If you prefer to bypass The Big Story and jump straight to the Local Market Report, click here.

The Big Story

2024 wrap-up and the year ahead

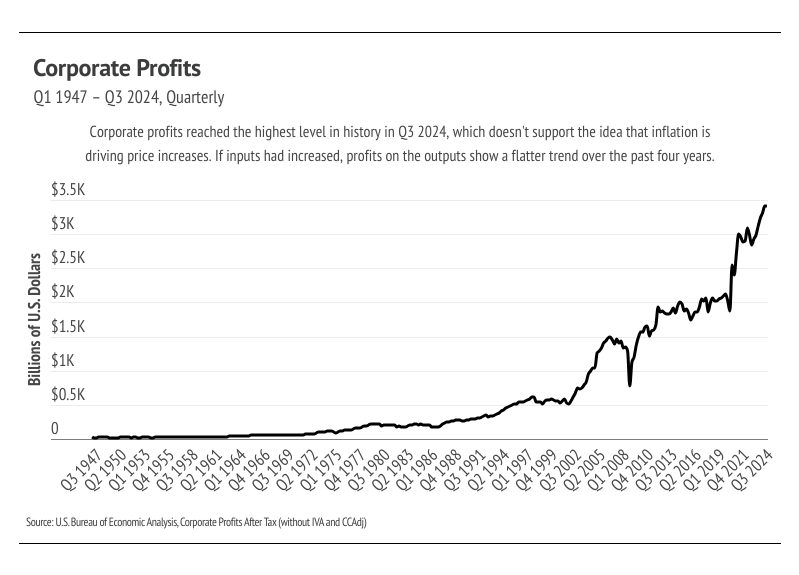

- Elevated mortgage rates dominated the housing market in 2024, and 2025 may look similar if inflation starts to ramp up again. Corporations are already increasing prices before more tariffs kick in despite record profits over the past four years.

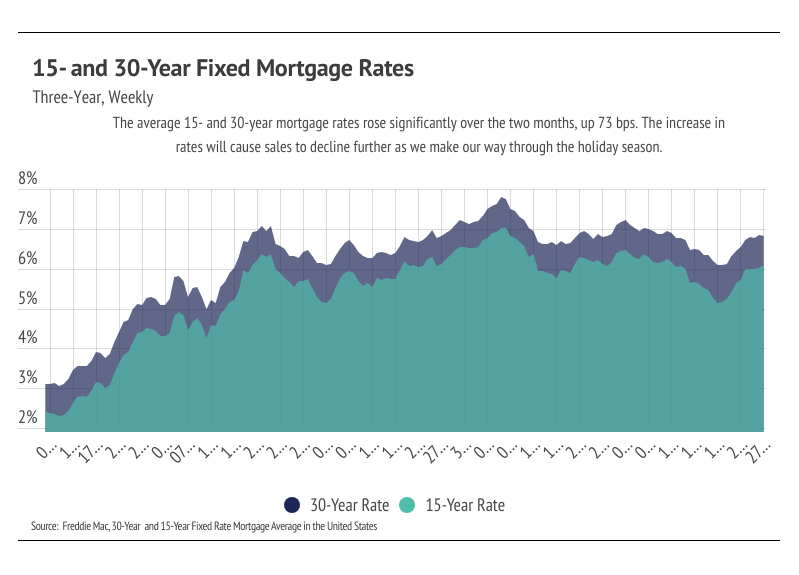

- During November 2024, the average 30-year mortgage rate rose 9 bps, adding to the 64 bps increase in October. Since September 2024, the Fed has cut rates by 75 bps, and we expect another 25 bps cut at their December meeting, barring a significant uptick in November inflation data.

