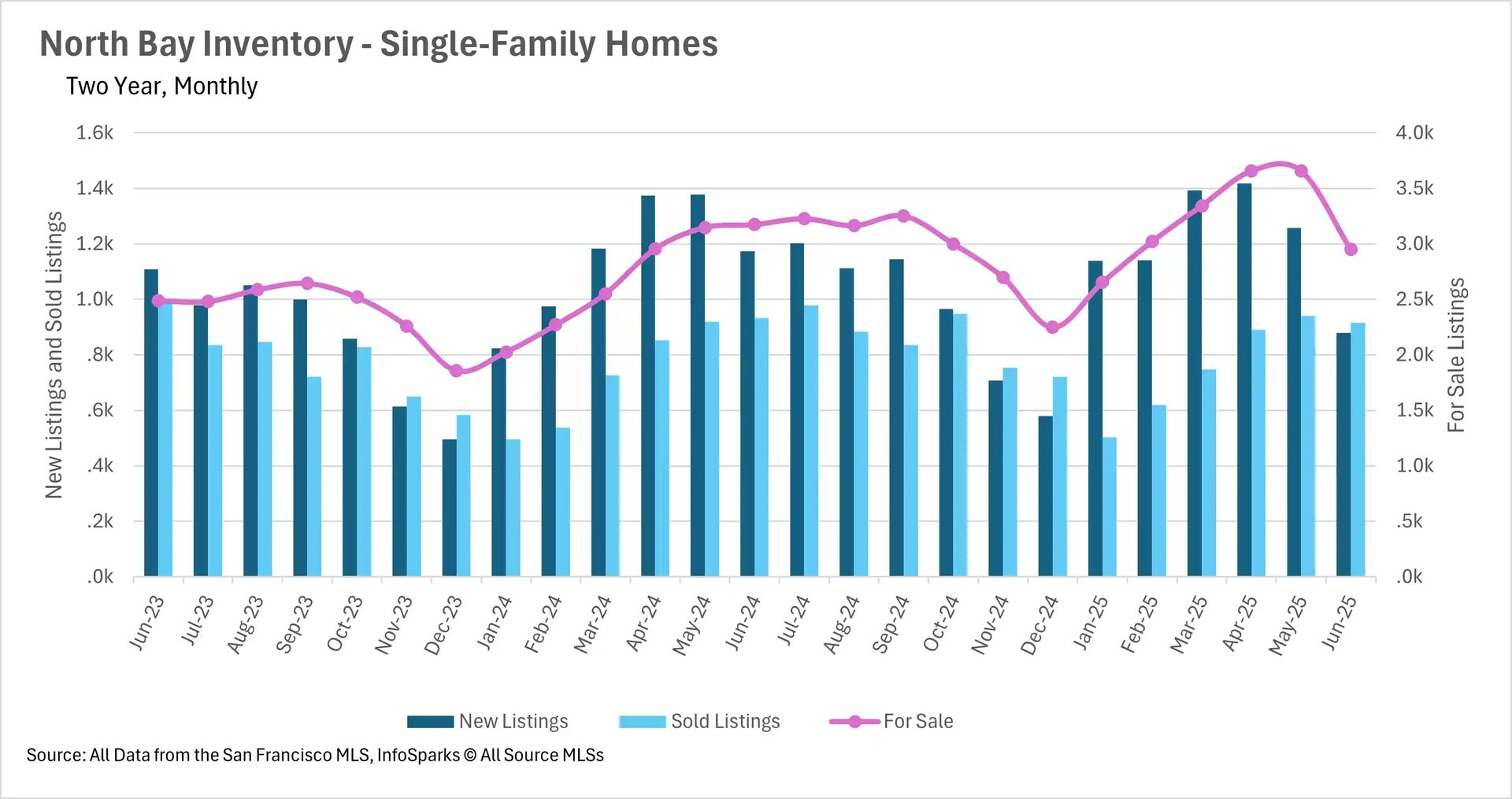

June marked a significant shift in inventory dynamics across the Bay Area, with most regions experiencing substantial month-over-month declines after reaching local peaks in May. The North Bay witnessed one of the sharpest inventory declines in recent history, with single-family home inventory falling 19.34% month-over-month (though still down only 7.09% year-over-year) and condo inventory dropping 19.76% month-over-month. San Francisco continued its multi-year inventory decline trend with single-family homes down 7.87% year-over-year and condos showing an even steeper 18.77% decline.

