The Local Lowdown

Quick Take:

- Bay Area real estate markets show stark contrasts in May, with San Francisco surging while Silicon Valley's growth streak breaks and North Bay prices decline.

- Inventory dynamics vary dramatically across regions, East Bay and Silicon Valley see massive increases while San Francisco and North Bay experience sharp declines.

- The region's housing markets are increasingly polarized, with single-family homes generally favoring sellers while condo markets present significant opportunities for buyers.

- Despite varying market conditions, homes are selling relatively quickly throughout most of the Bay Area, though condos are taking considerably longer in some areas.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

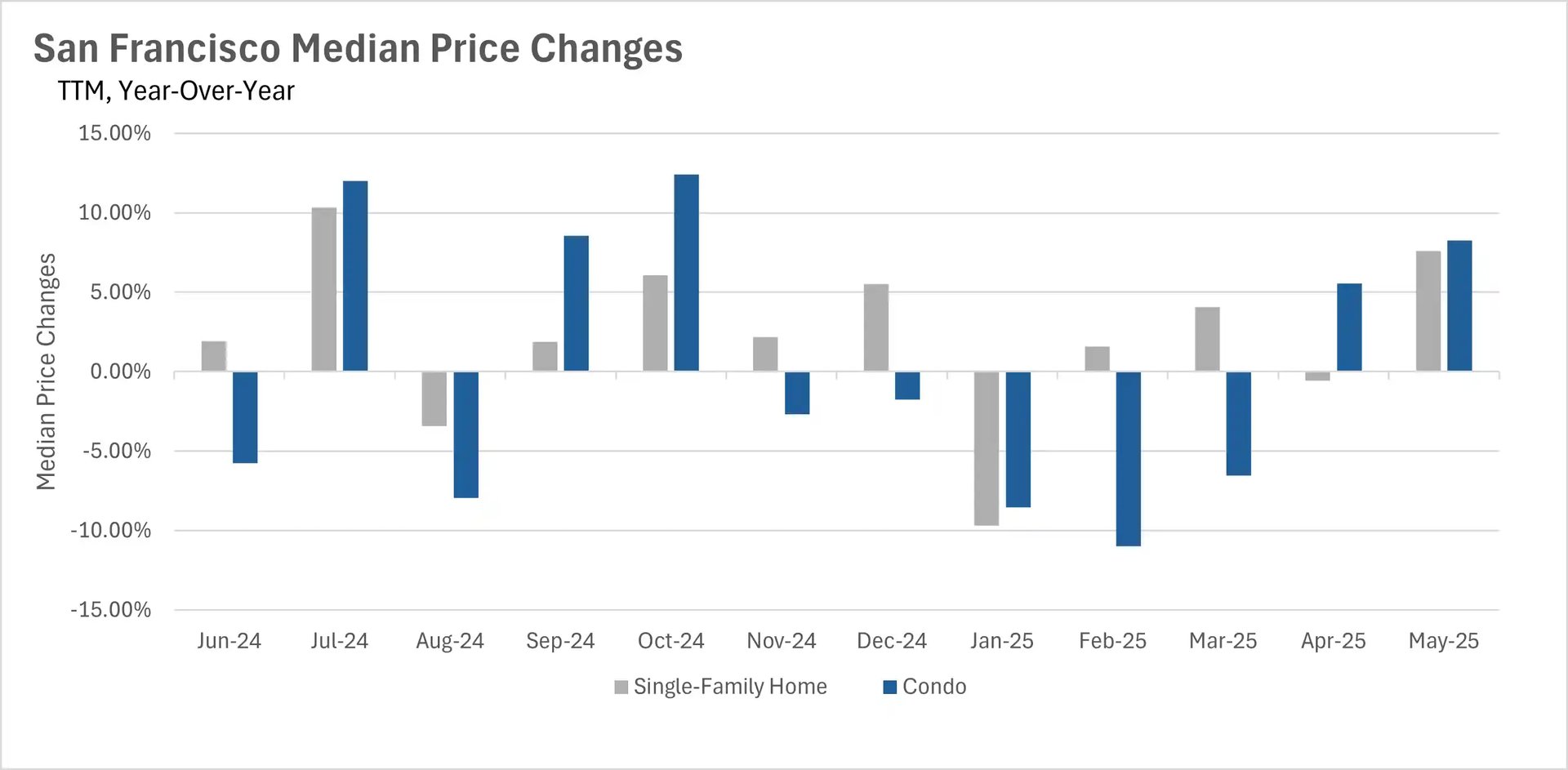