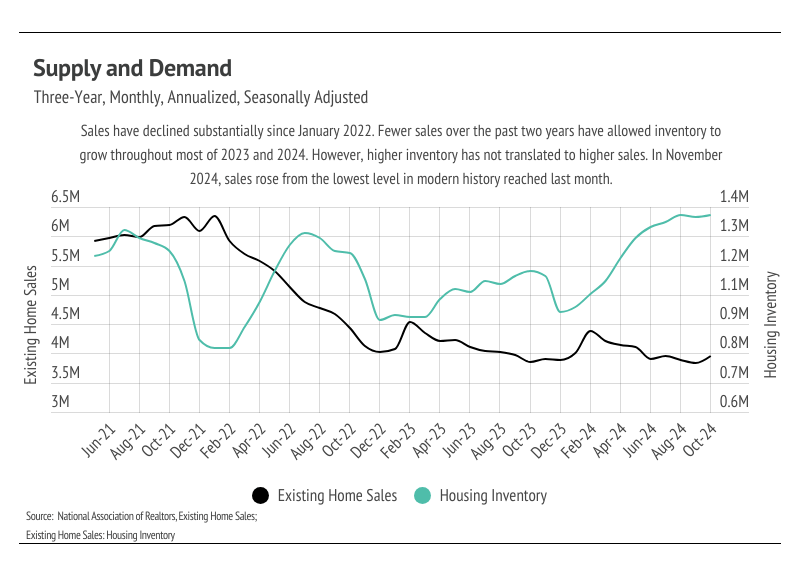

- Sales rose 3.4% month over month, up slightly from last month, which saw the lowest level of sales in modern history. At the same time, inventory rose to its highest level since 2020. Higher inventory levels created more opportunity for sales, although we don’t expect sales volume to increase significantly until spring 2025.