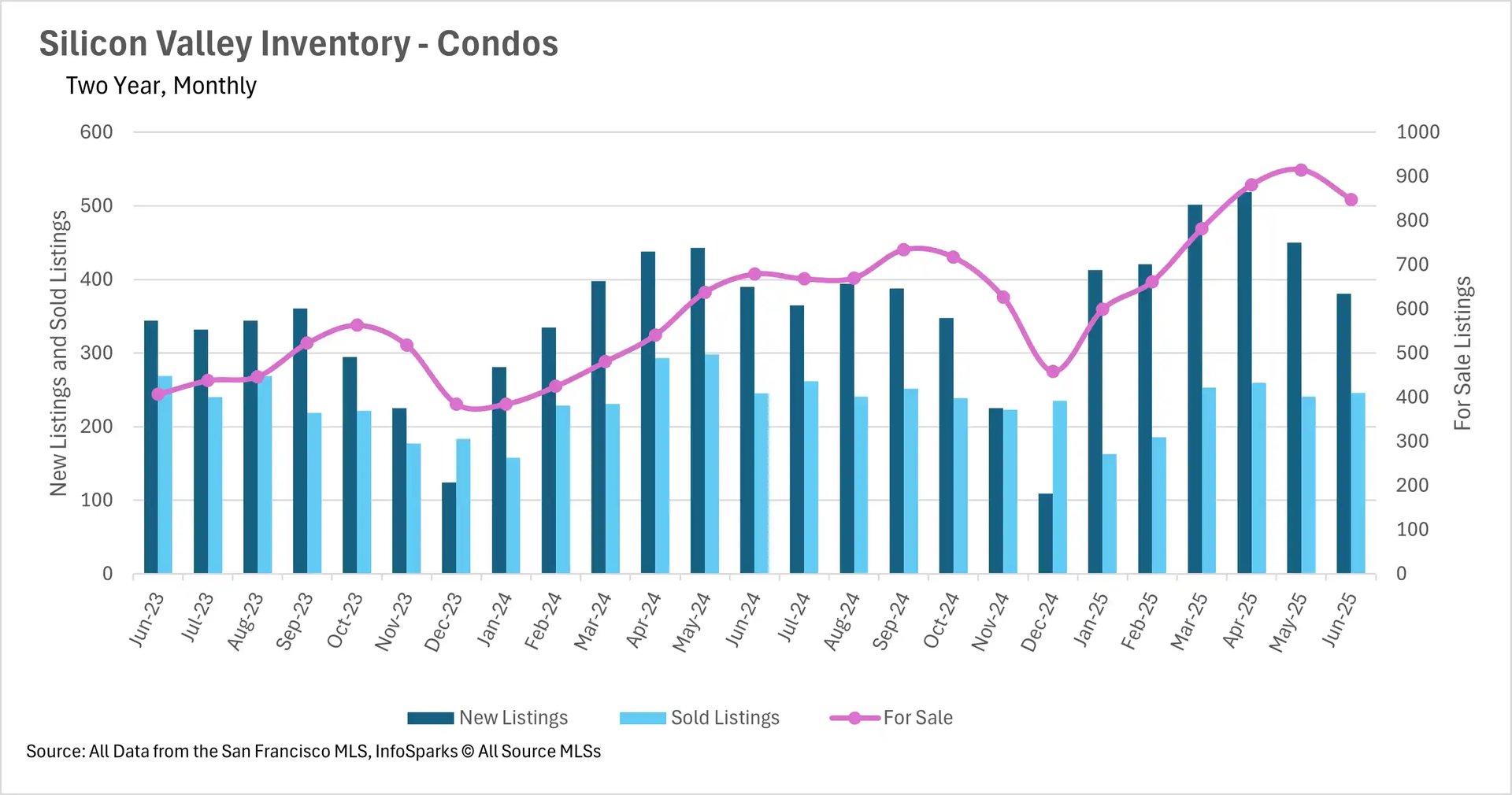

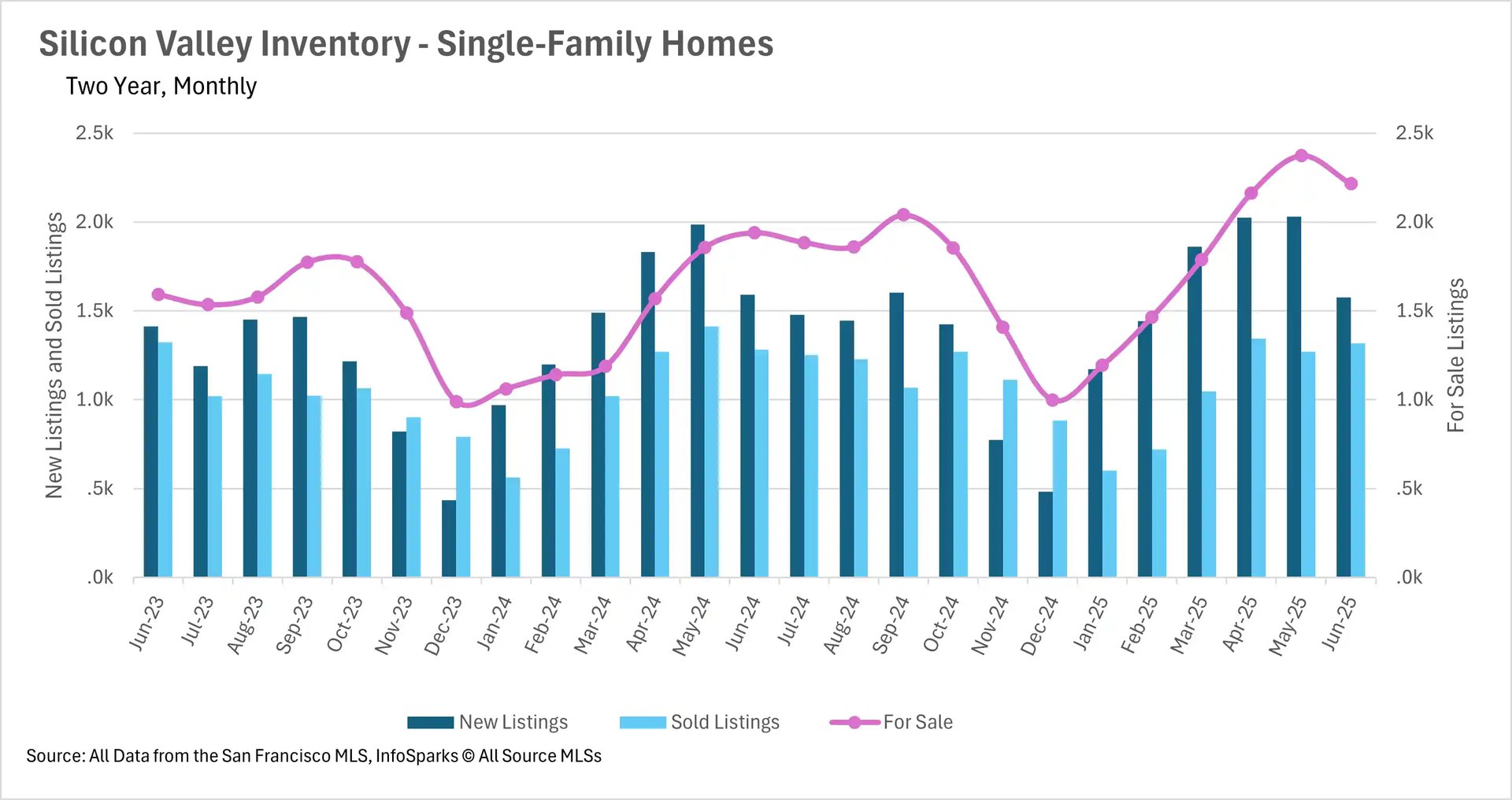

Silicon Valley and the East Bay appear to have reached their inventory peaks, with both regions seeing decreases in June despite maintaining significantly higher levels than last year. The East Bay still shows single-family inventory 20.05% higher year-over-year and condo inventory 13.15% higher, while Silicon Valley maintains 14.18% more single-family listings and 24.89% more condo listings than June 2024. The common thread across all regions is that inventory declines are being driven more by fewer new listings hitting the market rather than increased sales activity, suggesting seller hesitancy rather than buyer demand.