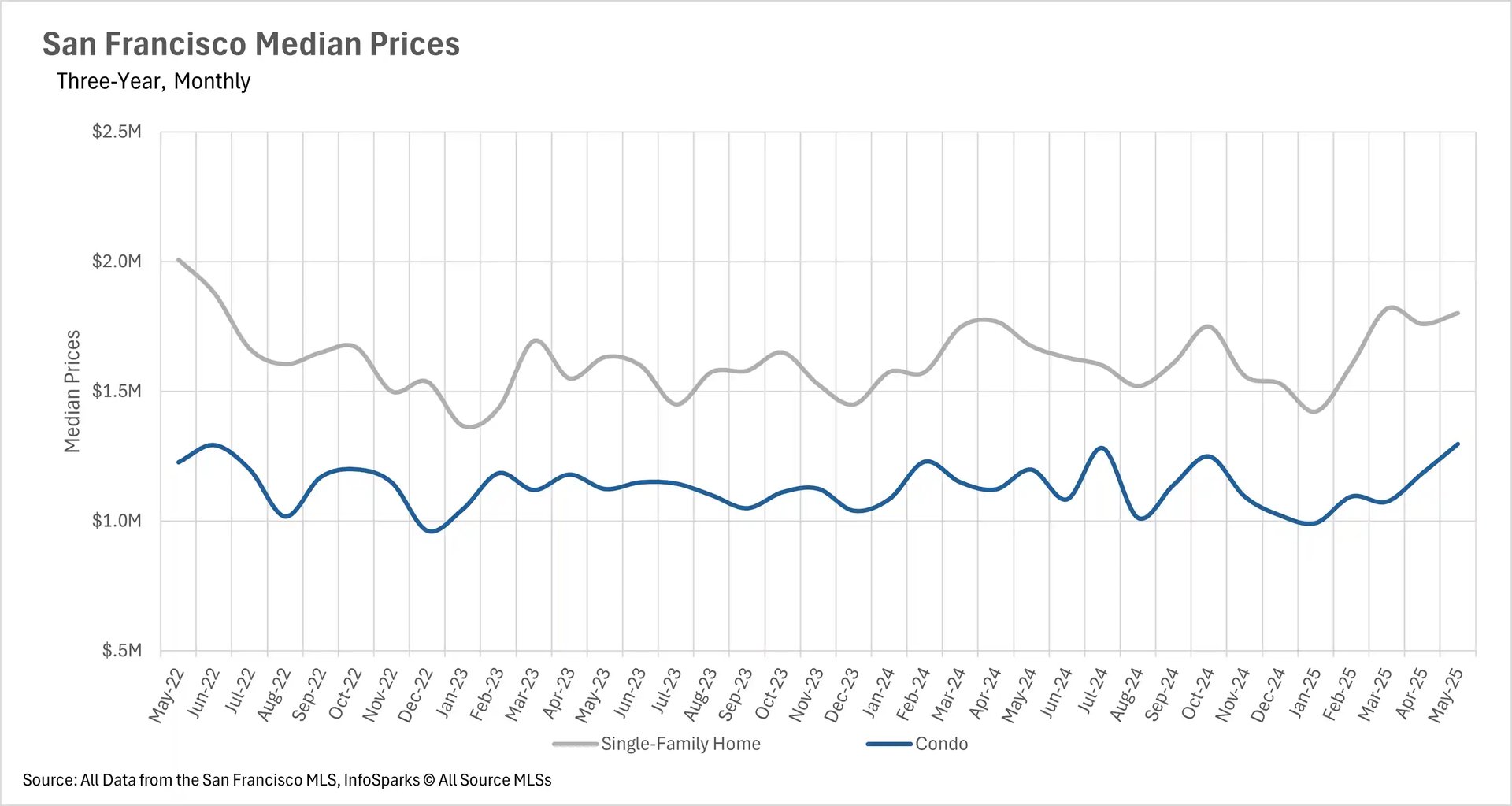

San Francisco leads price growth while other regions cool

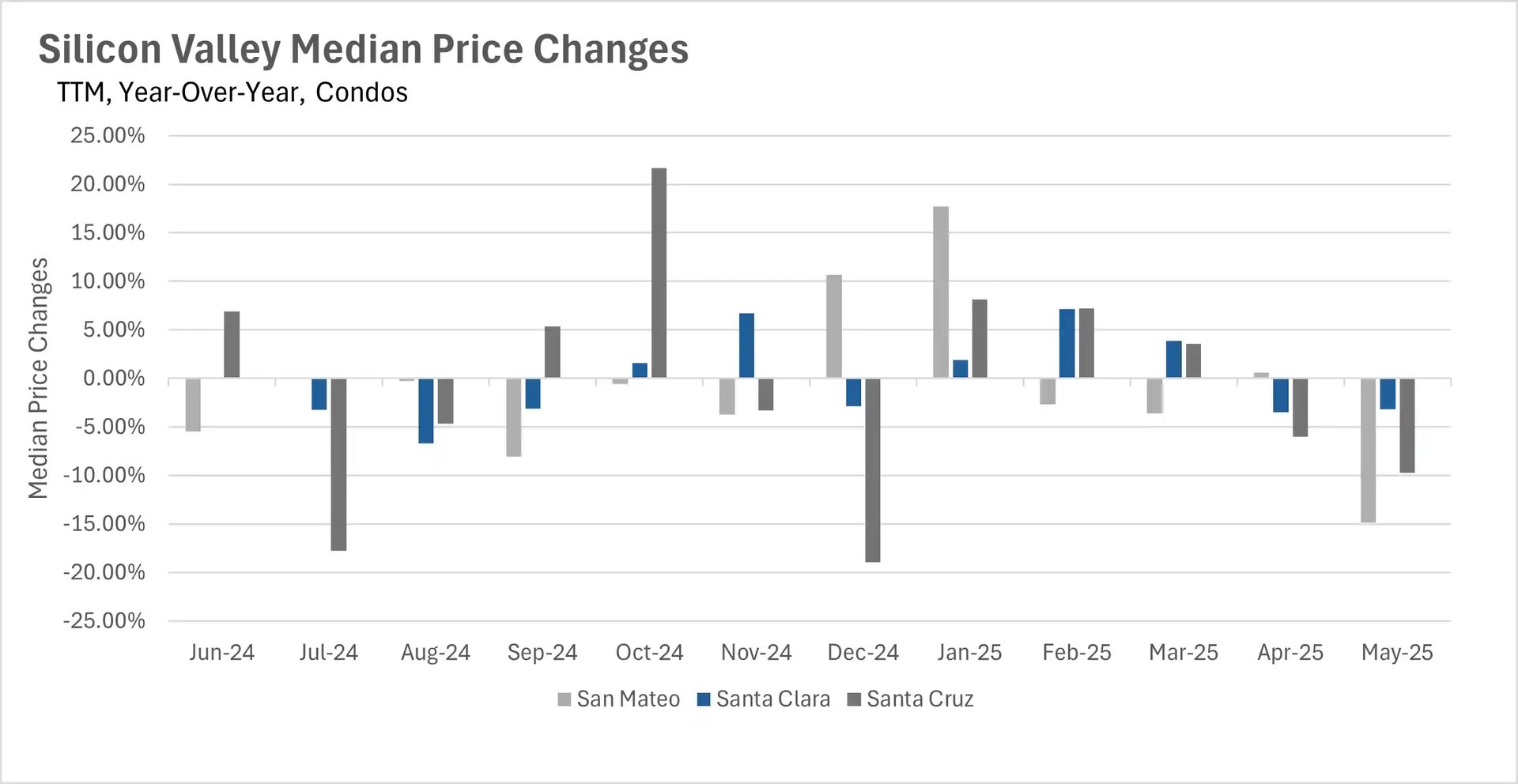

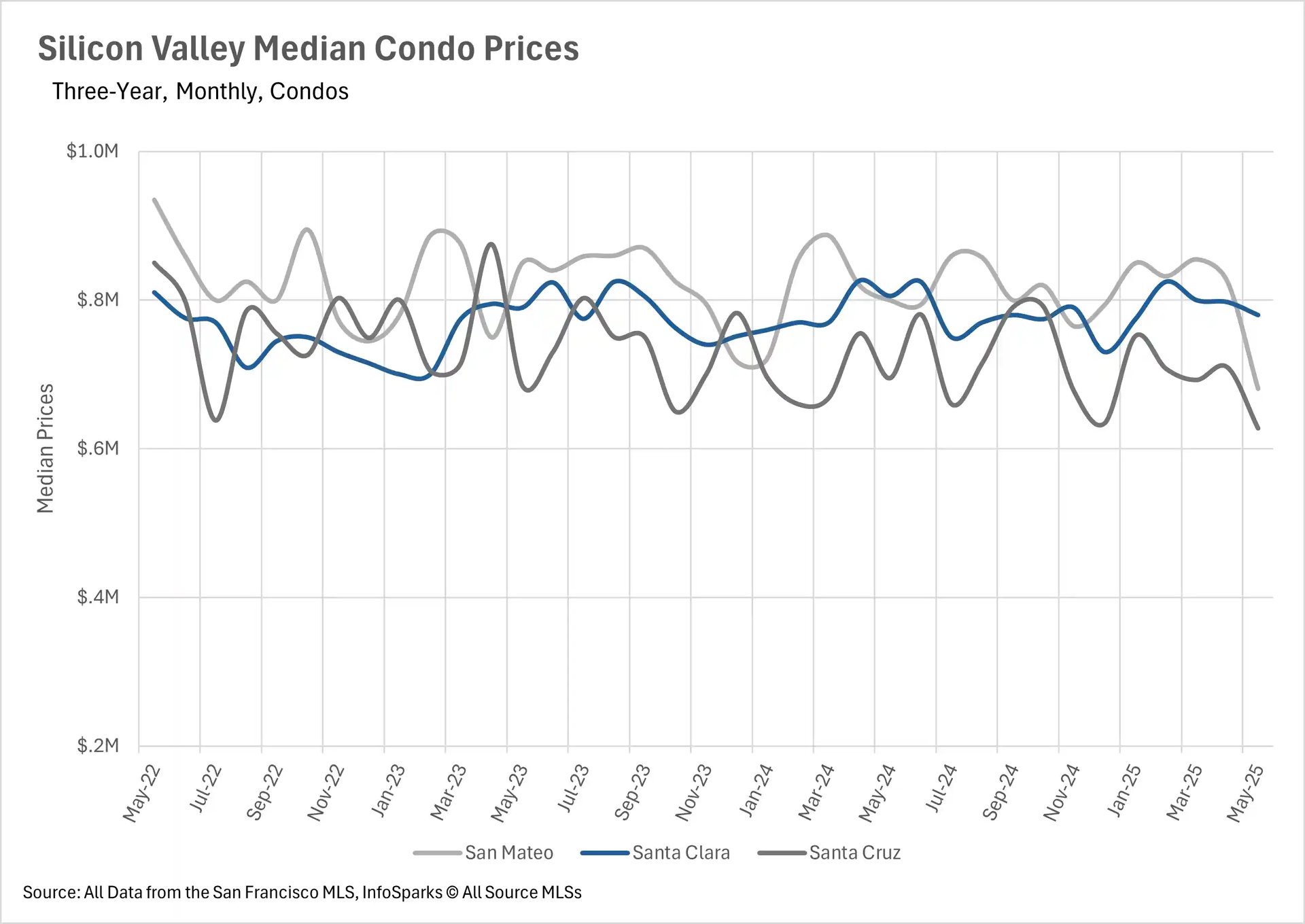

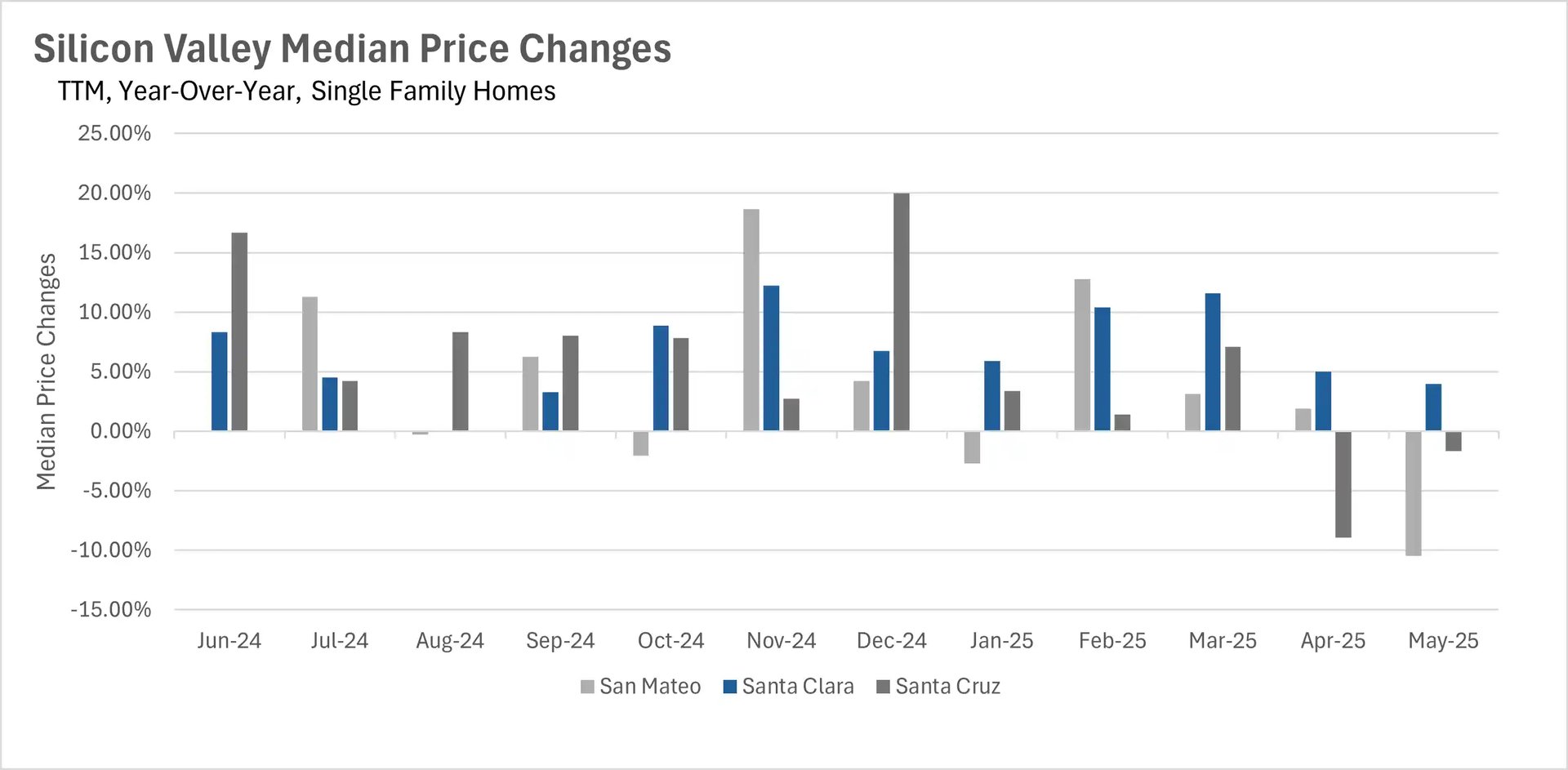

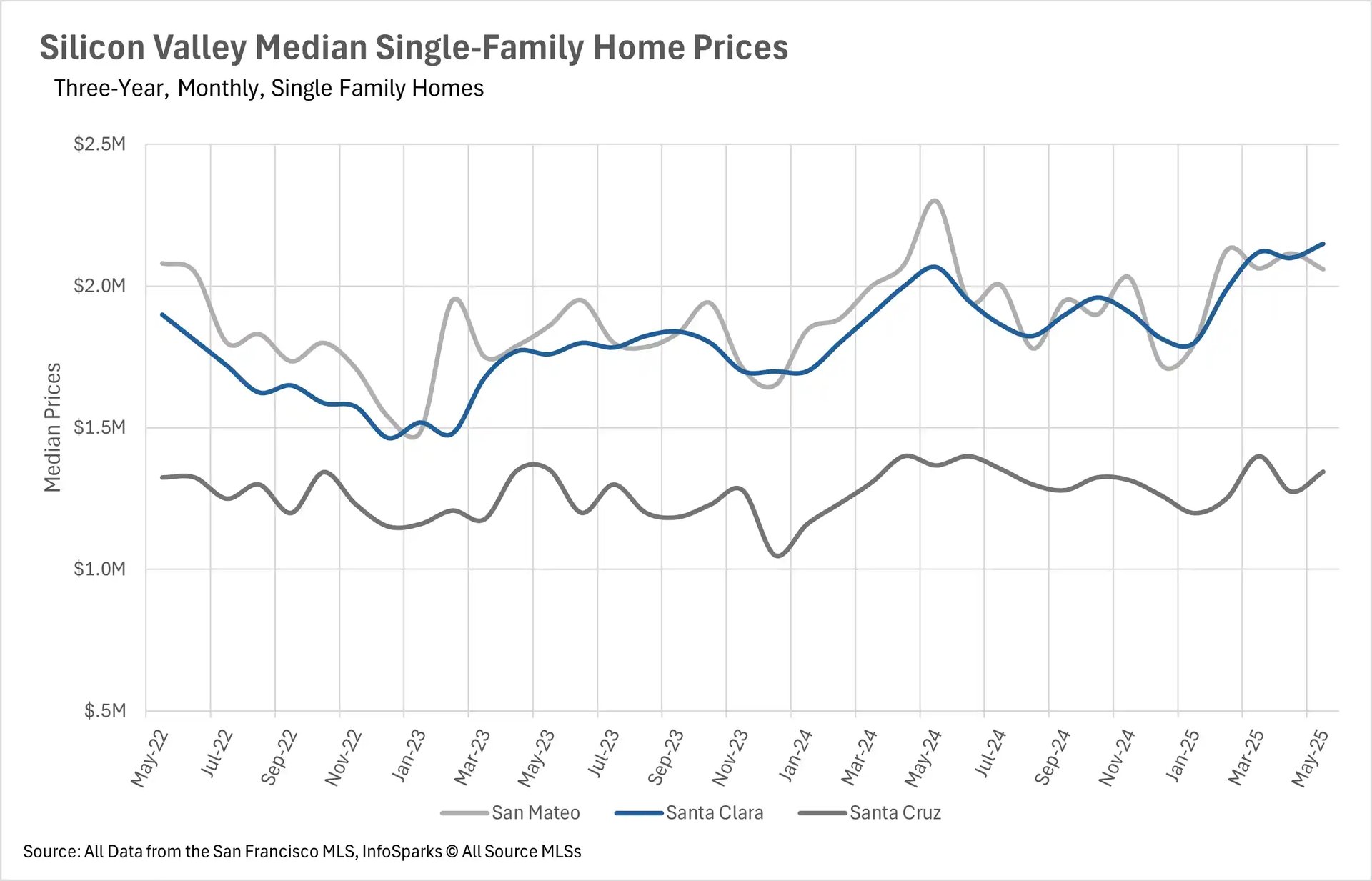

May showcased the Bay Area's increasingly divergent price trends. San Francisco demonstrated remarkable resilience with median single-family home prices surging 7.58% to $1,802,000 and condos jumping 8.26% to $1,298,000, reaching some of the highest levels seen in over two years. This contrasts sharply with Silicon Valley, where the nearly two-year growth streak finally broke. Santa Cruz and San Mateo Counties saw single-family home prices decline by 1.65% and 10.46% respectively, while Santa Clara County managed a modest 3.99% increase.