Higher mortgage rates and higher prices

Big Story Data

The Local Lowdown

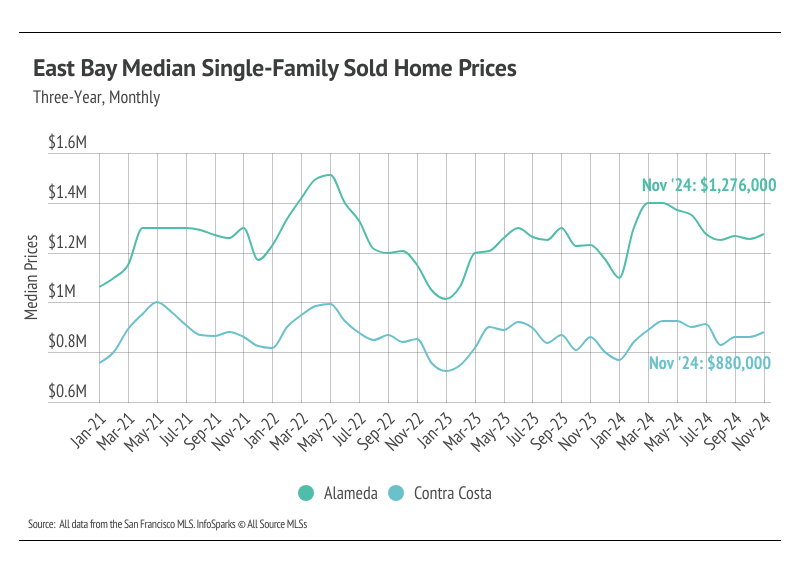

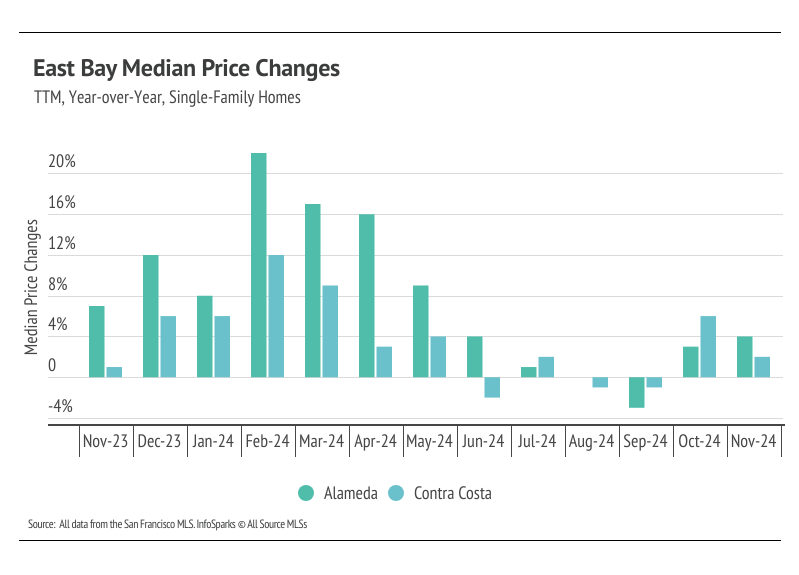

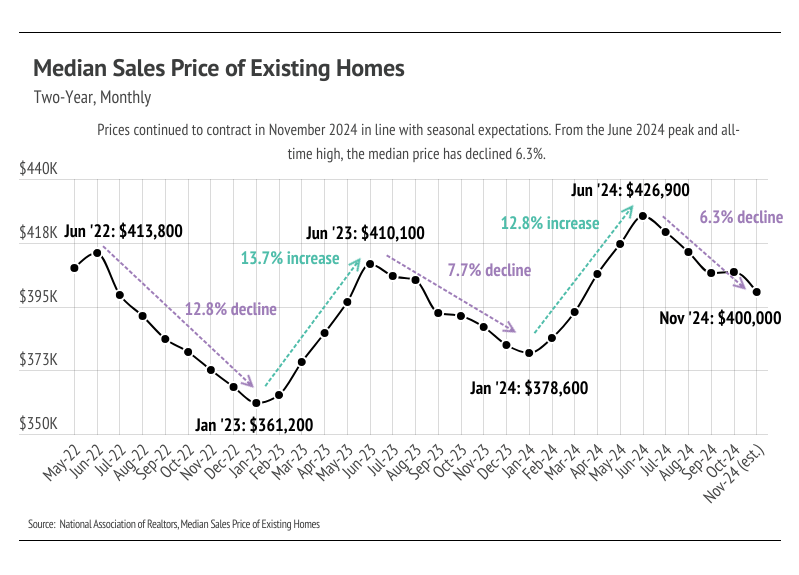

- Median home prices rose slightly in November, which is normal for the East Bay this time of year. Prices generally contract in the second half of the year, and we expect prices to decline through January 2025.

- Total inventory decreased 24.5% month over month, as new listings fell more than sales. We expect inventory to decline and the overall market to slow over the next two months.