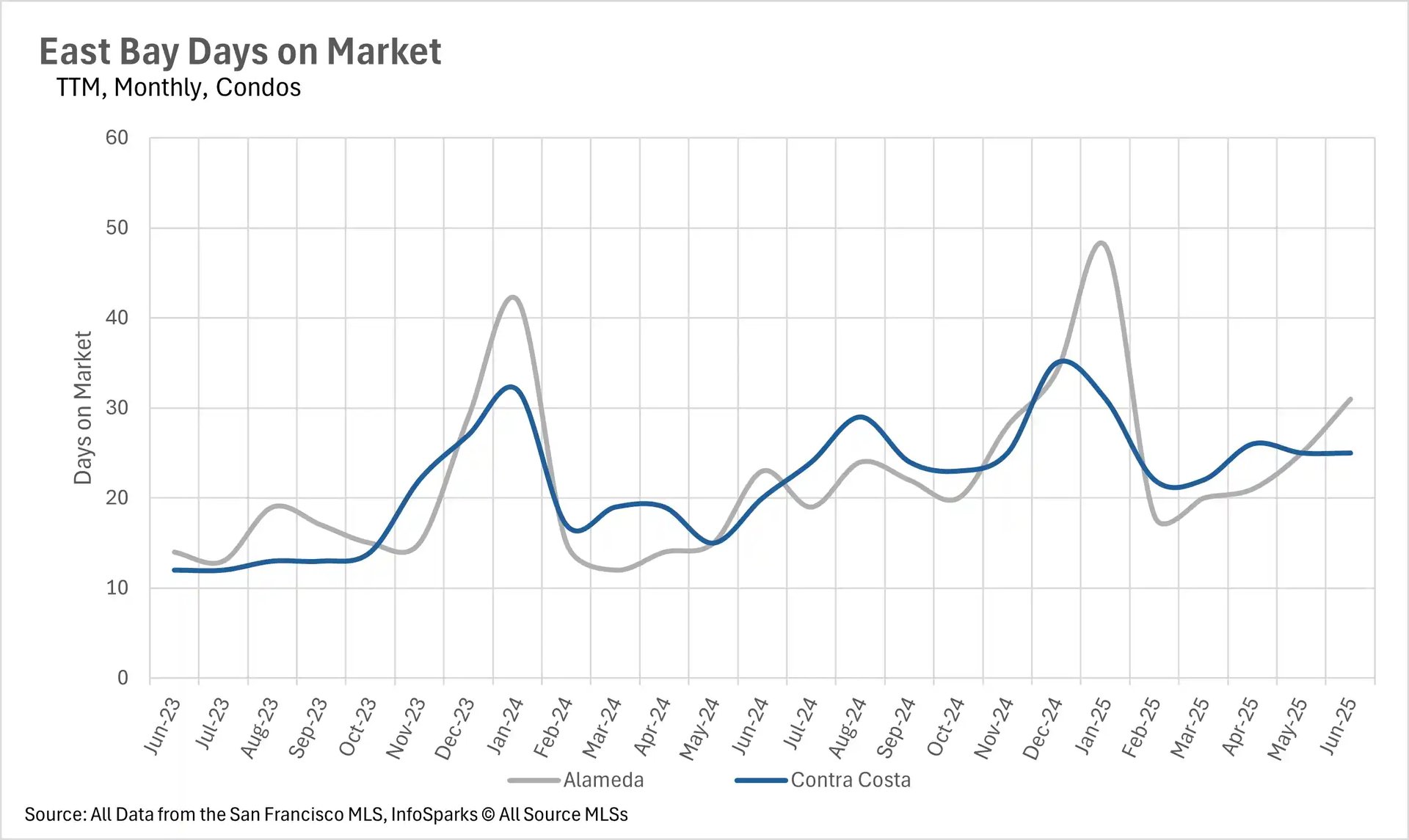

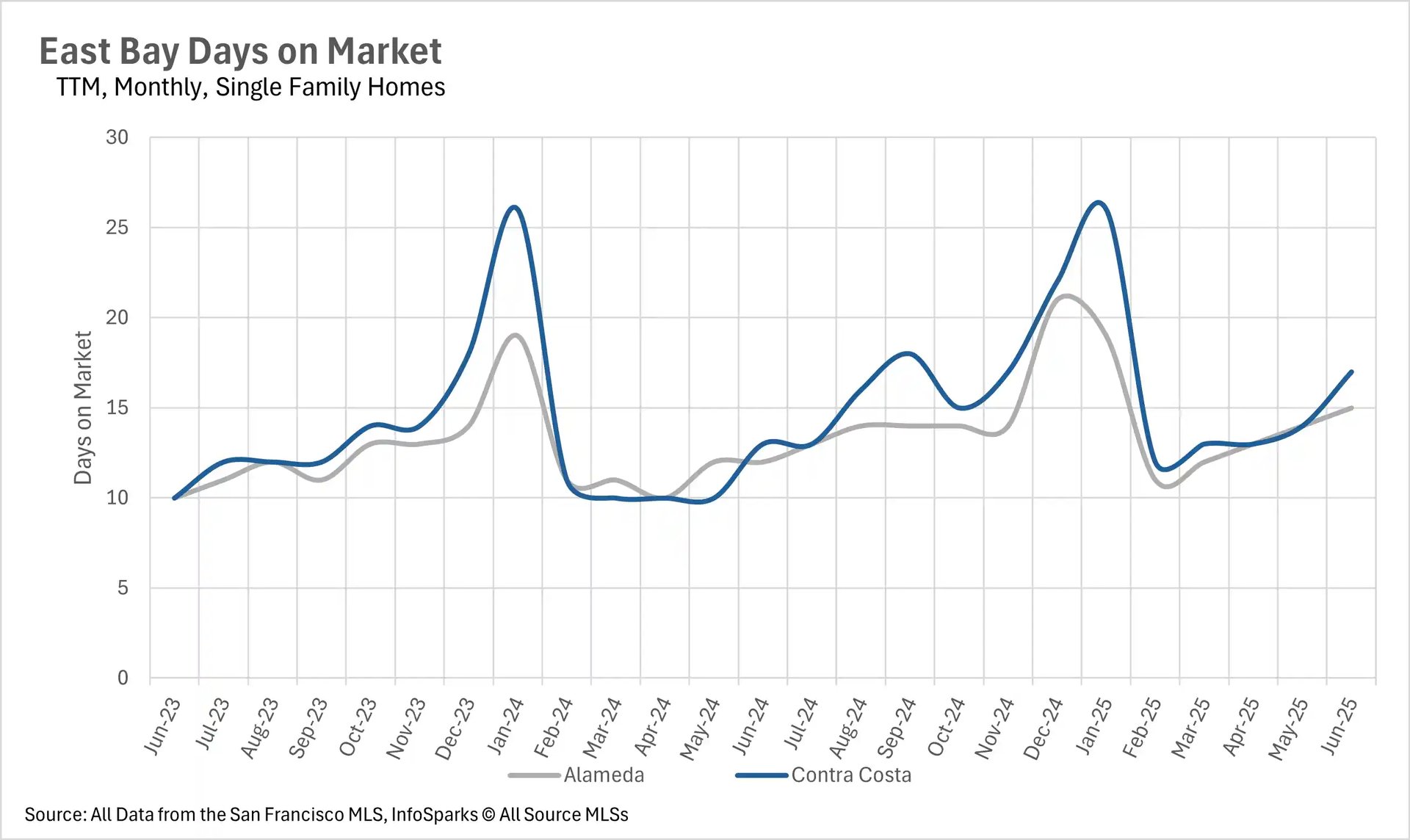

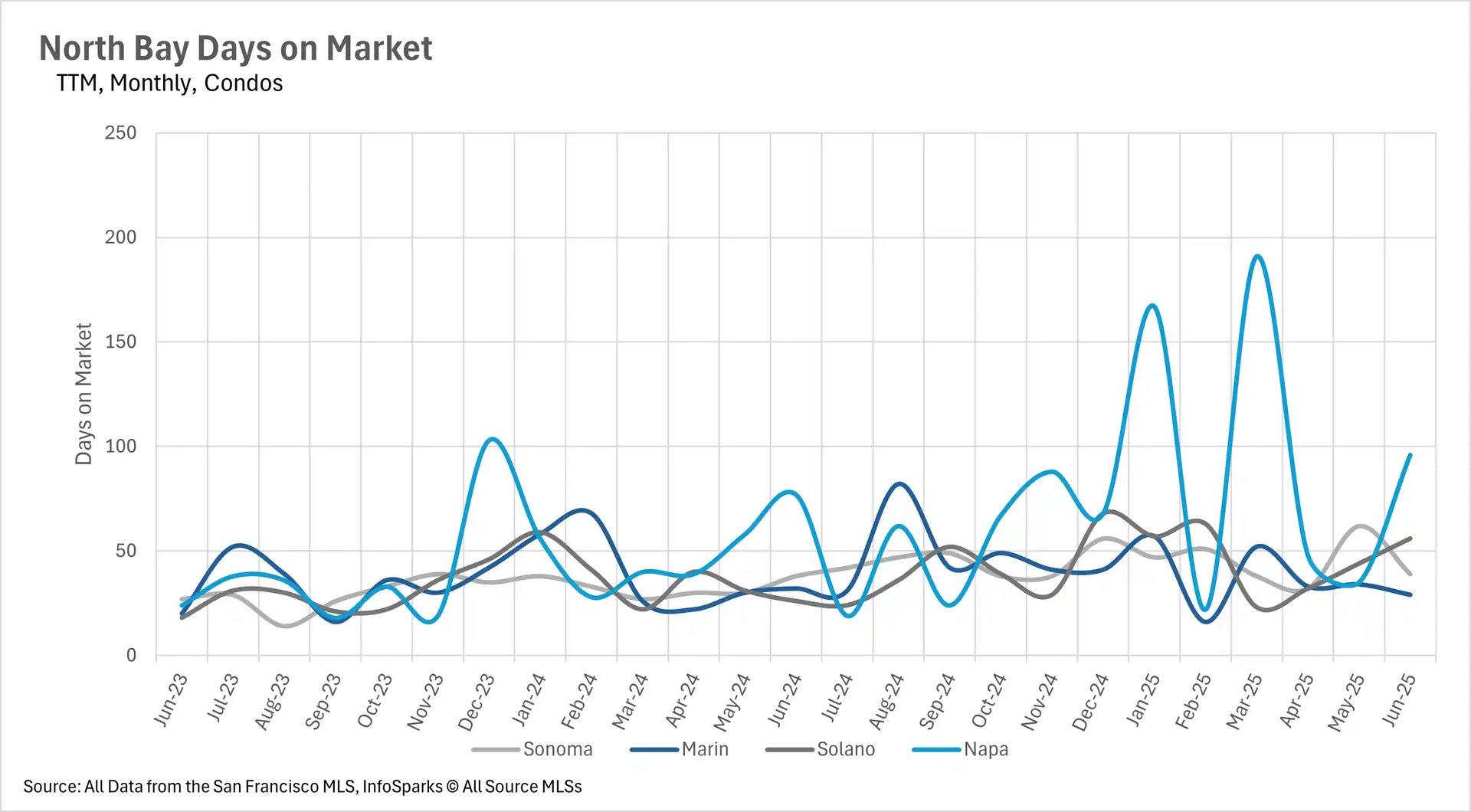

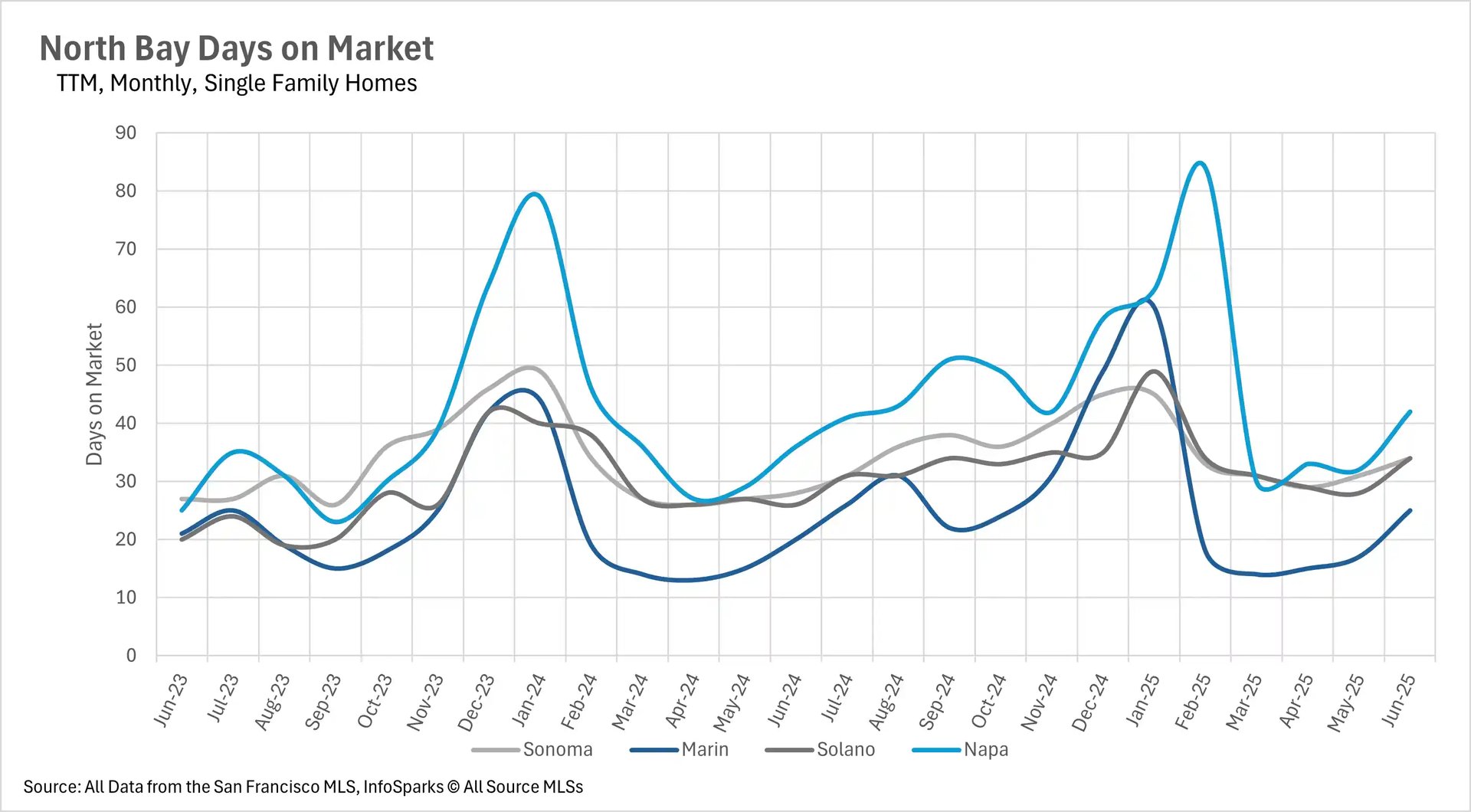

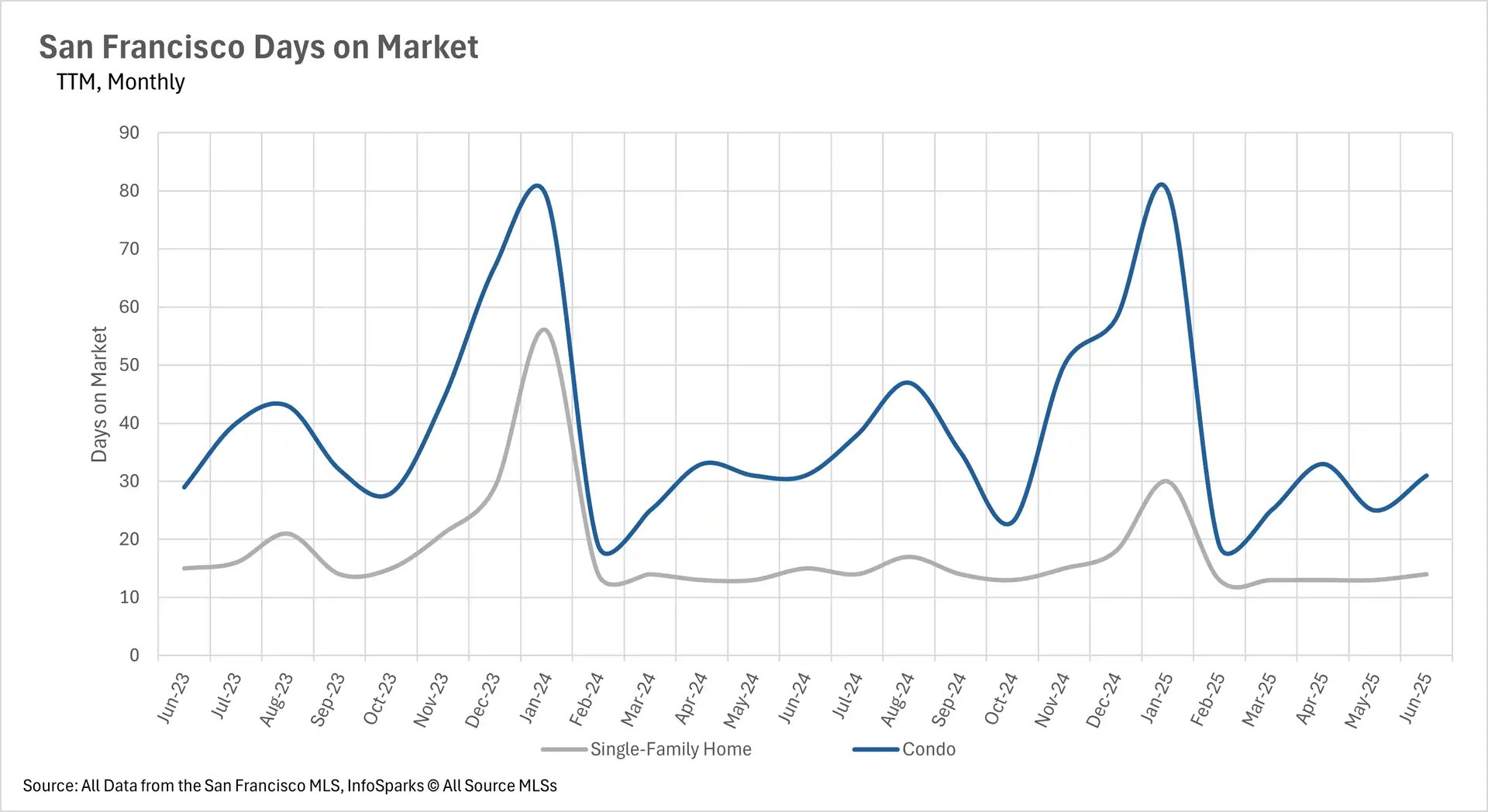

Days on market increase dramatically despite inventory declines

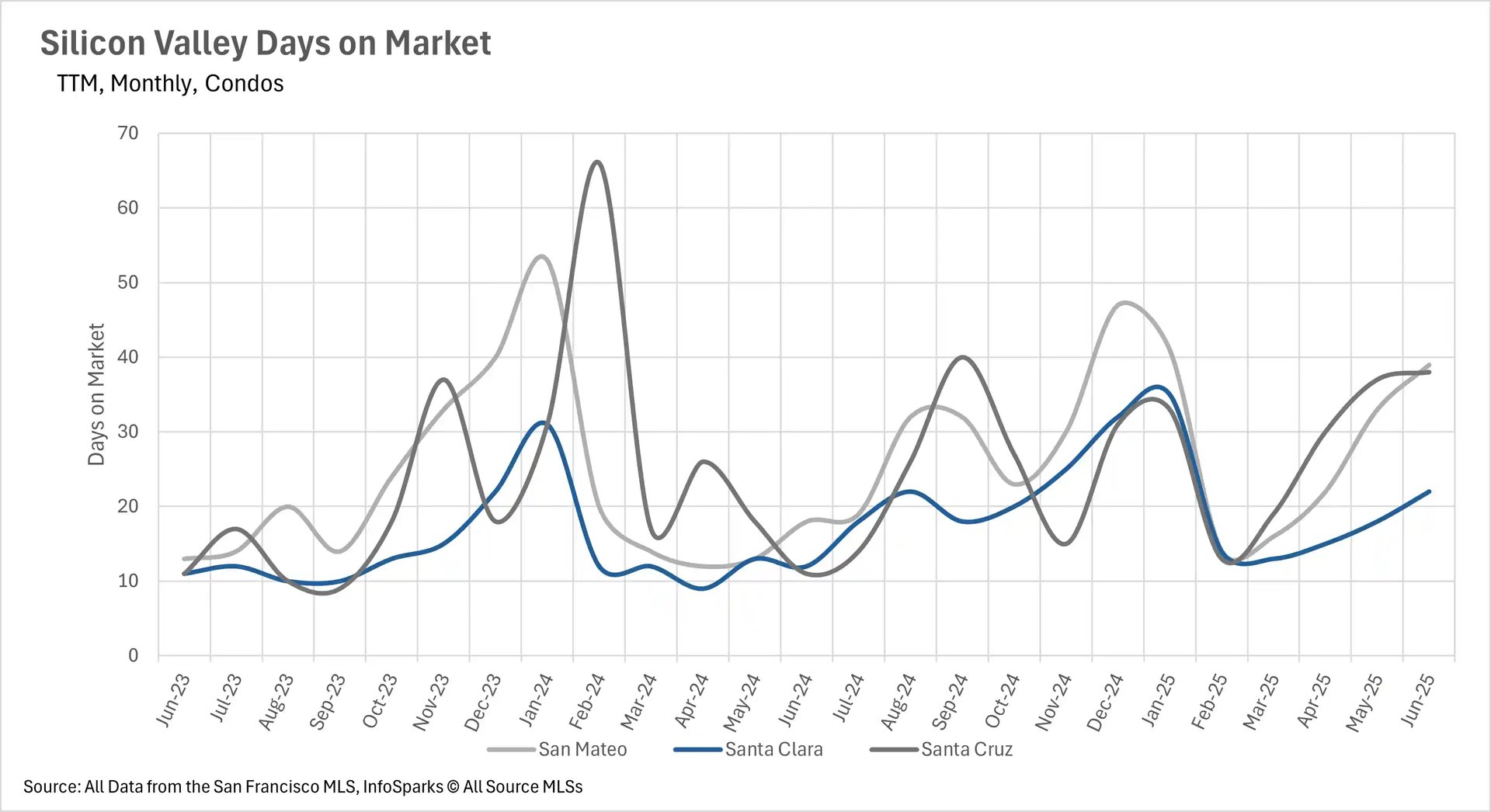

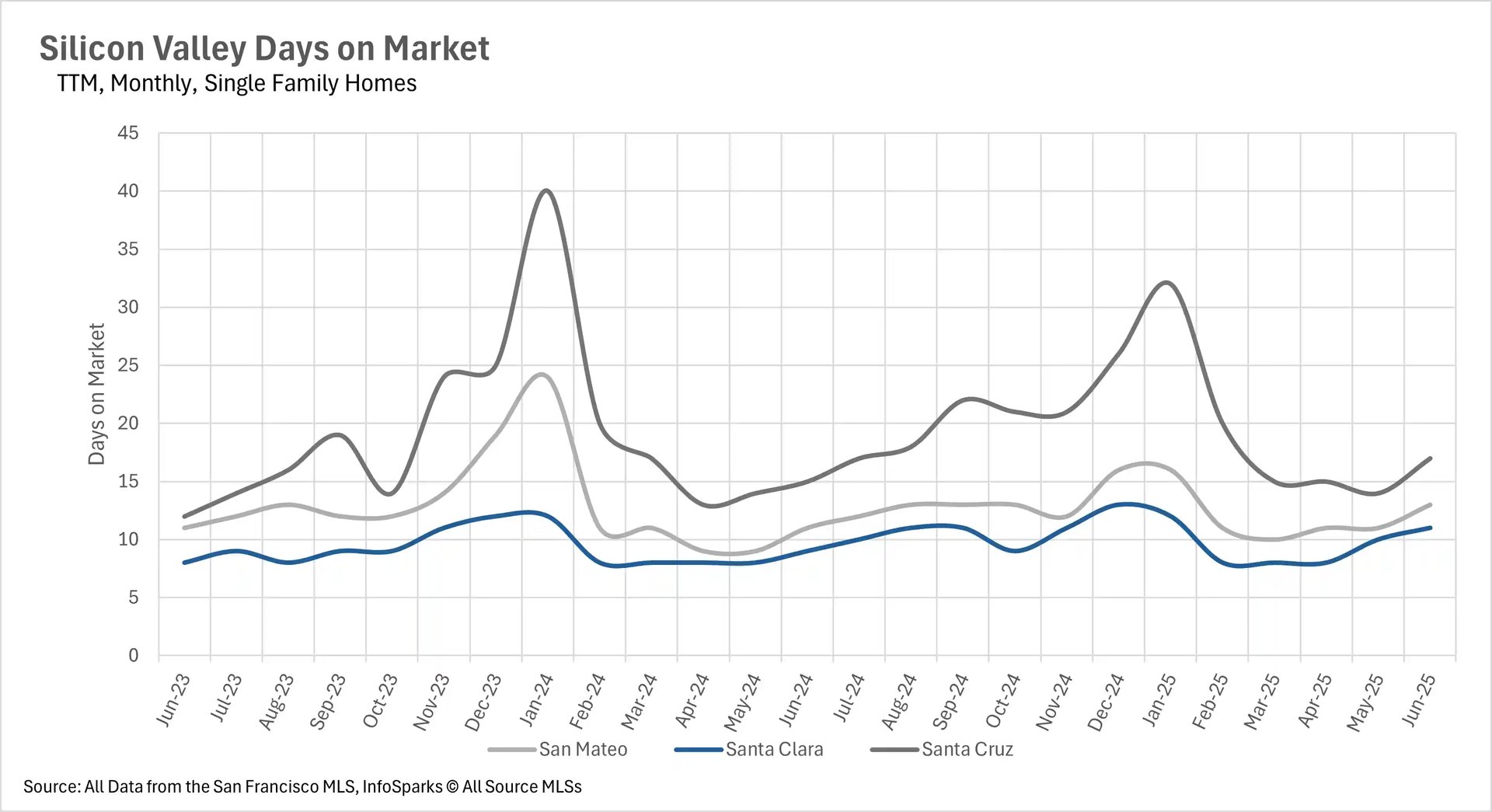

One of the most striking trends in June was the significant increase in days on market across all Bay Area regions, despite the substantial inventory declines. The North Bay saw the most consistent pattern with single-family homes spending 21.43% longer on market in Sonoma County, 25% longer in Marin County, 30.77% longer in Solano County, and 16.67% longer in Napa County year-over-year. Silicon Valley's condo market experienced the most dramatic increases, with Santa Cruz County condos spending 245.45% more time on market, San Mateo County condos up 116.67%, and Santa Clara County condos increasing 83.33%.

Even San Francisco, typically the Bay Area's fastest-moving market, saw single-family homes take 14 days on average (down 6.67% from last year) while condos remained flat at 31 days. The East Bay showed more modest but still significant increases of 25-35% more time on market year-over-year, though absolute numbers remained relatively quick with single-family homes selling in 15-17 days and condos in 25-31 days. This pattern suggests that while inventory is declining, buyer selectivity is increasing, creating a more deliberate purchasing environment.