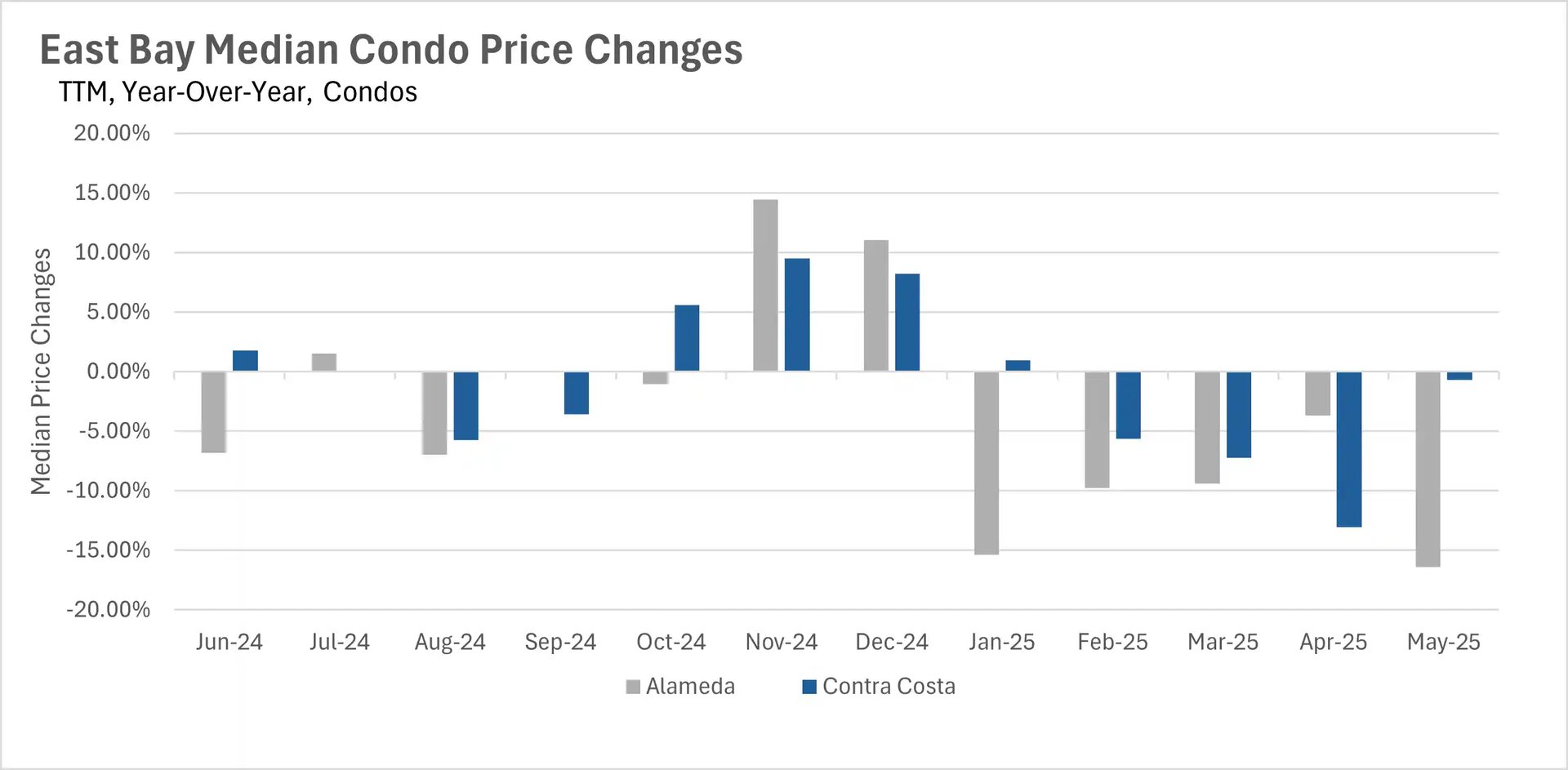

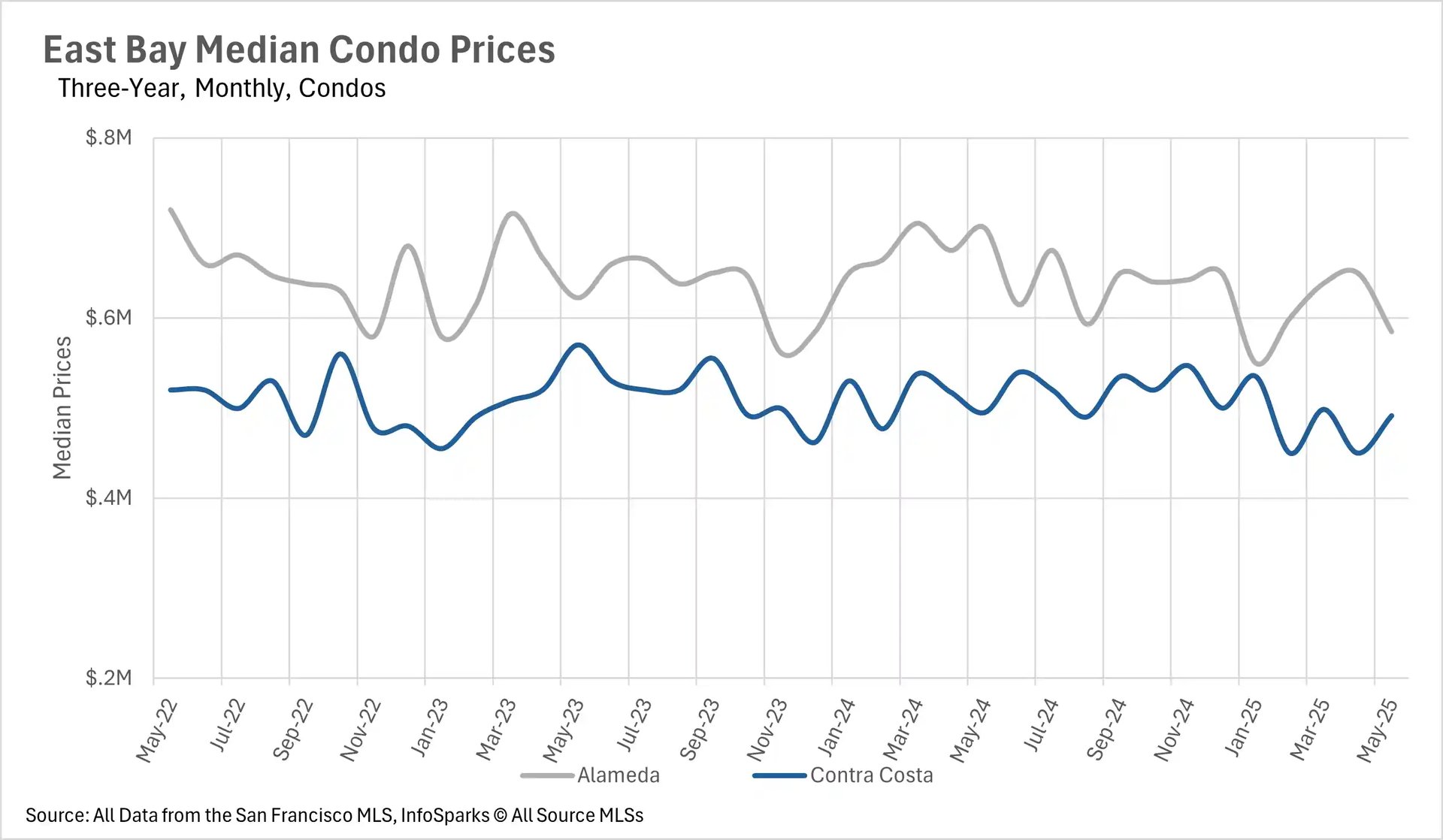

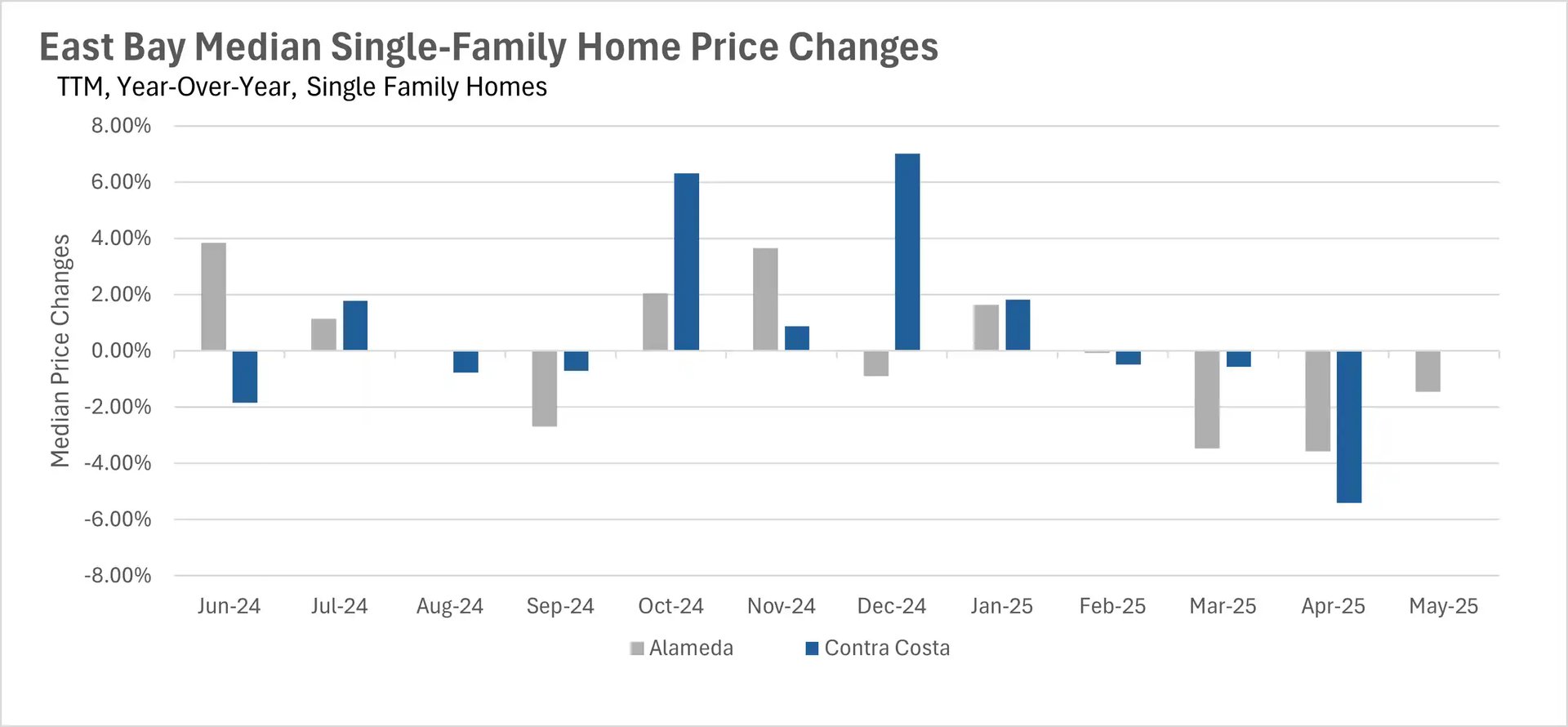

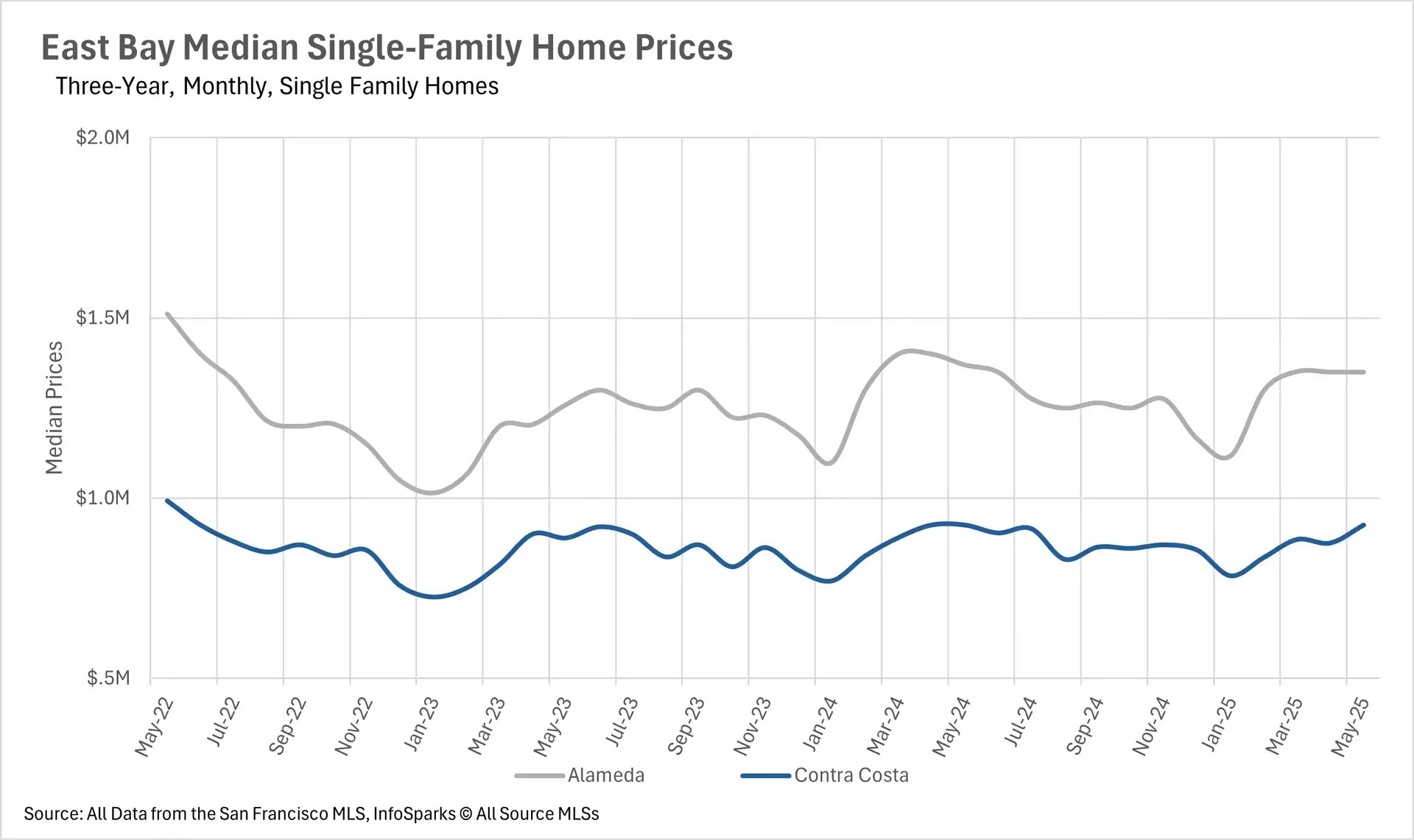

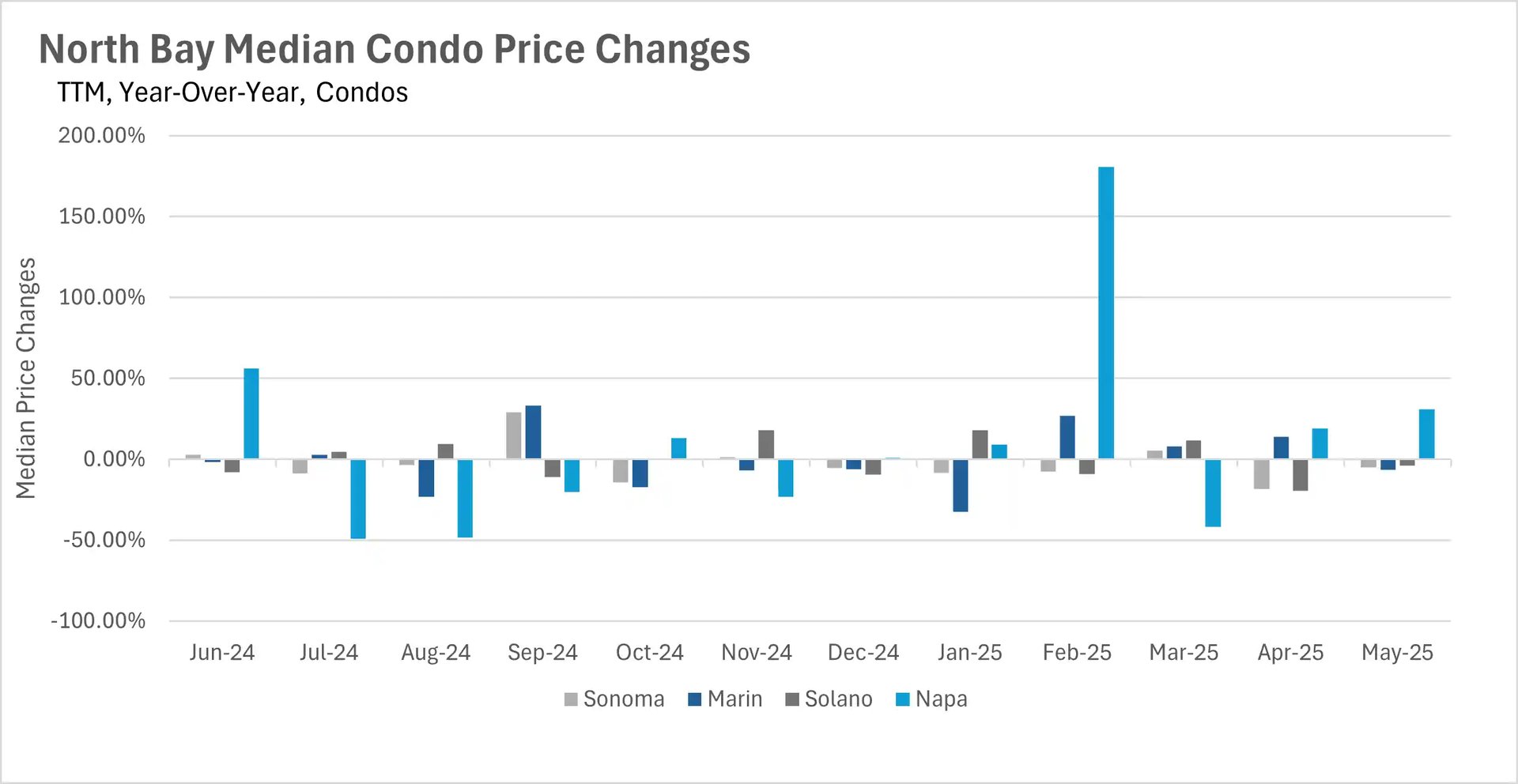

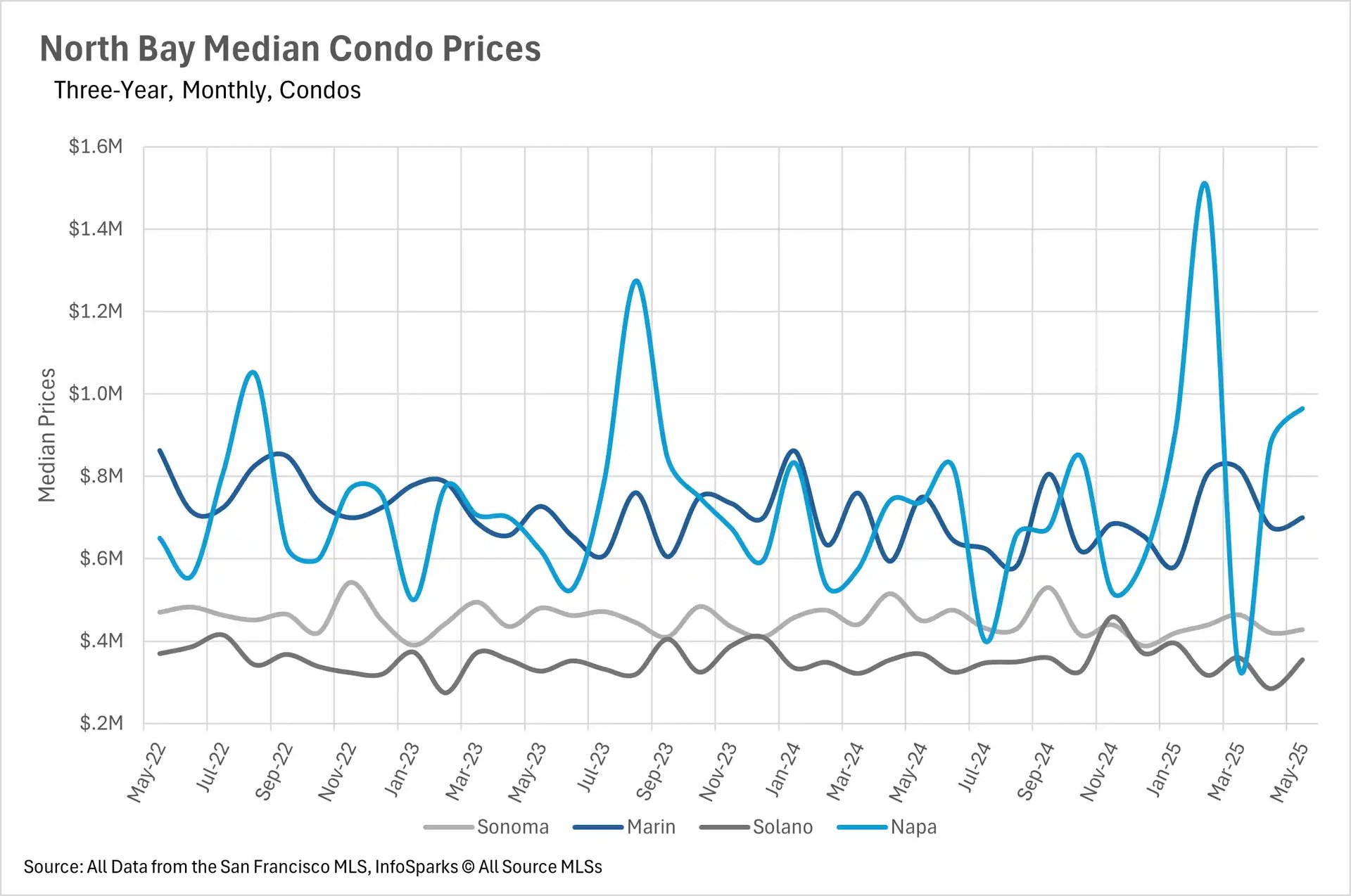

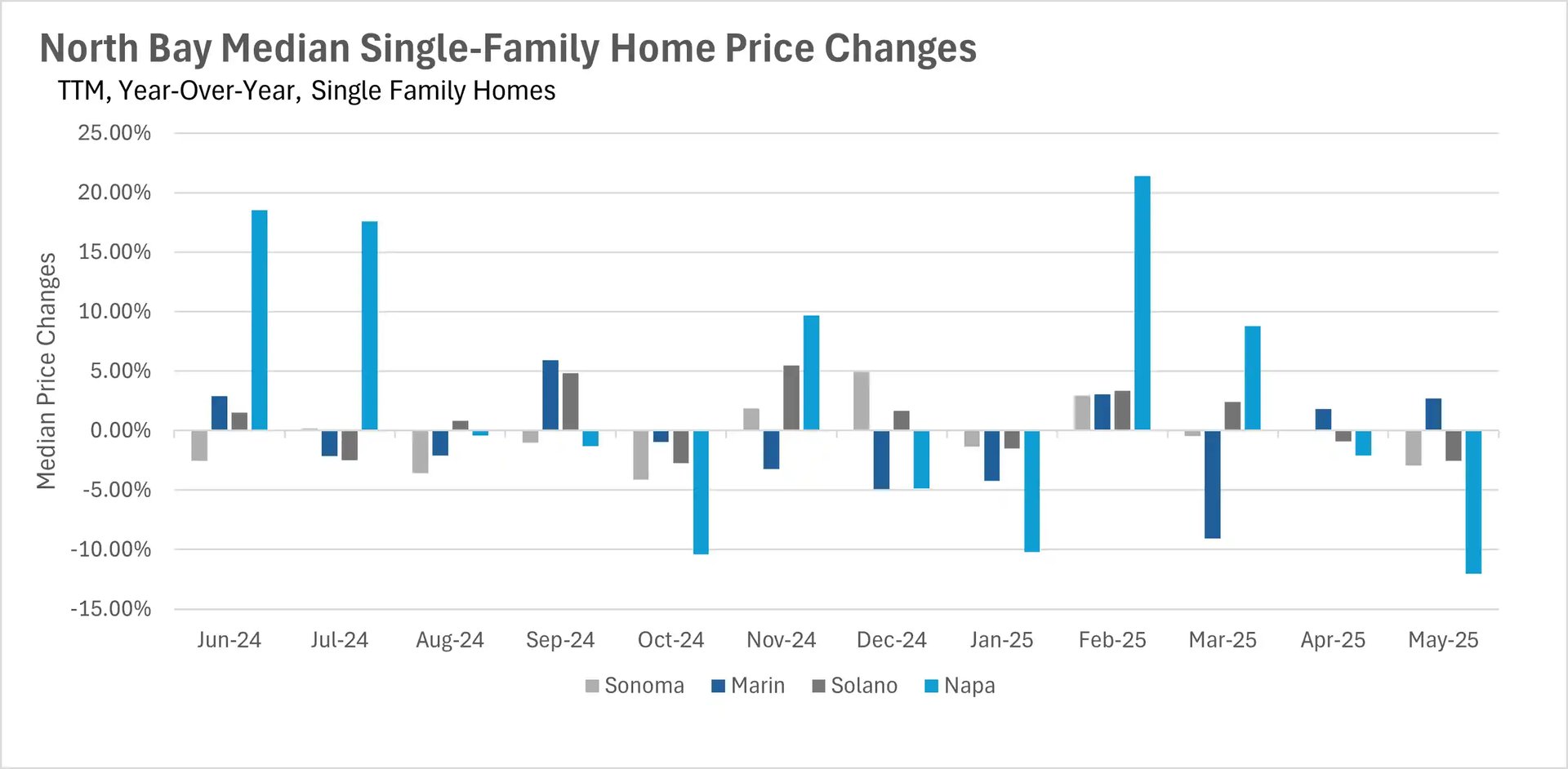

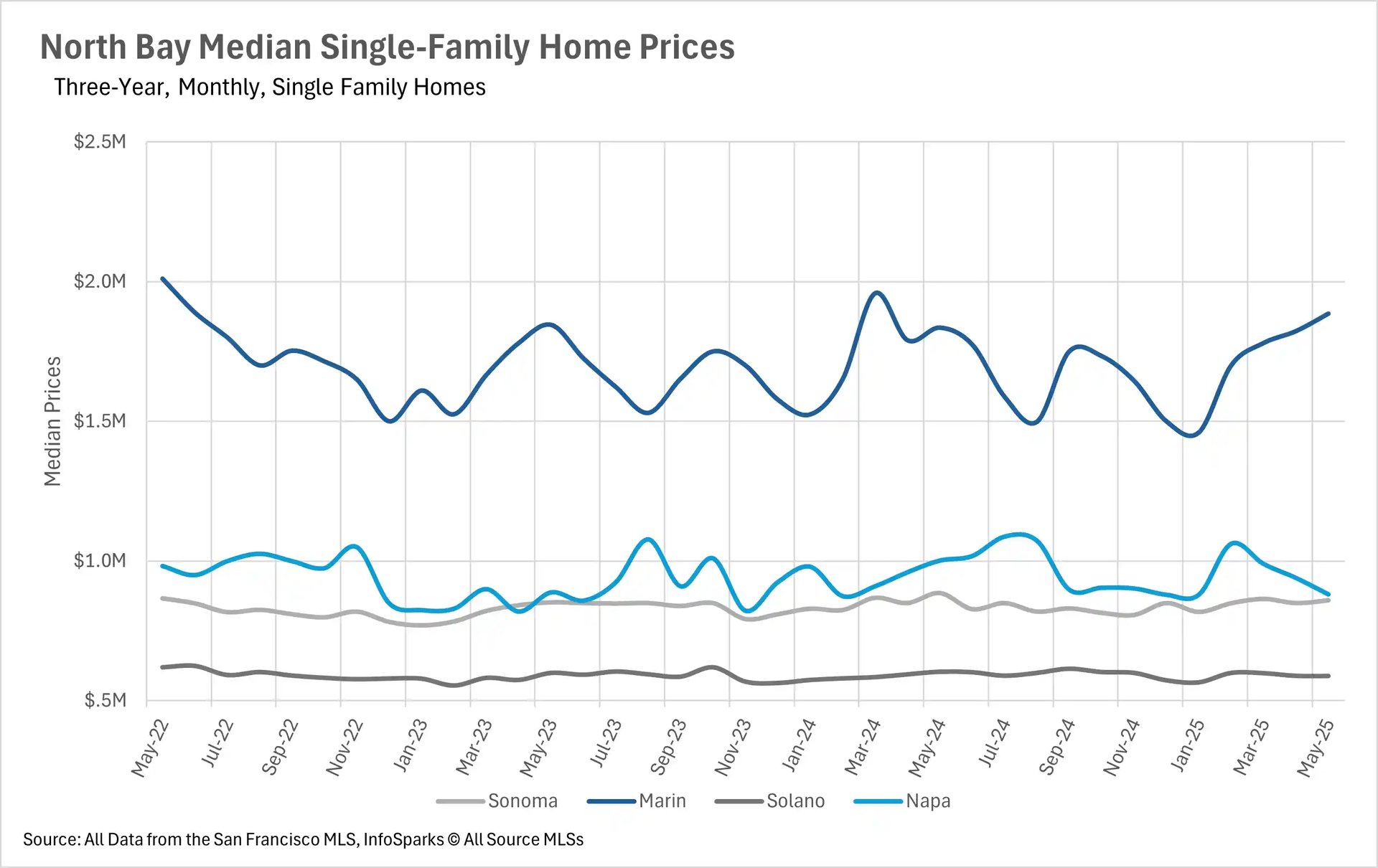

The condo market in Silicon Valley experienced even steeper declines, dropping 14.88% in San Mateo, 3.19% in Santa Clara, and 9.71% in Santa Cruz. Meanwhile, the North Bay showed widespread price weakness, with Napa County experiencing a dramatic 12.03% decline, while Solano and Sonoma Counties saw more modest decreases of 2.93% and 2.52%. Only Marin County bucked the trend with a 2.72% increase. The East Bay proved most resilient with minimal price movement, just 0.01% down in Contra Costa County and 1.46% down in Alameda County for single-family homes, though condos faced significant pressure with Alameda down 16.43%.