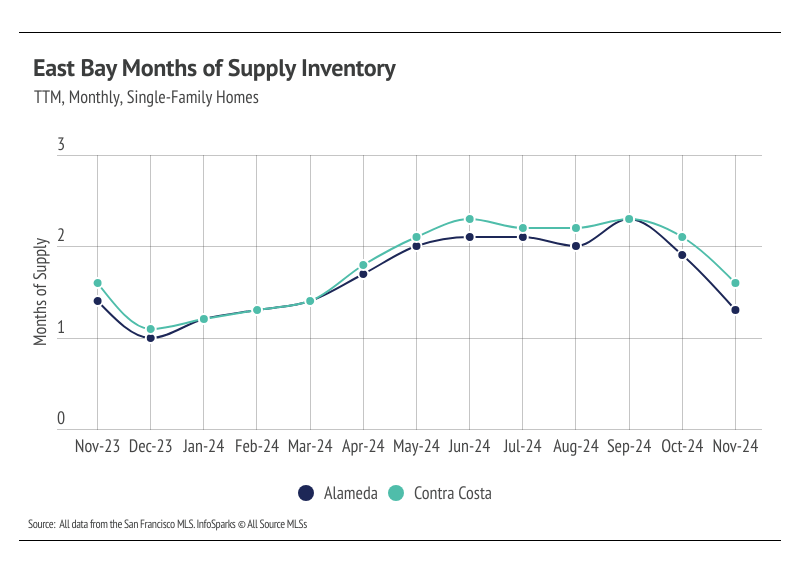

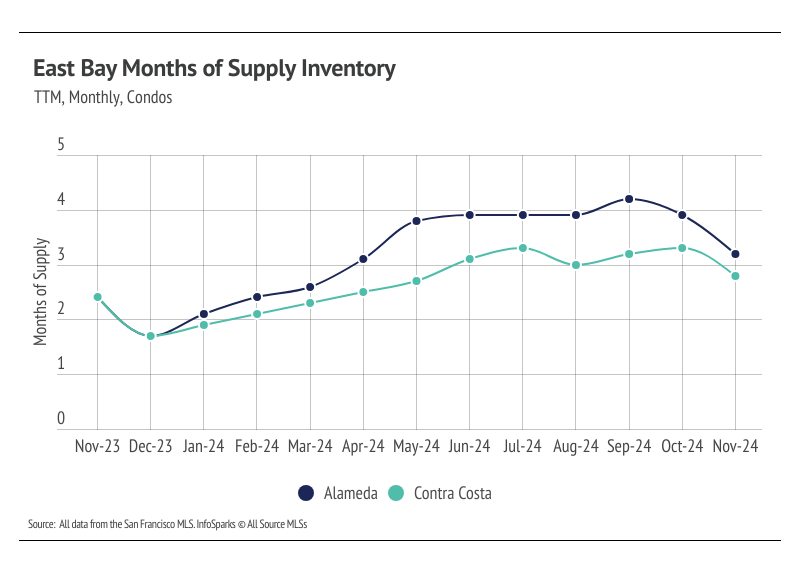

- Months of Supply Inventory still indicates a sellers’ market in the East Bay for single-family homes, but for condos, MSI implies the market is now more balanced.