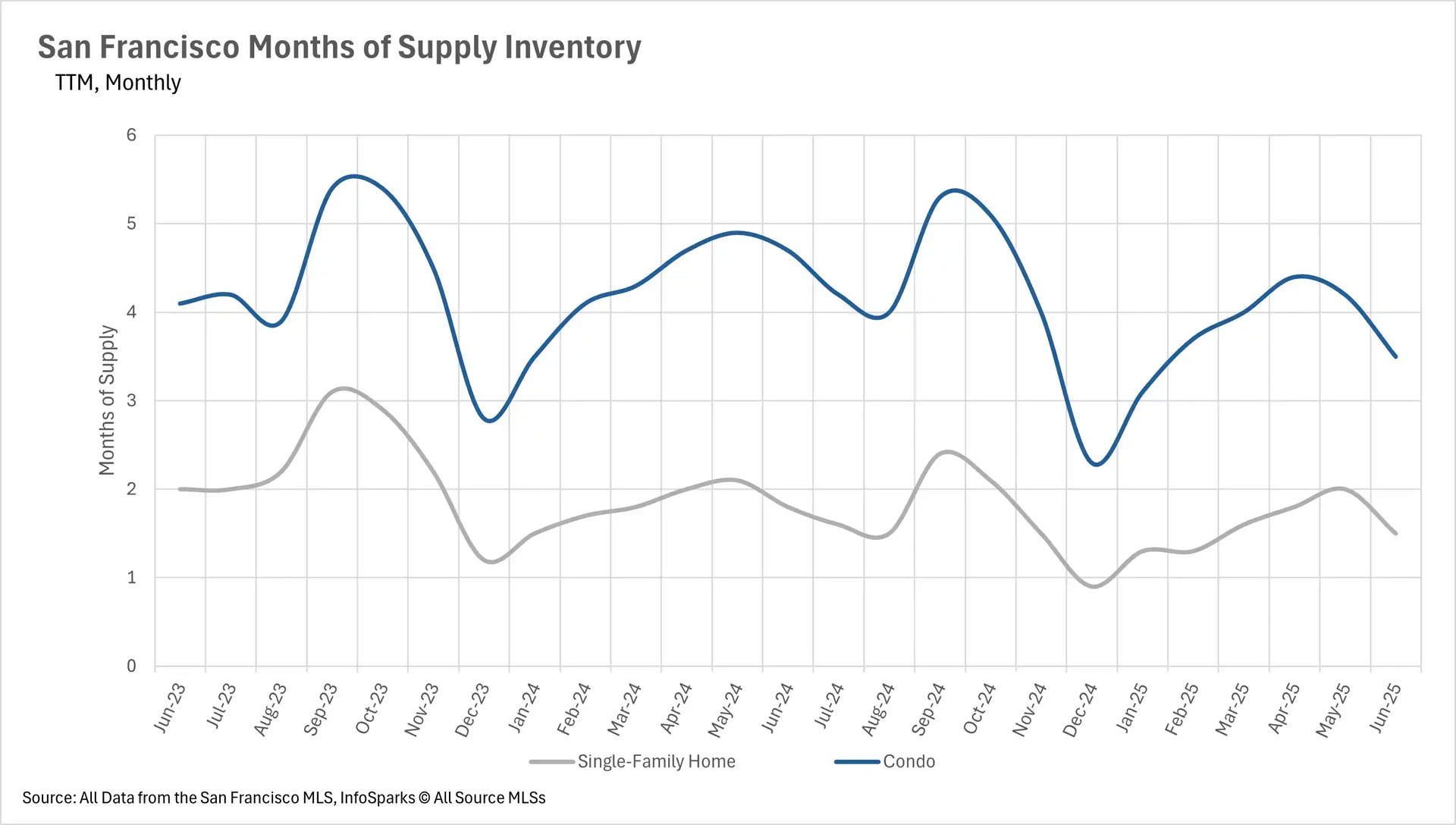

Market dynamics increasingly favor property type over geography

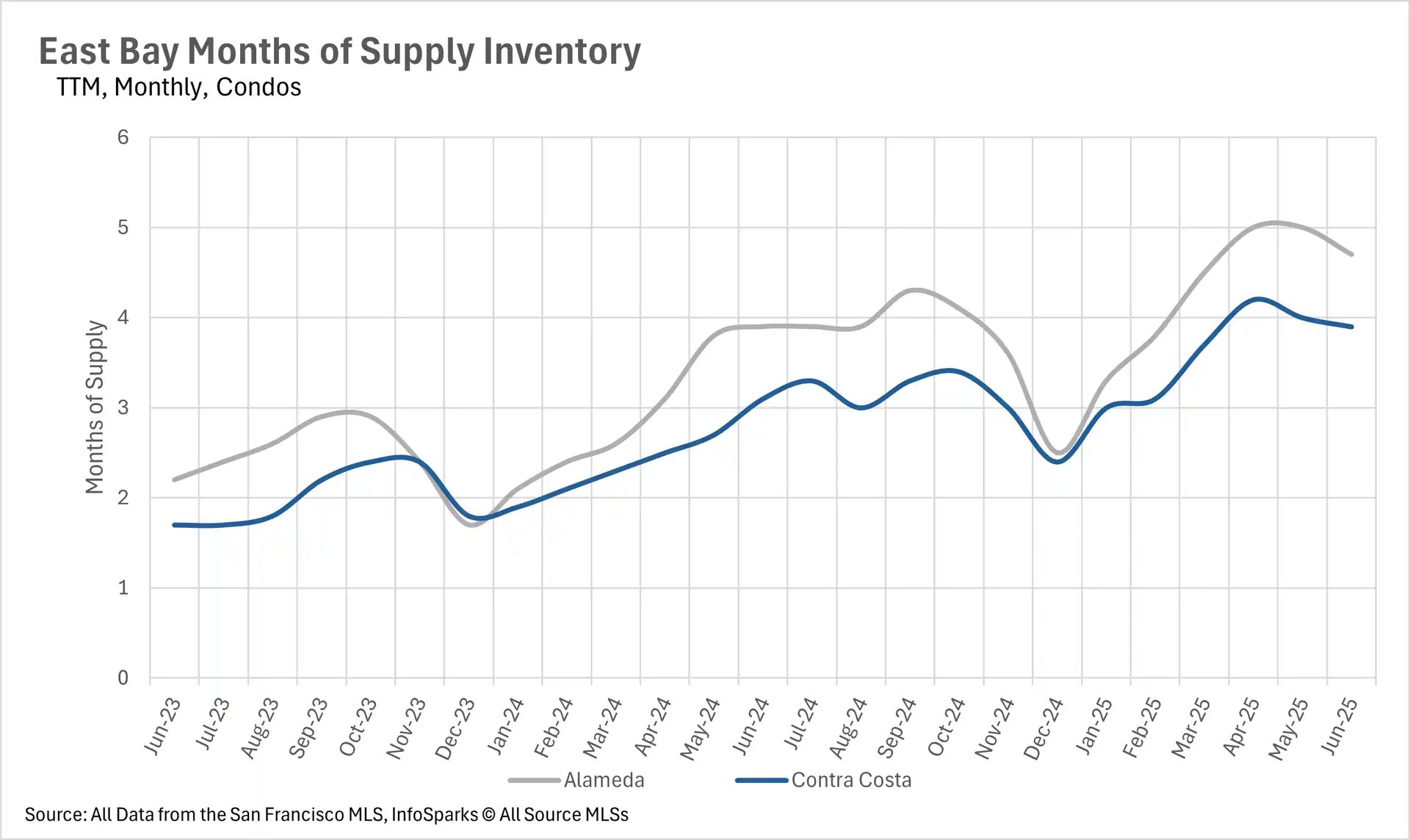

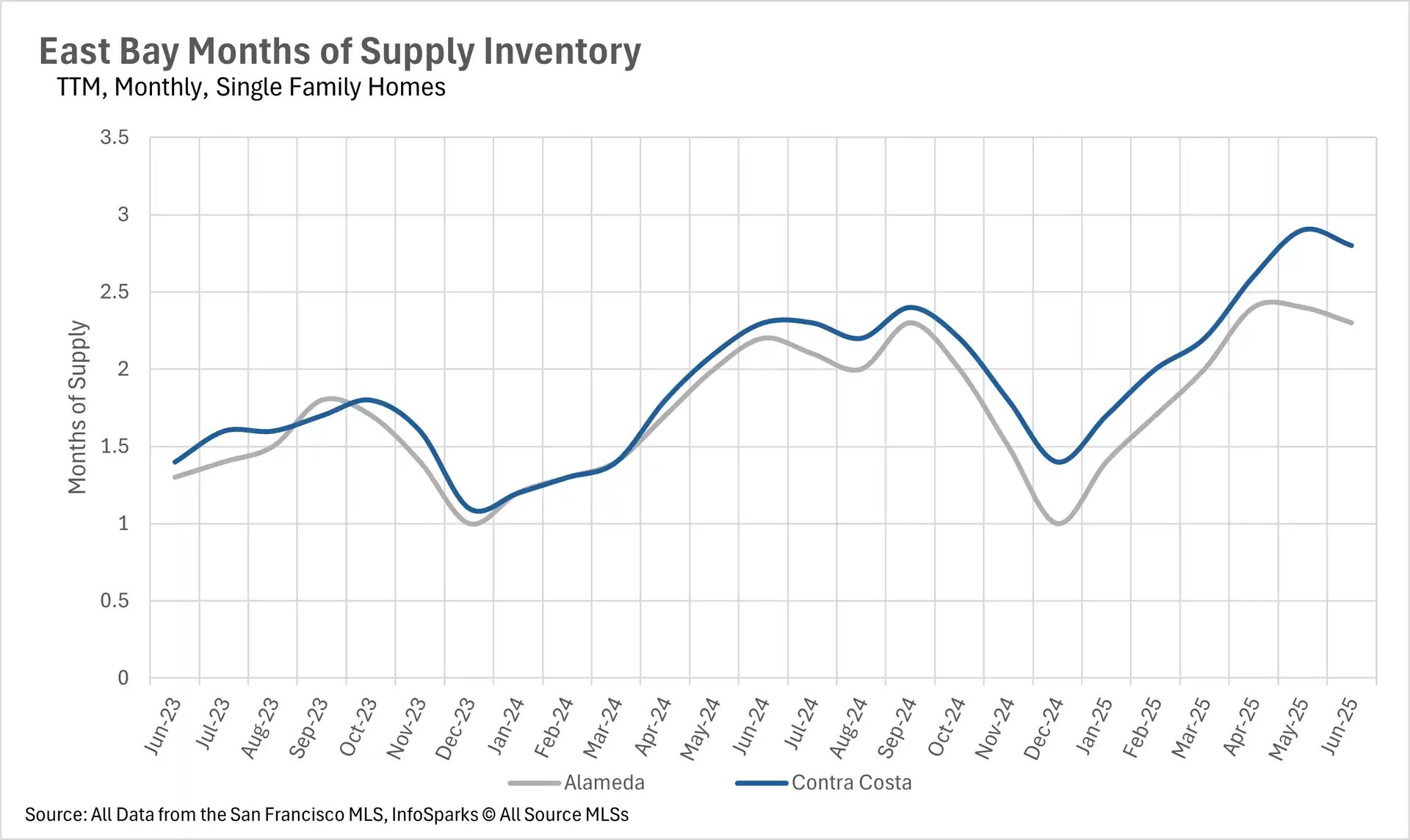

The months of supply inventory metric reveals a consistent Bay Area-wide pattern where single-family homes remain in seller's market territory while condos have shifted decisively toward buyer's markets. San Francisco exemplifies this trend with single-family homes at just 1.5 months of supply (strong seller's market) while condos sit at 3.5 months (buyer's market). Silicon Valley shows San Mateo and Santa Clara Counties maintaining seller's markets for single-family homes at 1.9 and 1.7 months respectively, while all three Silicon Valley counties present buyer's markets for condos ranging from 3.4 to 5.5 months of supply.