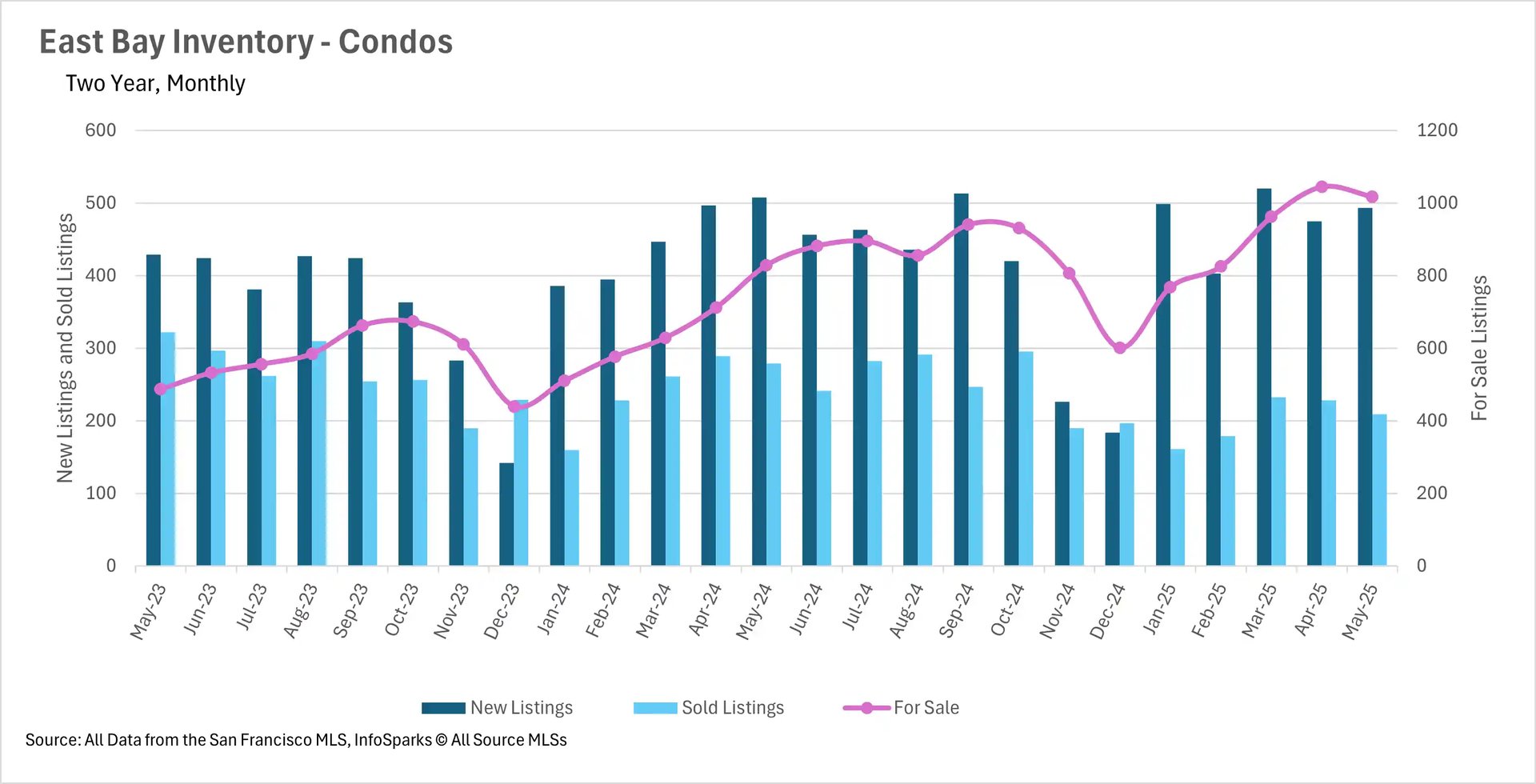

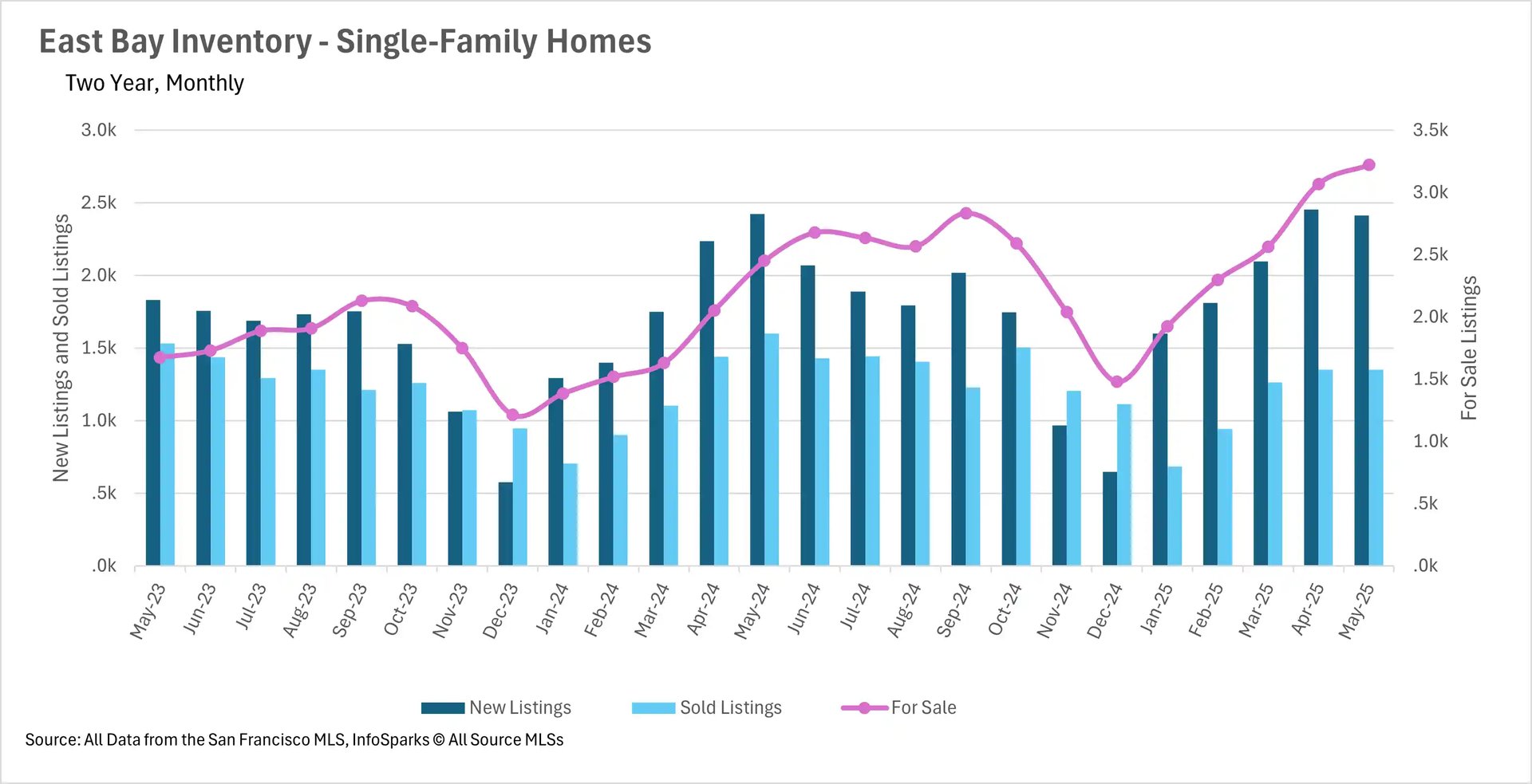

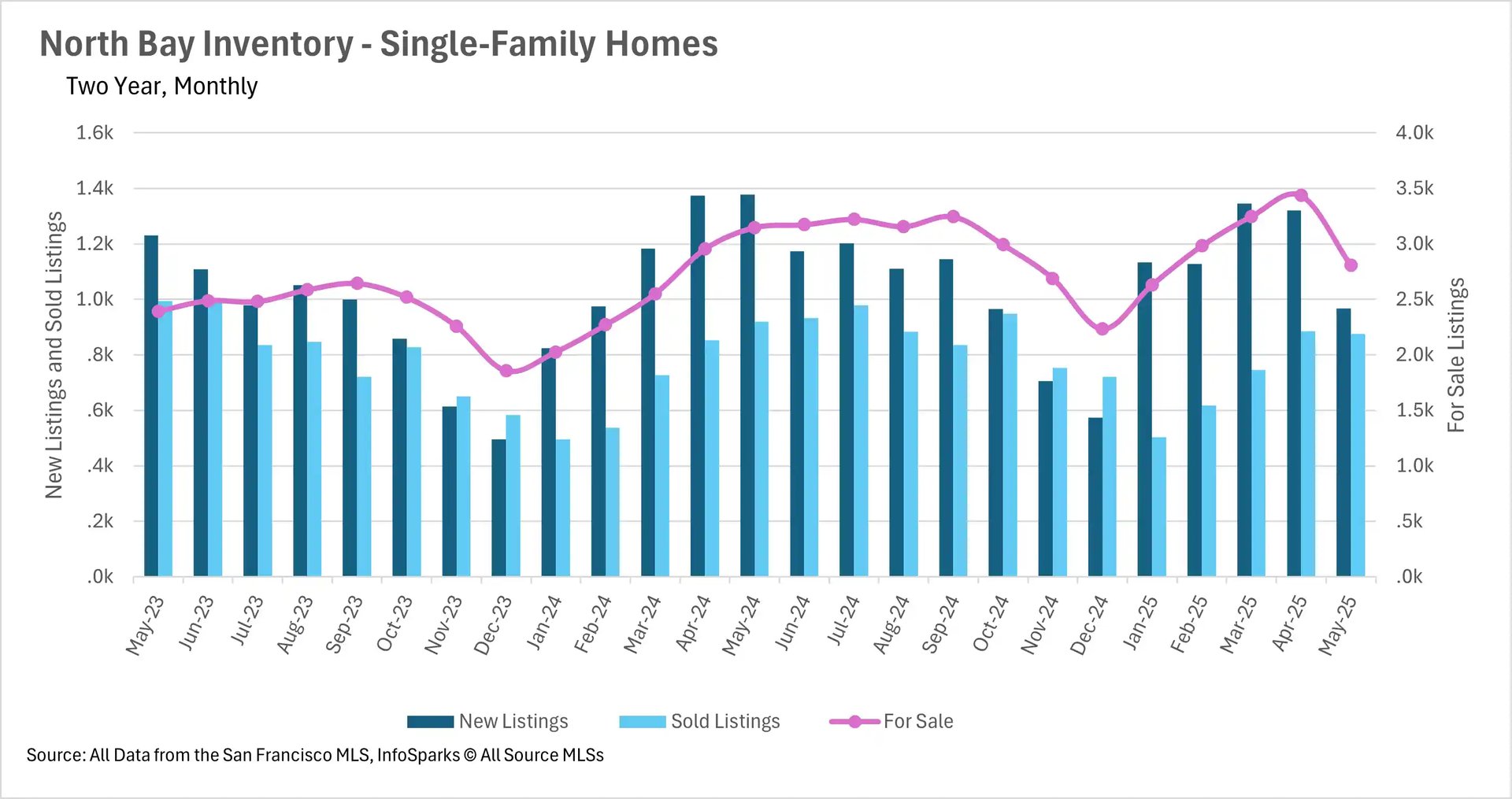

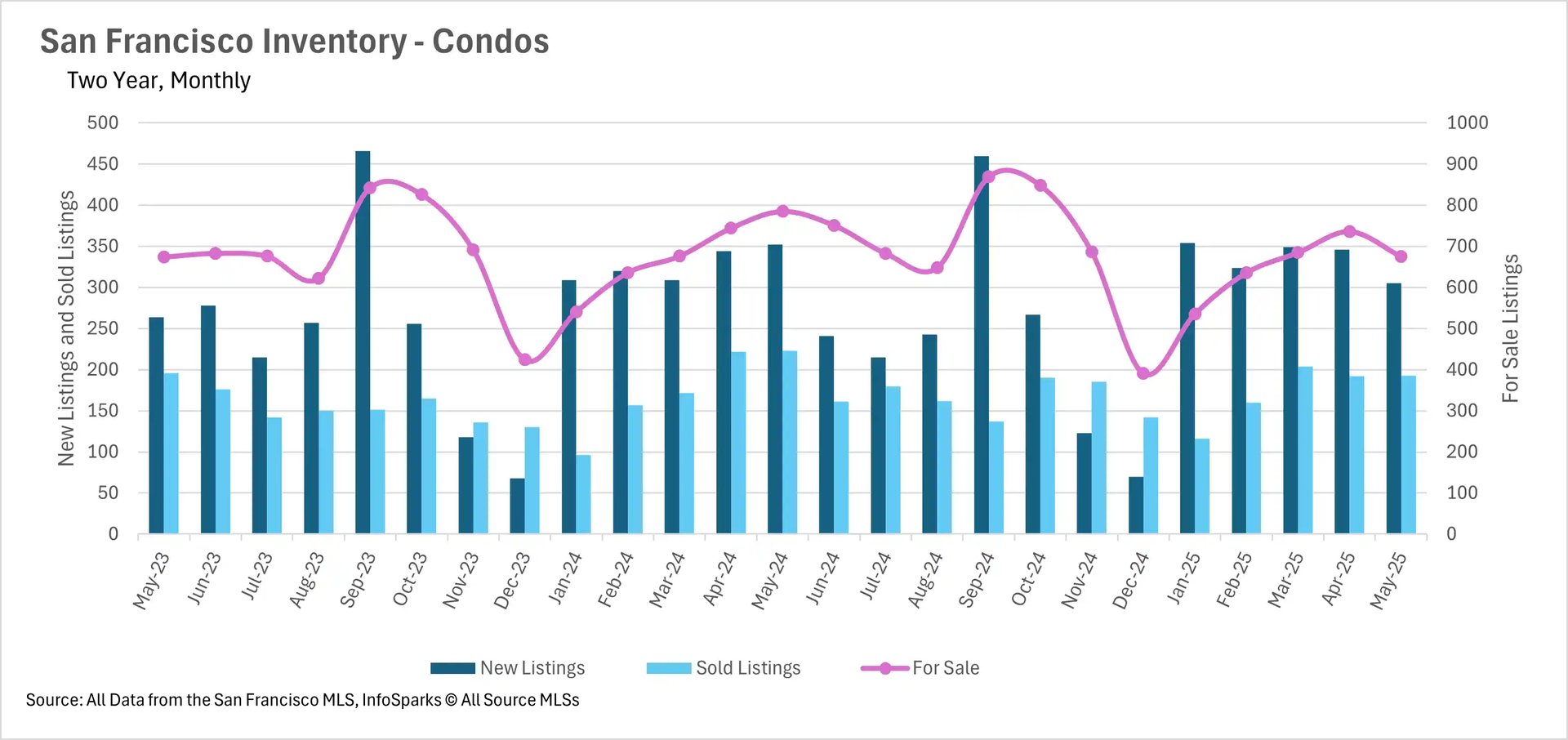

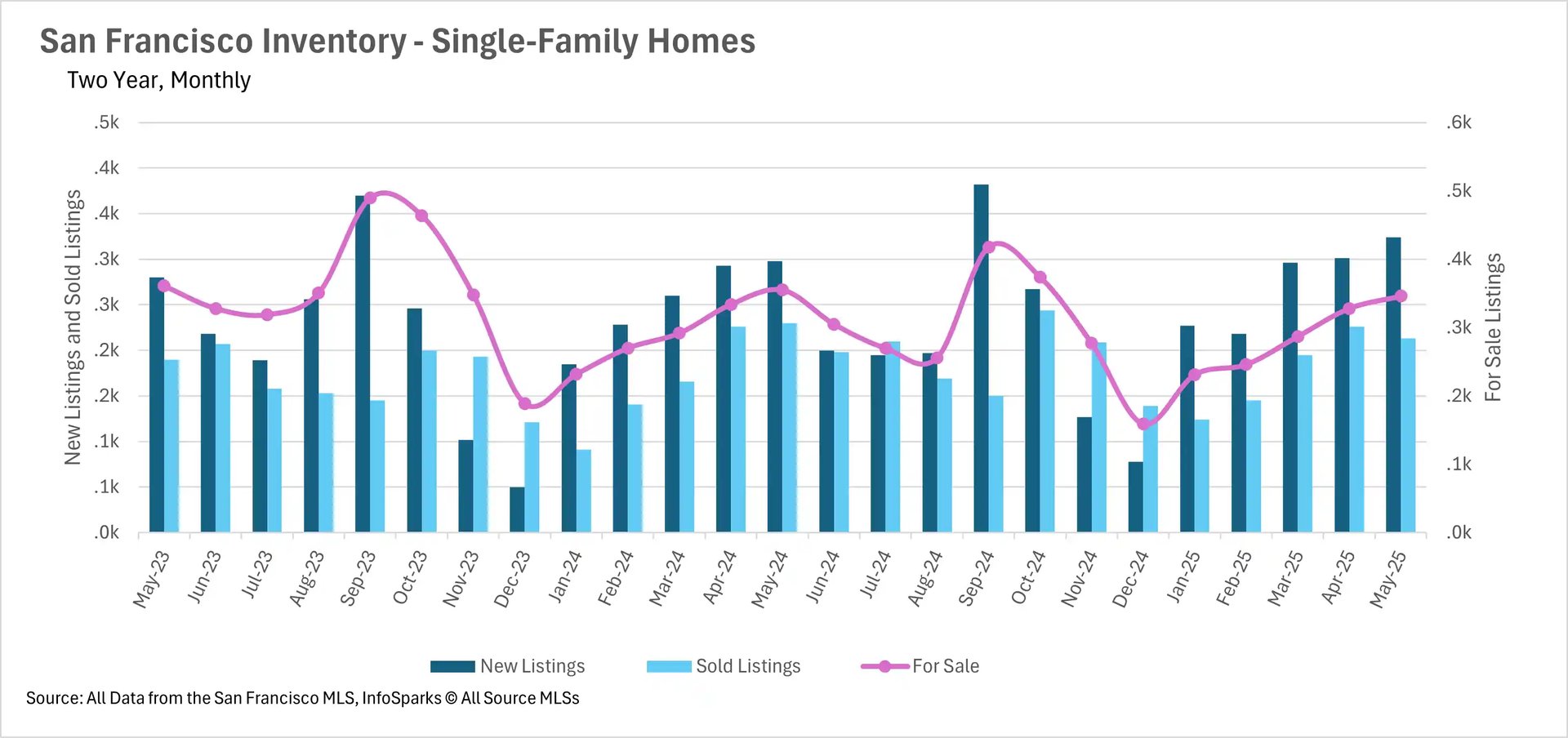

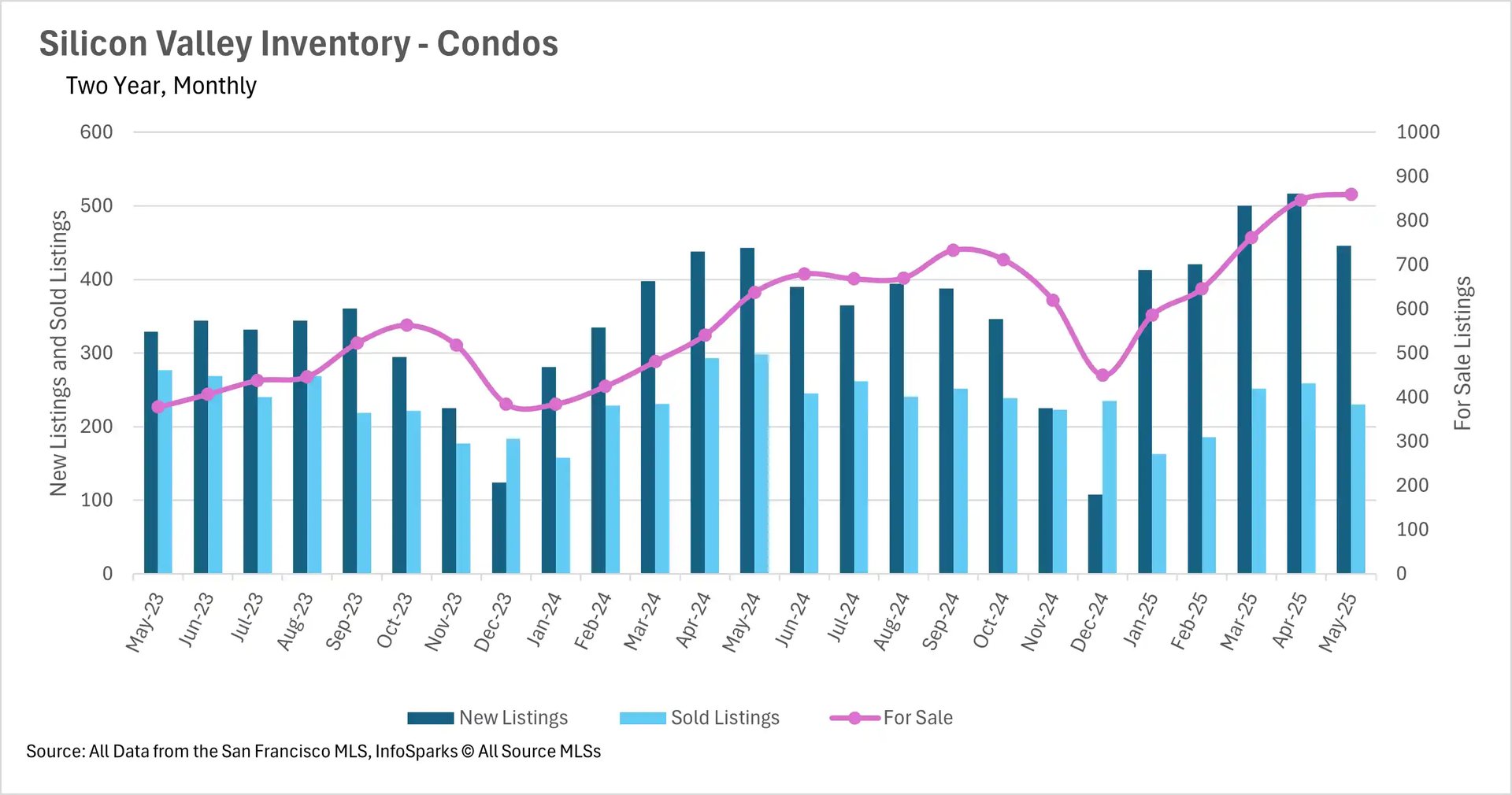

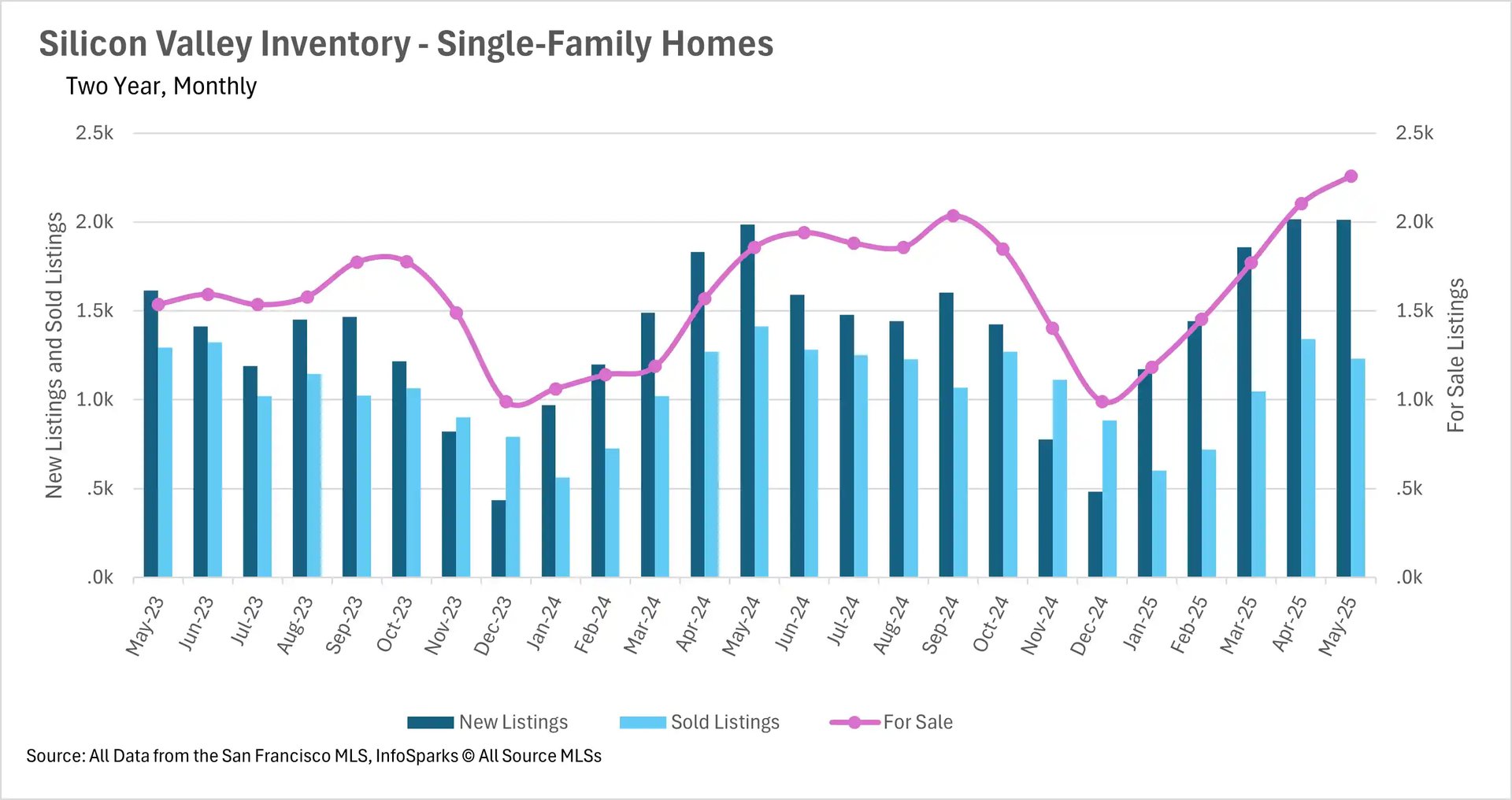

Inventory trends create a tale of two markets

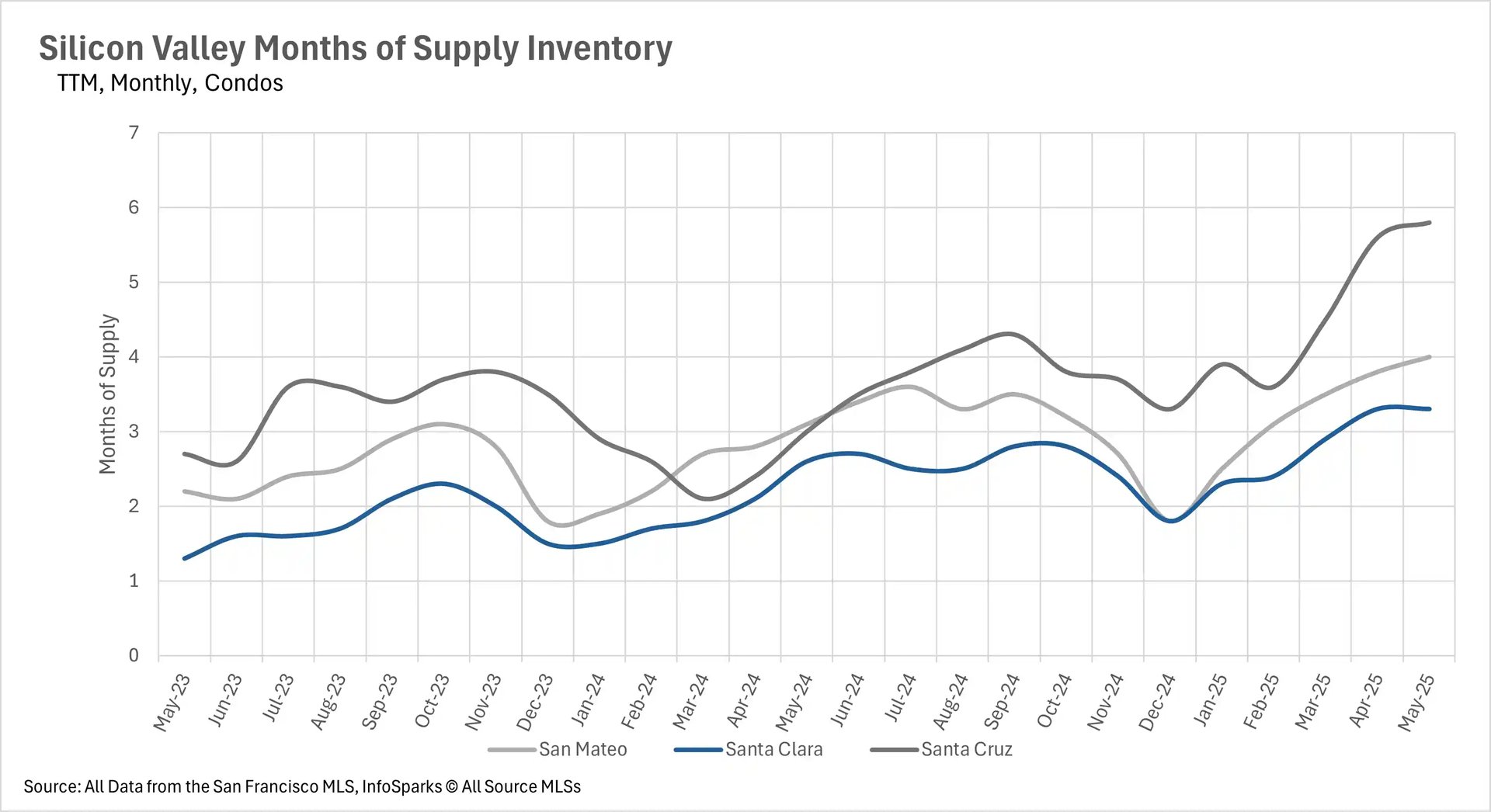

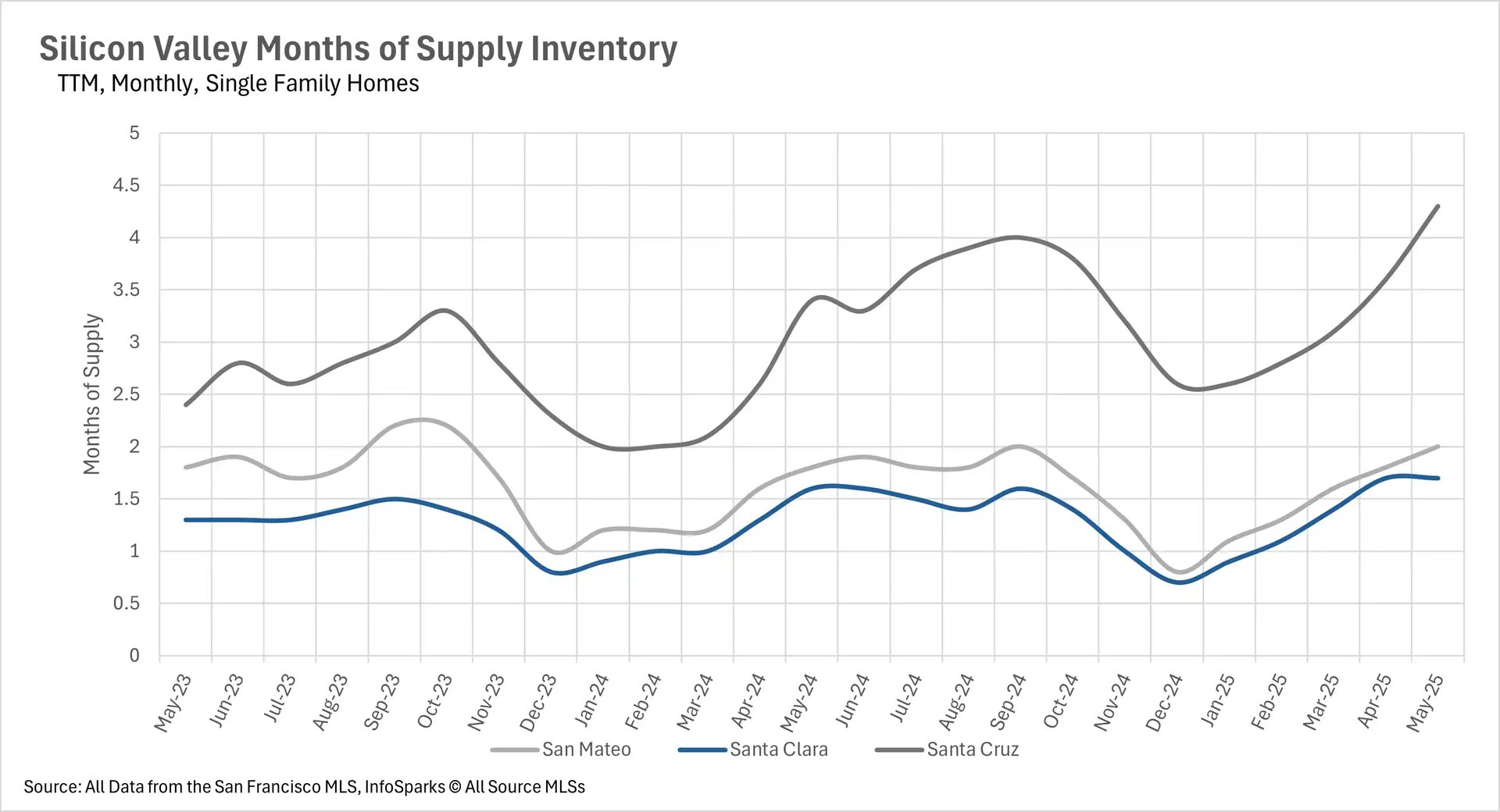

May revealed stark inventory contrasts across the Bay Area. The East Bay and Silicon Valley experienced massive inventory buildups, with East Bay single-family home inventories reaching new two-year highs, increasing 31.42% year-over-year, while condo inventories grew 22.80%. Silicon Valley similarly set new records with single-family inventories jumping 21.65% and condo inventories surging 34.80%. Both regions attributed this to fewer sales rather than more listings, East Bay saw 15.57% fewer single-family home sales and 25.09% fewer condo sales, while Silicon Valley experienced 13.01% fewer single-family sales and 22.82% fewer condo sales.

In dramatic contrast, San Francisco continued its multi-year inventory decline with single-family homes down 2.54% and condos falling 14.01% year-over-year. The North Bay also saw sharp inventory declines, with single-family home listings dropping 10.74% and new listings decreasing roughly 30% across both single-family homes and condos. This created a bifurcated Bay Area market where inventory abundance in some regions coincided with severe shortages in others.