Median home prices rose slightly month over month in the East Bay

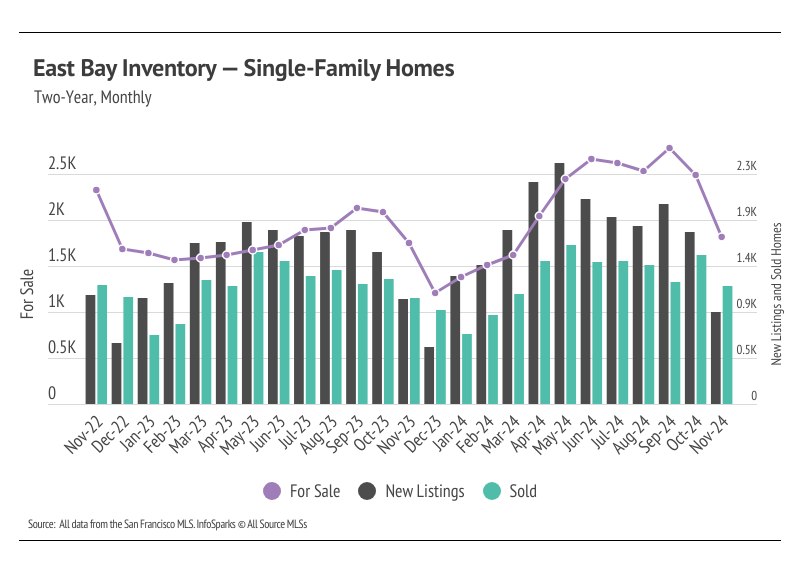

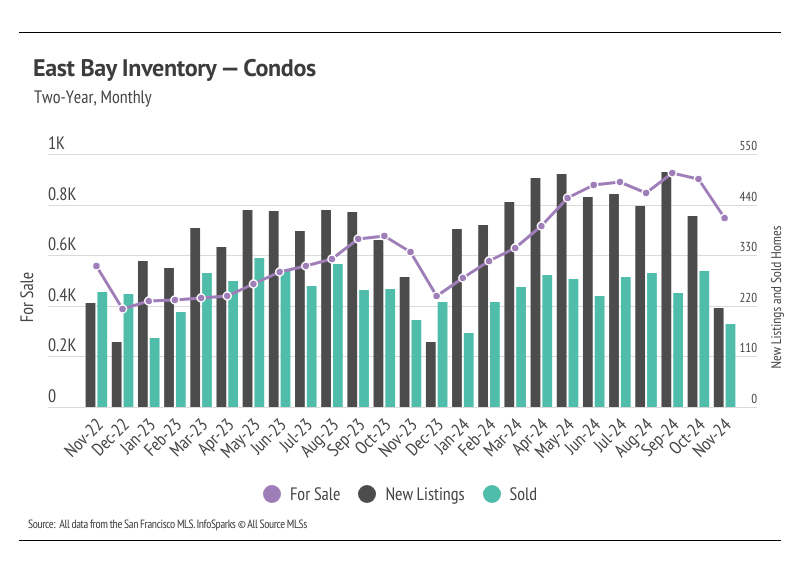

Inventory, new listings, and sales fell

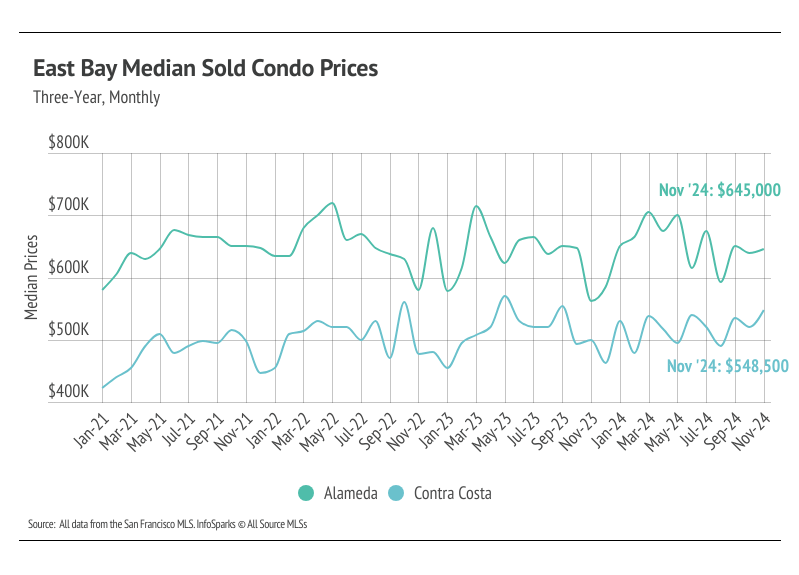

The 2024 housing market has looked progressively healthier with each passing month. We’re far enough into the year to know that inventory levels are about as good as we could’ve hoped, although single-family home inventory is still lower than we would like. In 2023, single-family home and condo inventory followed fairly typical seasonal trends, but at significantly depressed levels. Low inventory and fewer new listings slowed the market considerably last year. Even though sales volume this year was similar to last, far more new listings have come to the market, which has allowed inventory to grow. Condo inventory even reached a four-year high in September before declining in October and November. For single-family homes, inventory is up slightly year over year, but inventory fell significantly month over month as new listings declined at a greater magnitude than sales.

Typically, inventory begins to increase in January or February, peaking in July or August before declining once again from the summer months to the winter. It’s looking like 2024 inventory, sales, and new listings will resemble historically seasonal patterns, and at more normal levels than last year.