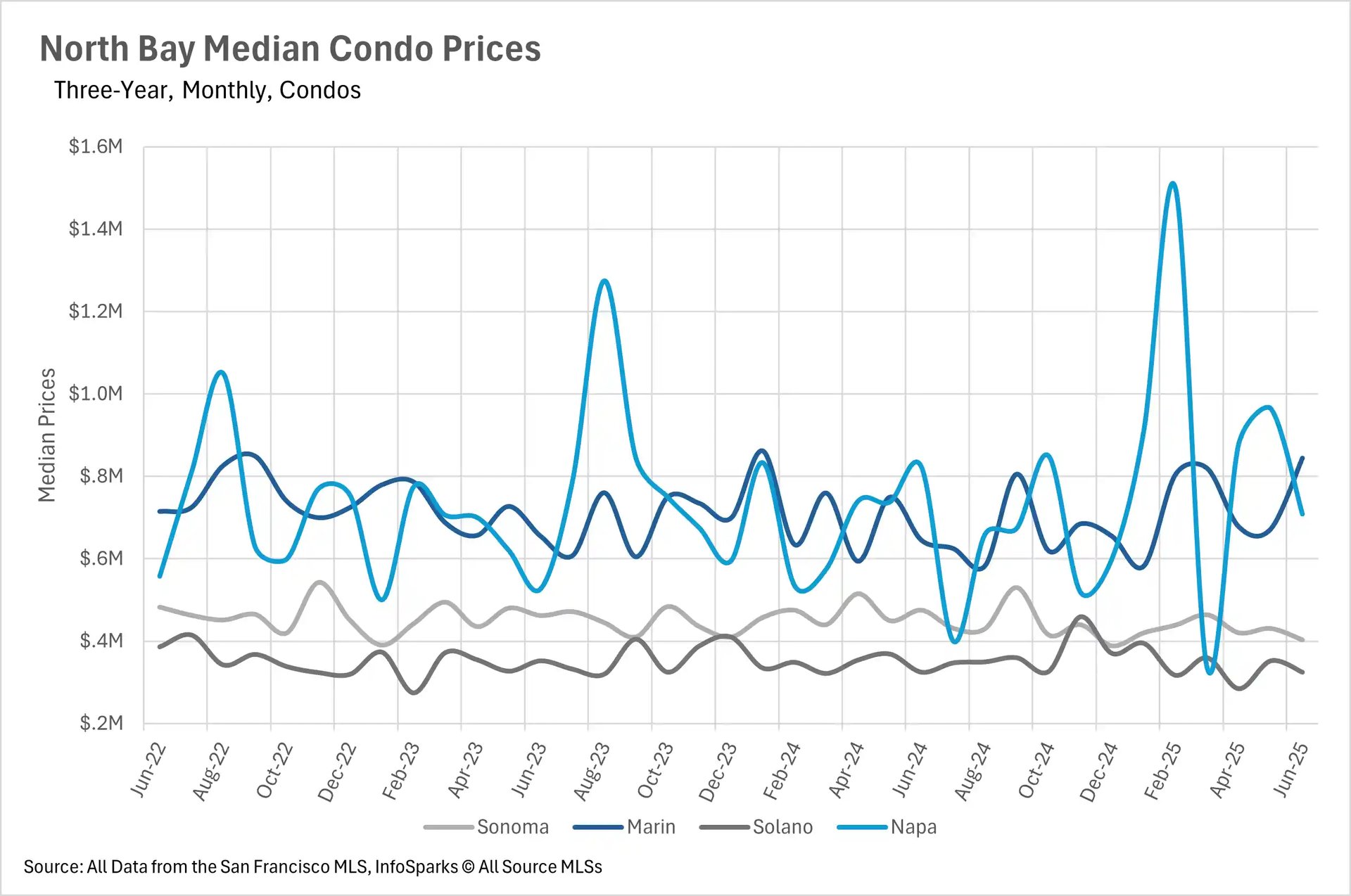

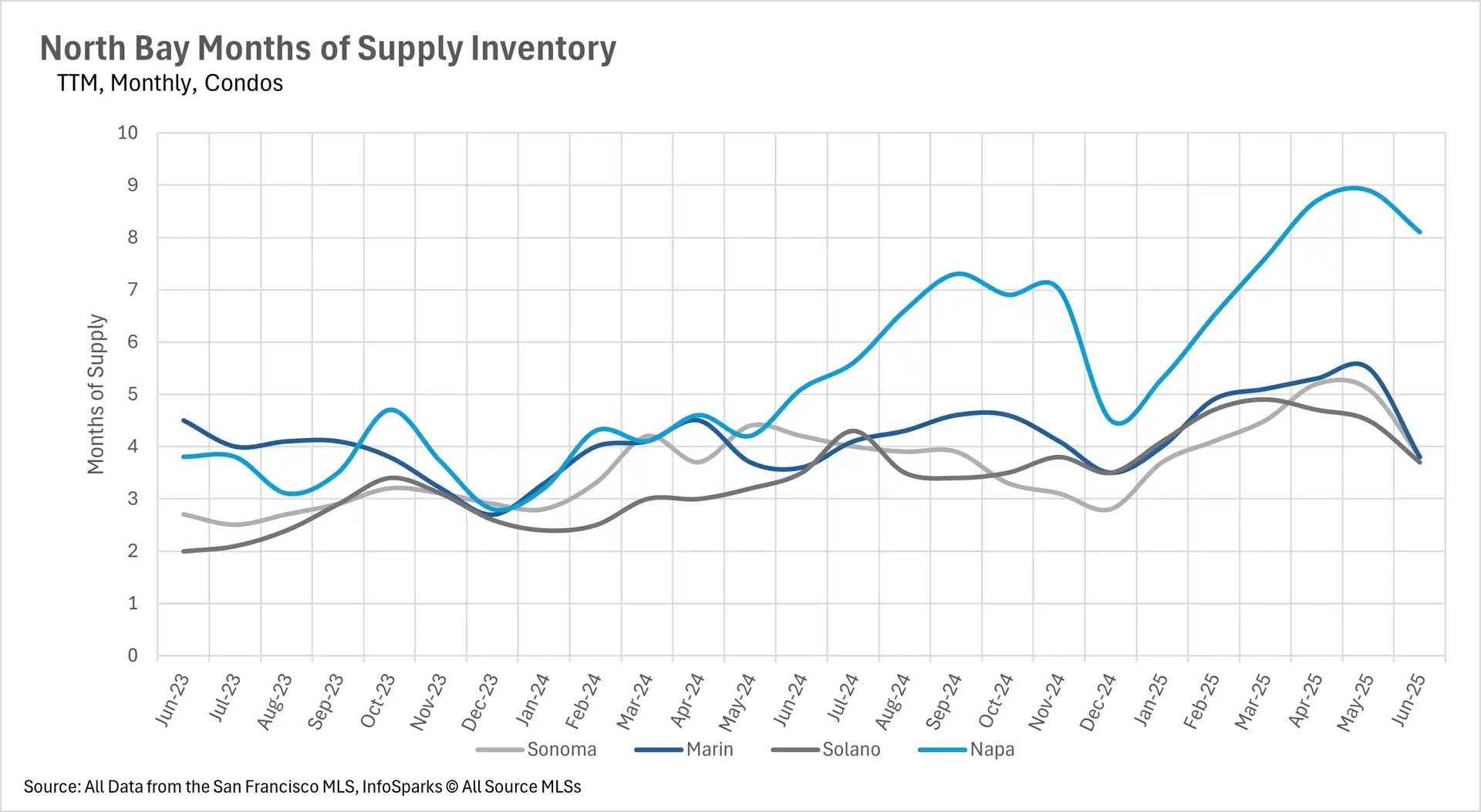

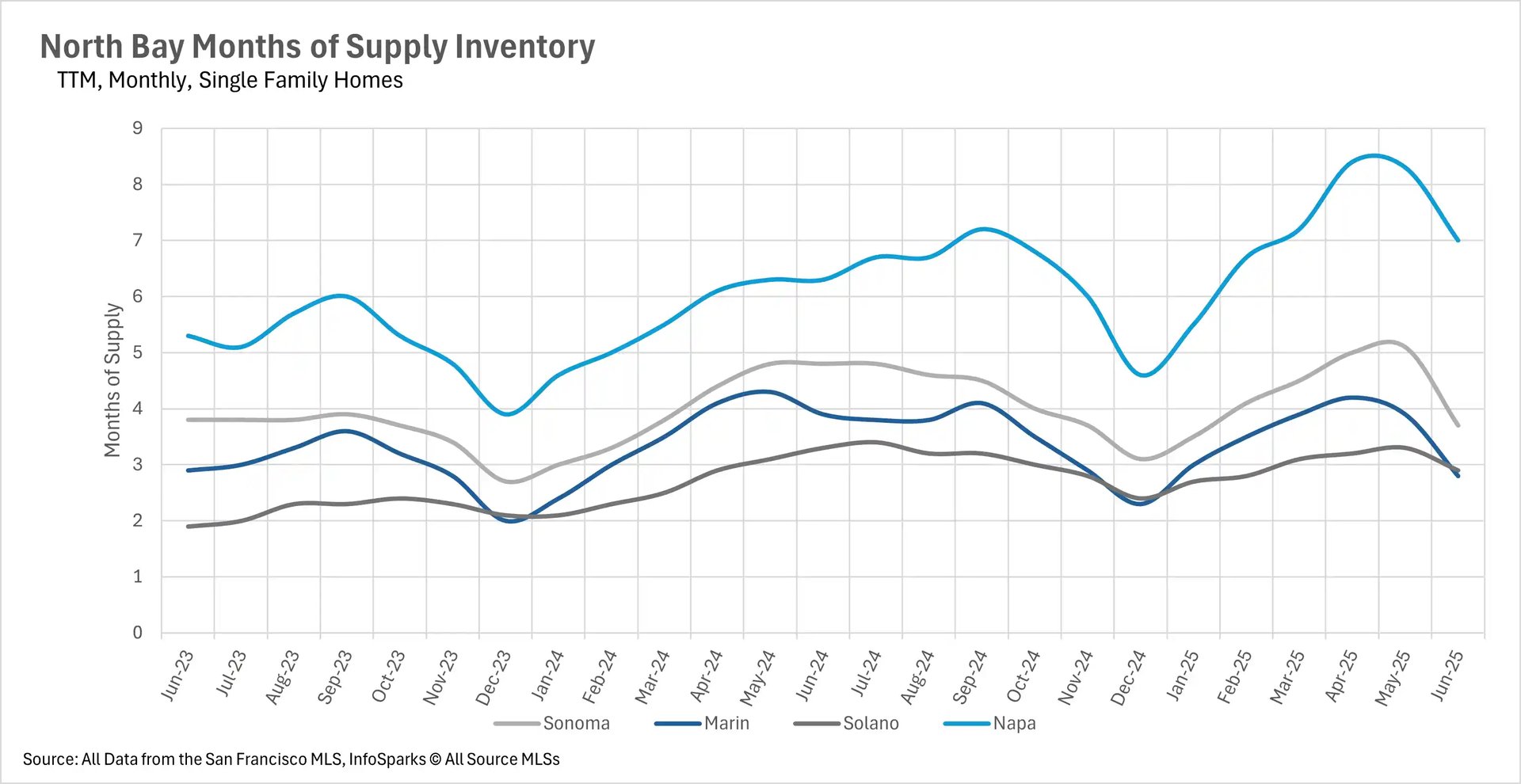

The East Bay maintains its traditional split with single-family homes at 2.3 months in Alameda and 2.8 months in Contra Costa (seller's markets), while condos favor buyers with 4.7 and 3.9 months respectively. The North Bay shows the most variation, with Marin and Solano Counties approaching balanced markets for single-family homes at 2.8 and 2.9 months, while Sonoma (3.7 months) and Napa (7 months) favor buyers. However, all North Bay counties present buyer's markets for condos, with Napa County showing an extreme 8.1 months of condo supply. This pattern suggests that across the Bay Area, single-family homes retain their premium status and seller advantage, while the condo market presents increasingly attractive opportunities for buyers willing to navigate longer timelines and more inventory choices.