I get it—everything feels like it’s gotten more expensive these days. Groceries, gas, utilities—it’s enough to make anyone start to worry. And if you’re keeping an eye on the housing market, those rising costs can feel like they’re leading us down a familiar, uncomfortable path. You might even wonder if homeowners are starting to fall behind on their mortgage payments, sparking fears of another wave of foreclosures.

But let’s take a step back and look at what’s actually happening. The good news is that the latest foreclosure data shows we’re not heading for any kind of crash. Things look very different than they did back in 2008.

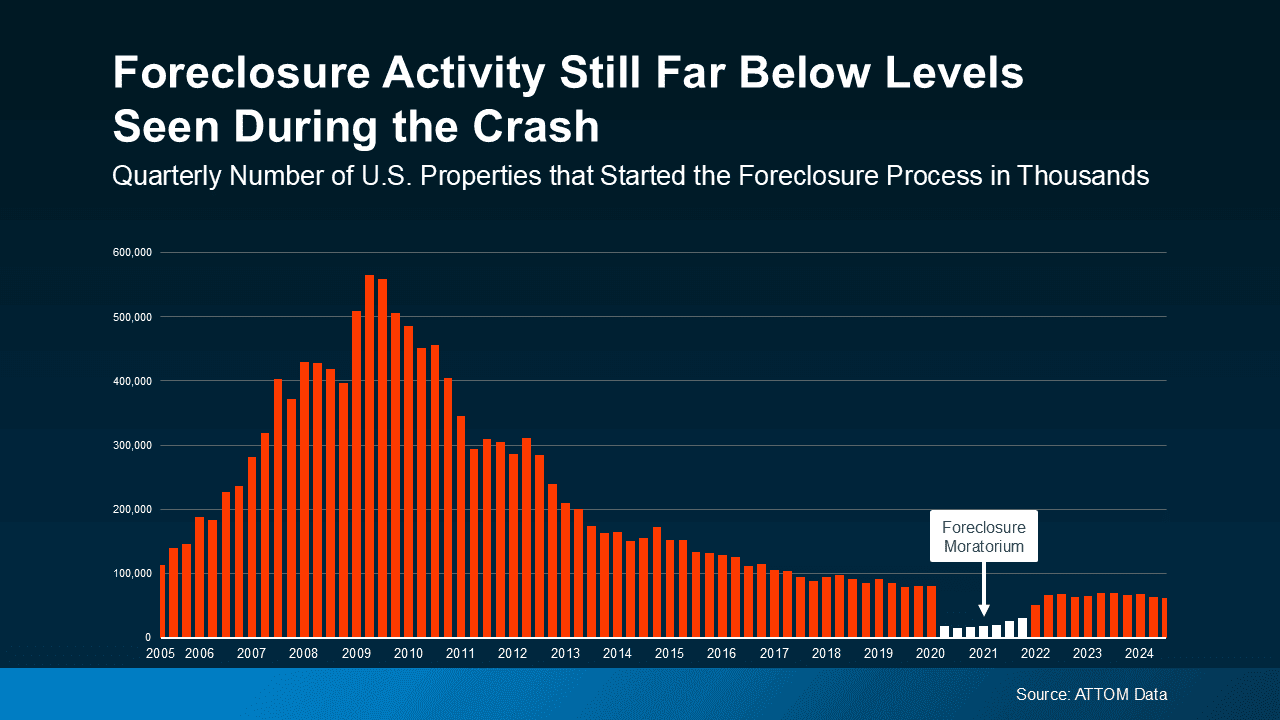

How Today’s Market Isn’t 2008 All Over Again

We all remember what happened back then, right? The market tanked, foreclosures spiked, and a lot of people got burned. So, it’s easy to jump to that worst-case scenario when we start seeing foreclosure headlines again. But the reality is, this is a very different situation.

Take a look at the latest numbers, and you’ll see that foreclosure filings are nowhere near what they were in the aftermath of 2008. Even though there’s been a slight uptick since 2020 and 2021, it’s important to remember that back then, we had a foreclosure moratorium in place to help struggling homeowners. That’s why the numbers were so unusually low for a couple of years. Now that things are moving again, we’re seeing a return to more typical levels, but it’s still far below the crisis we experienced over a decade ago.

Why Fewer Foreclosures Are Happening (Even with Higher Costs)

Now, you might be thinking: "Wait, how can we have fewer foreclosures when everything is so expensive?" It’s a valid question, especially with the cost of living being what it is. But one of the key differences between now and 2008 is that homeowners today are in a much stronger position financially, thanks to the equity they’ve built up in their homes.

Unlike the housing crash, when people were upside down on their mortgages—meaning they owed more than their homes were worth—most homeowners today have an "equity cushion." This safety net is helping people avoid foreclosure, even if they hit financial bumps in the road. As Bankrate points out

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”

Think of it like this: if someone is struggling to make their mortgage payments now, they often have the option to sell their home, pay off their mortgage, and still walk away with money in their pocket. Back in 2008, that wasn’t the case for a lot of folks. They were trapped in homes they couldn’t sell because the value had plummeted. That’s not happening today.

What’s Next for the Housing Market?

Look, I’m not going to sugarcoat it—things are tough out there right now. The rising cost of everything from gas to groceries is making it harder for many families to balance their budgets. But that doesn’t mean we’re heading toward another foreclosure crisis. The equity that homeowners have built up is acting as a buffer, keeping foreclosure filings lower than you might expect given the financial pressure people are under.

What’s more, homeowners today have more options. They’re not stuck the way many were back in 2008. If things get tough, they can sell, downsize, or refinance. And that’s a huge reason why we’re not going to see a wave of foreclosures crashing into the market.

Bottom Line

Yes, things are more expensive these days. And sure, it’s natural to worry about how that might affect the housing market. But the data just doesn’t support the idea that we’re heading for another foreclosure crisis. Homeowners today are sitting on much more equity than they were back in 2008, and that equity is giving them more control over their financial situations. So, take a deep breath—this is not 2008 all over again.