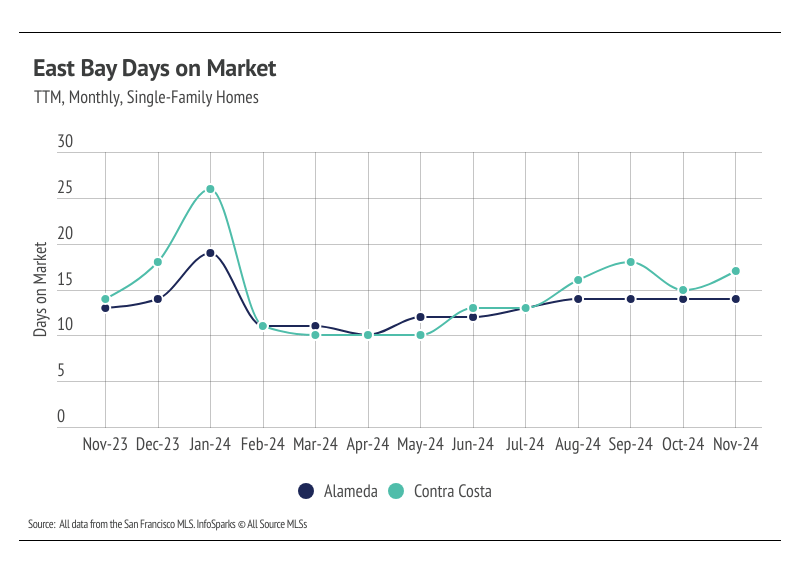

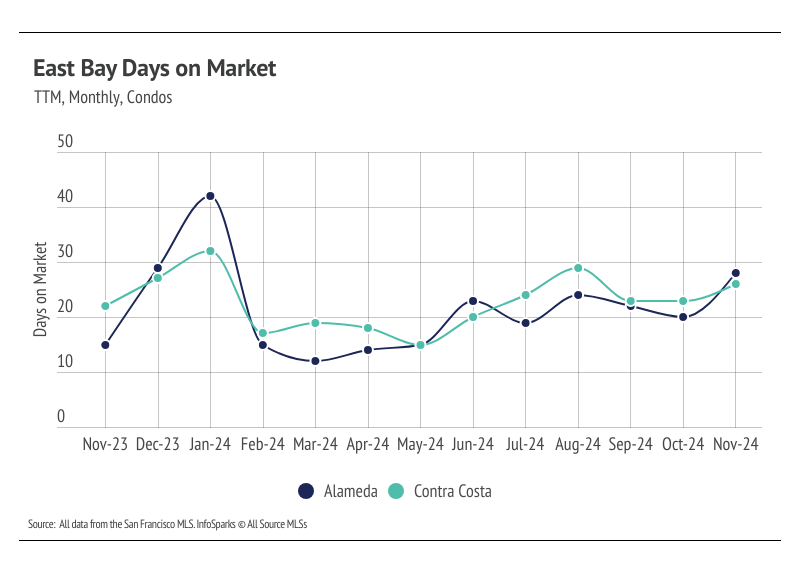

Months of Supply Inventory in November 2024 indicated a sellers’ market for single-family homes and a balanced market for condos

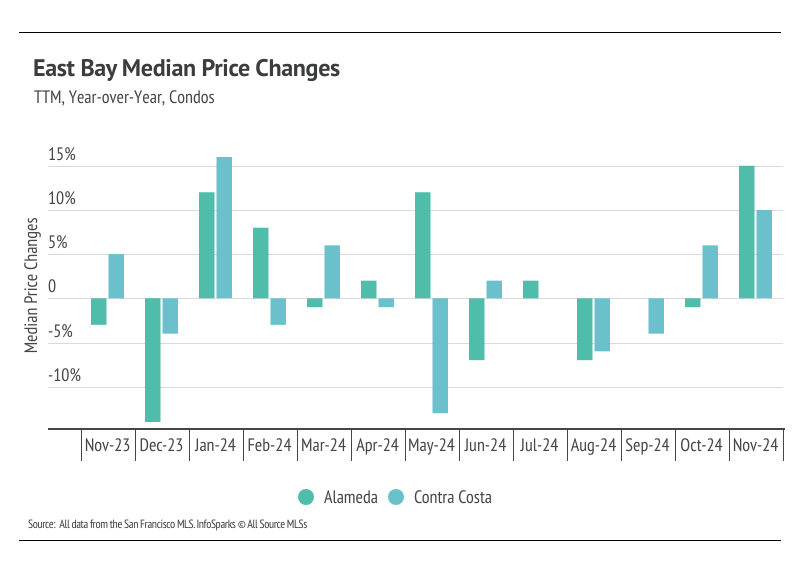

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The East Bay market tends to favor sellers, especially for single-family homes, which is reflected in its low MSI. For condos, MSI has trended higher in 2024, causing a shift from a sellers’ market to a buyers’ market, then back to balanced. Although single-family home MSI has moved slightly higher in 2024, it’s still low, indicating a sellers’ market.

Local Lowdown Data