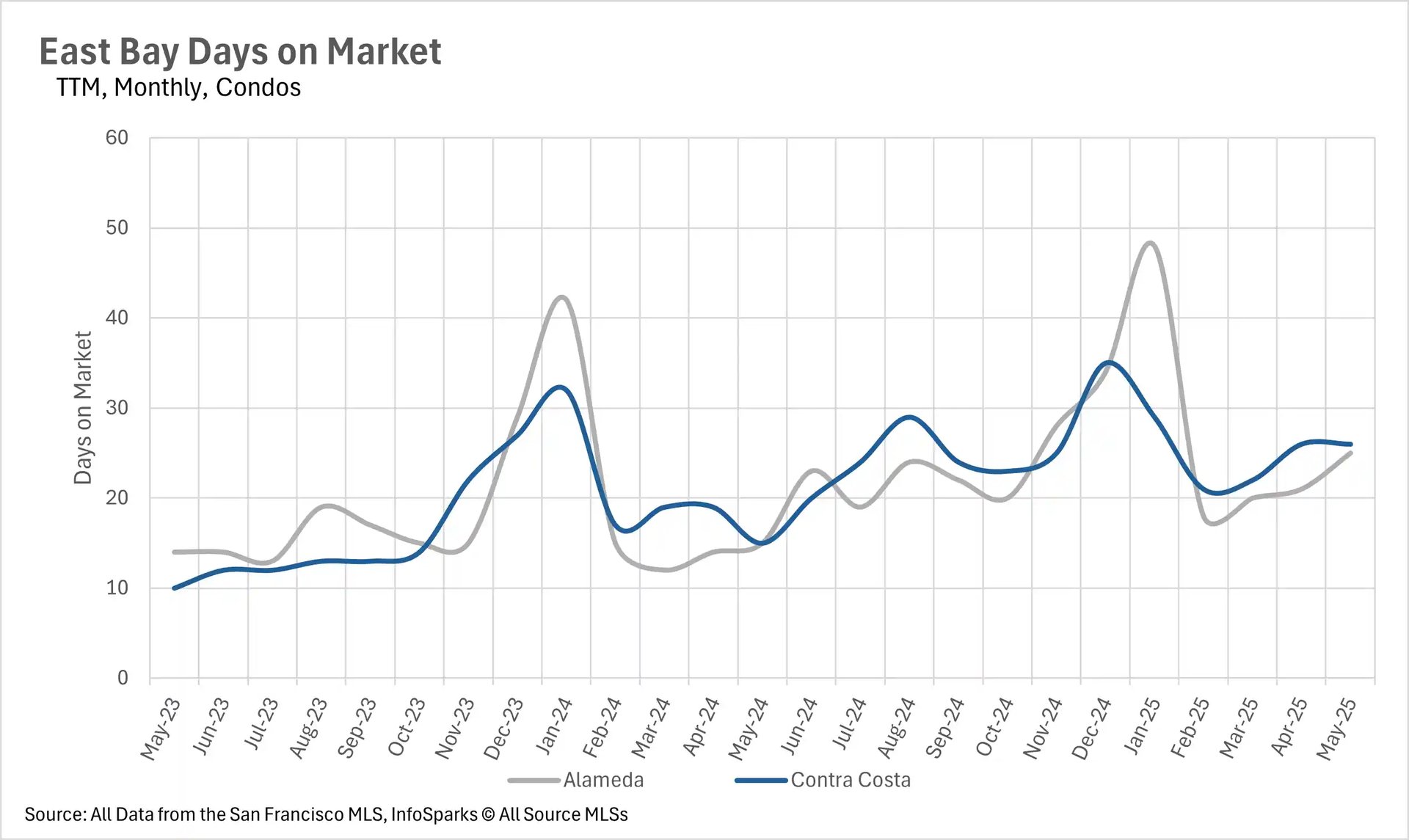

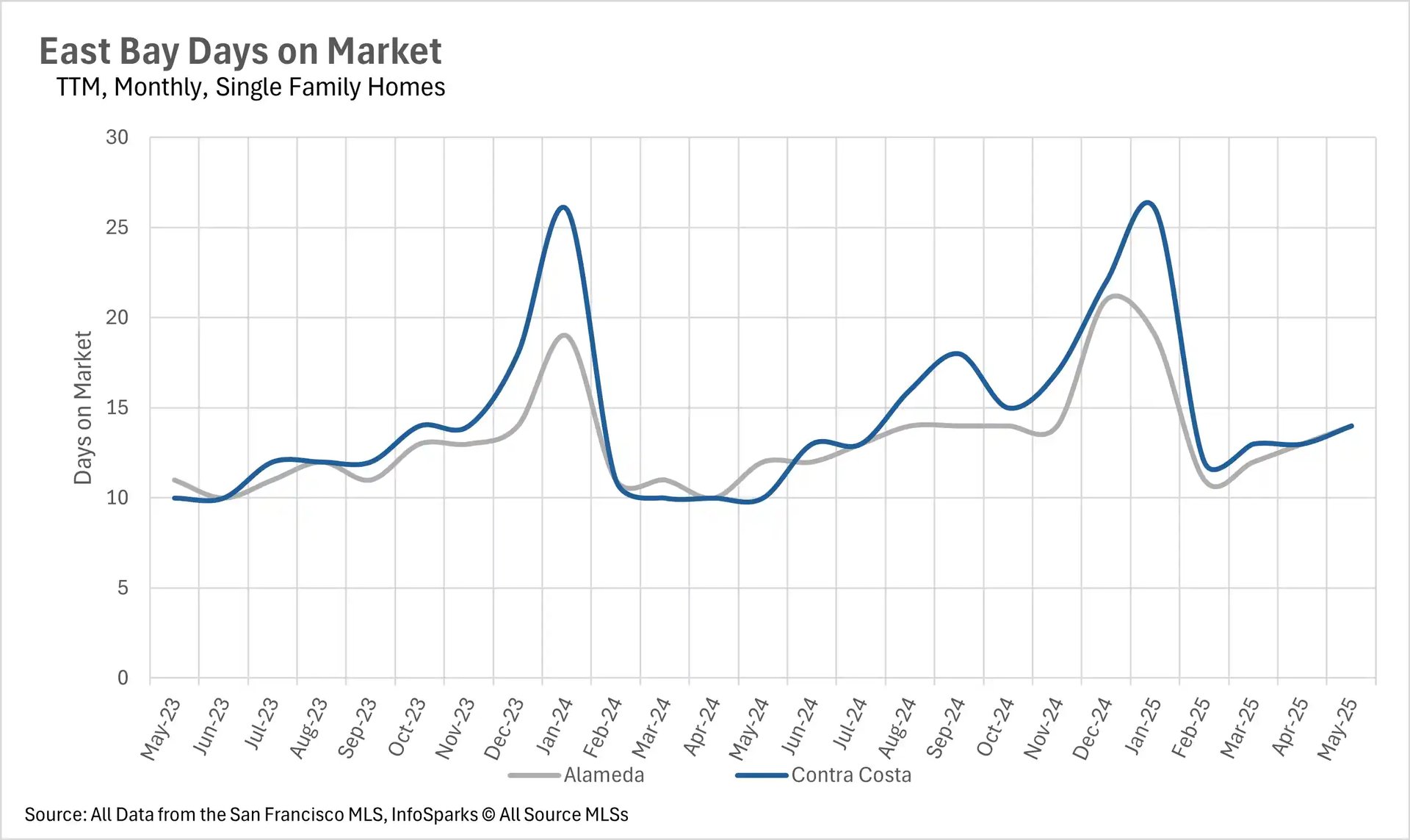

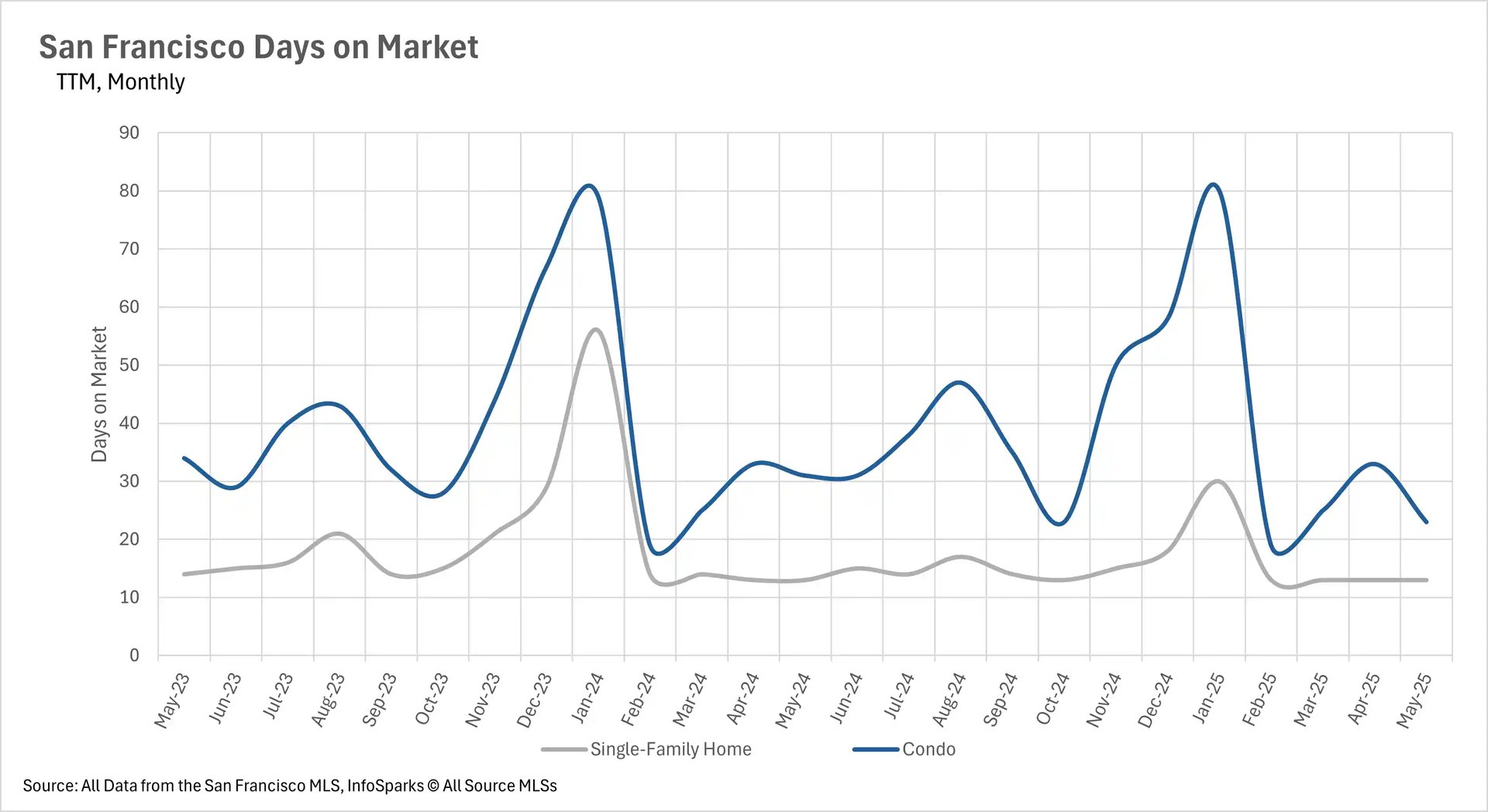

Days on market reveal regional buyer behavior patterns

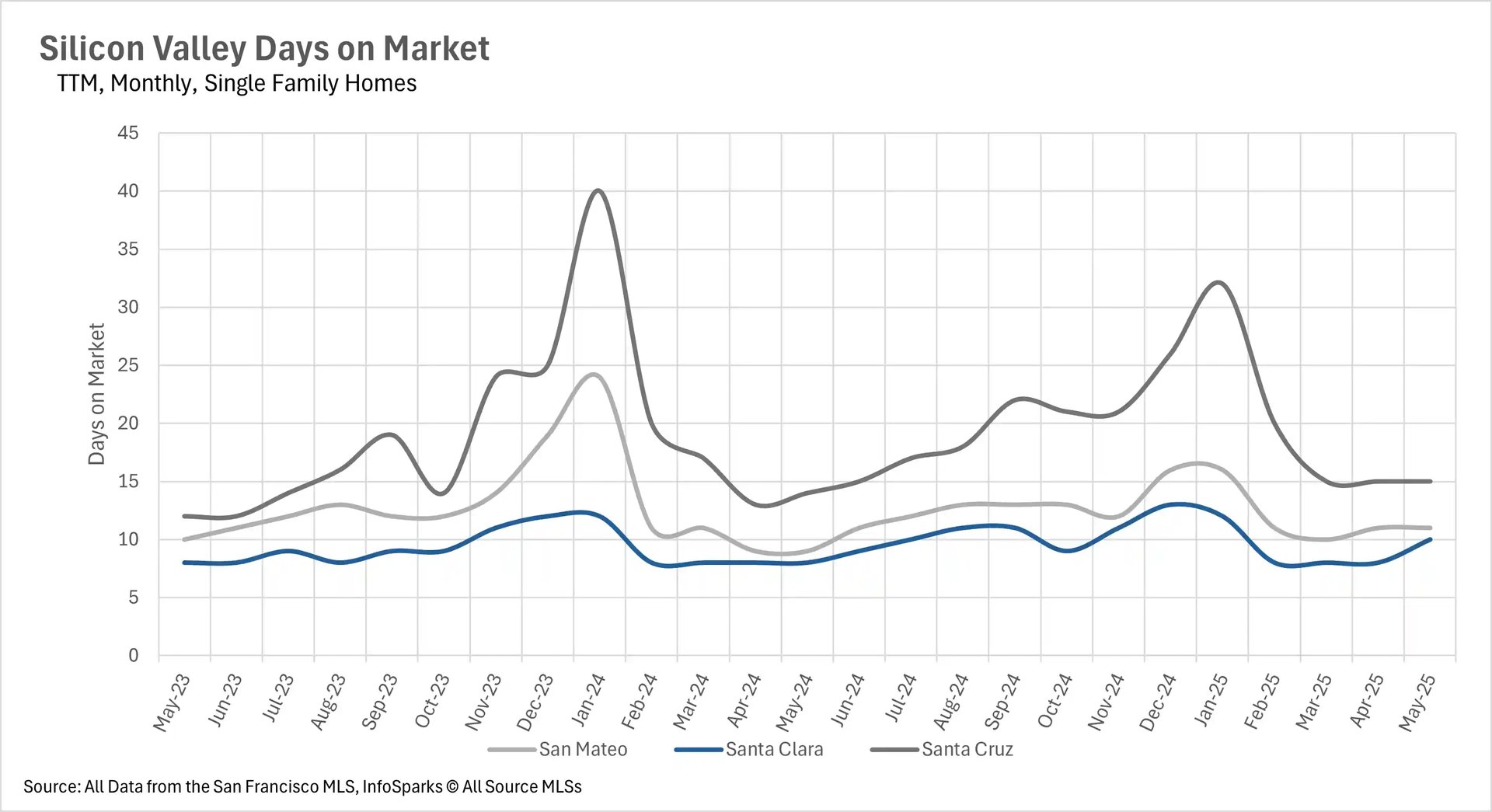

The time properties spend on market varies dramatically across the Bay Area, revealing distinct buyer behavior patterns. San Francisco maintains the fastest-moving market, with single-family homes selling in just 13 days (unchanged from last year) and condos moving in 23 days (a significant improvement from 31 days last May). The East Bay also shows quick movement despite inventory increases, with single-family homes averaging just 14 days on market, though this represents a 40% increase from last year.

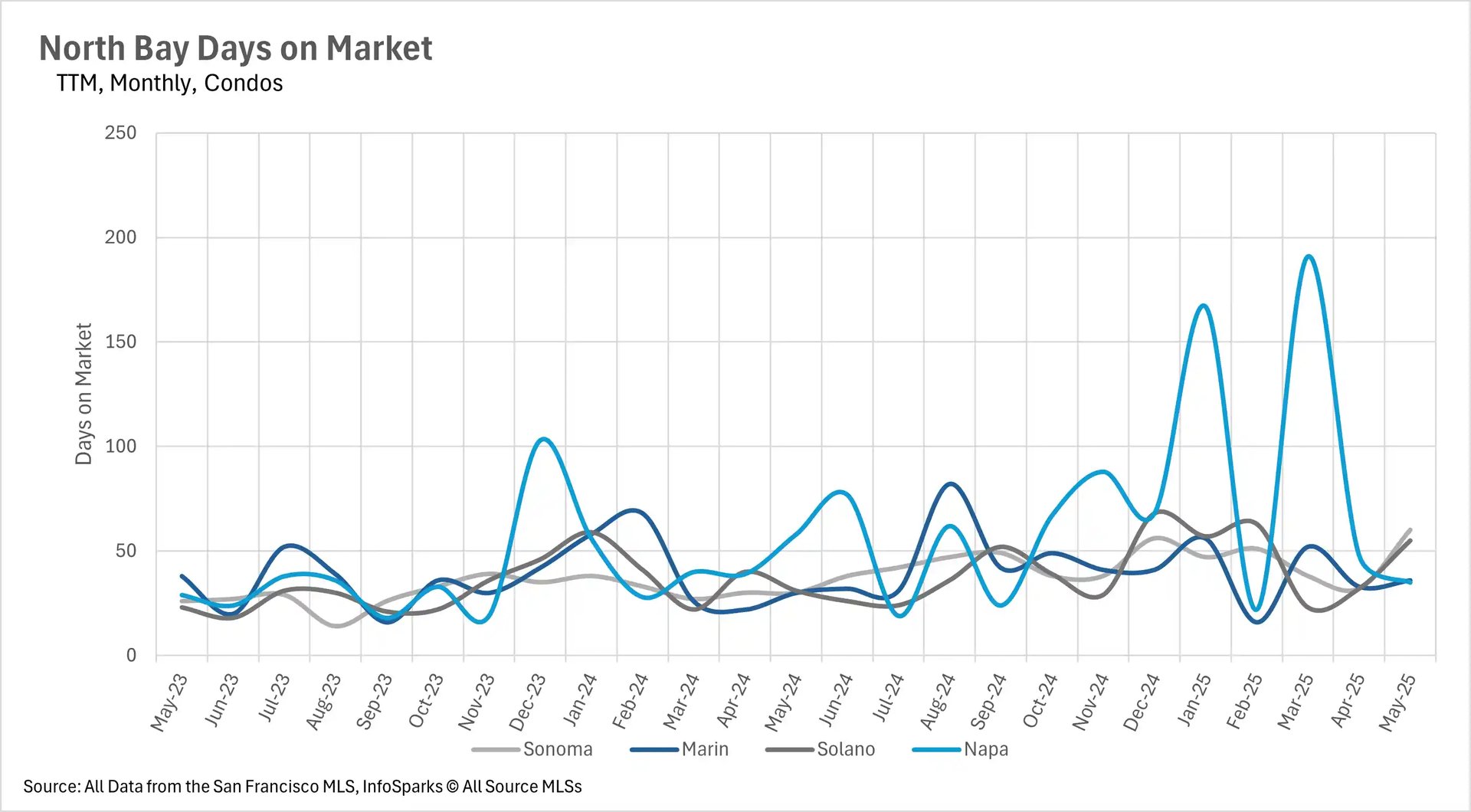

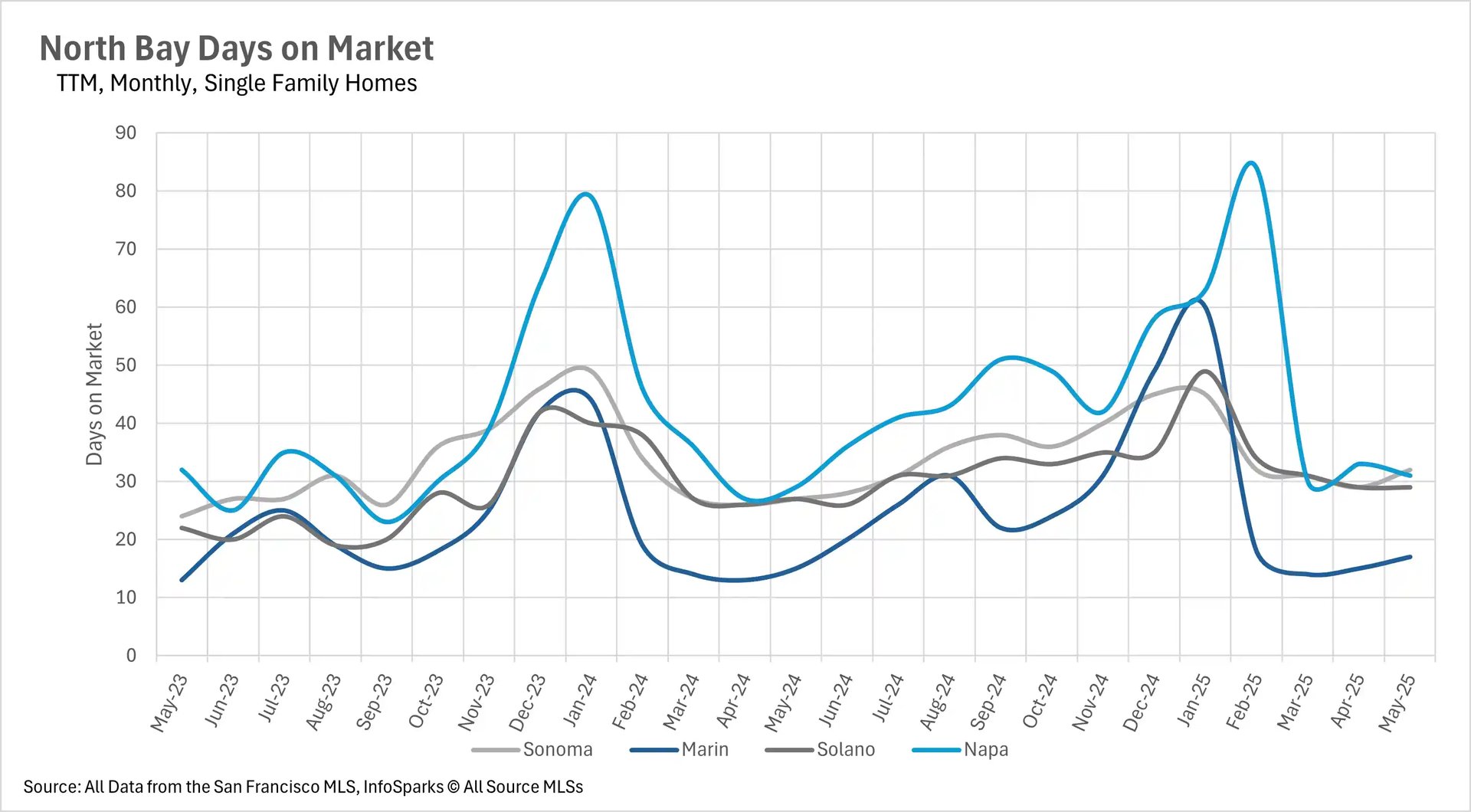

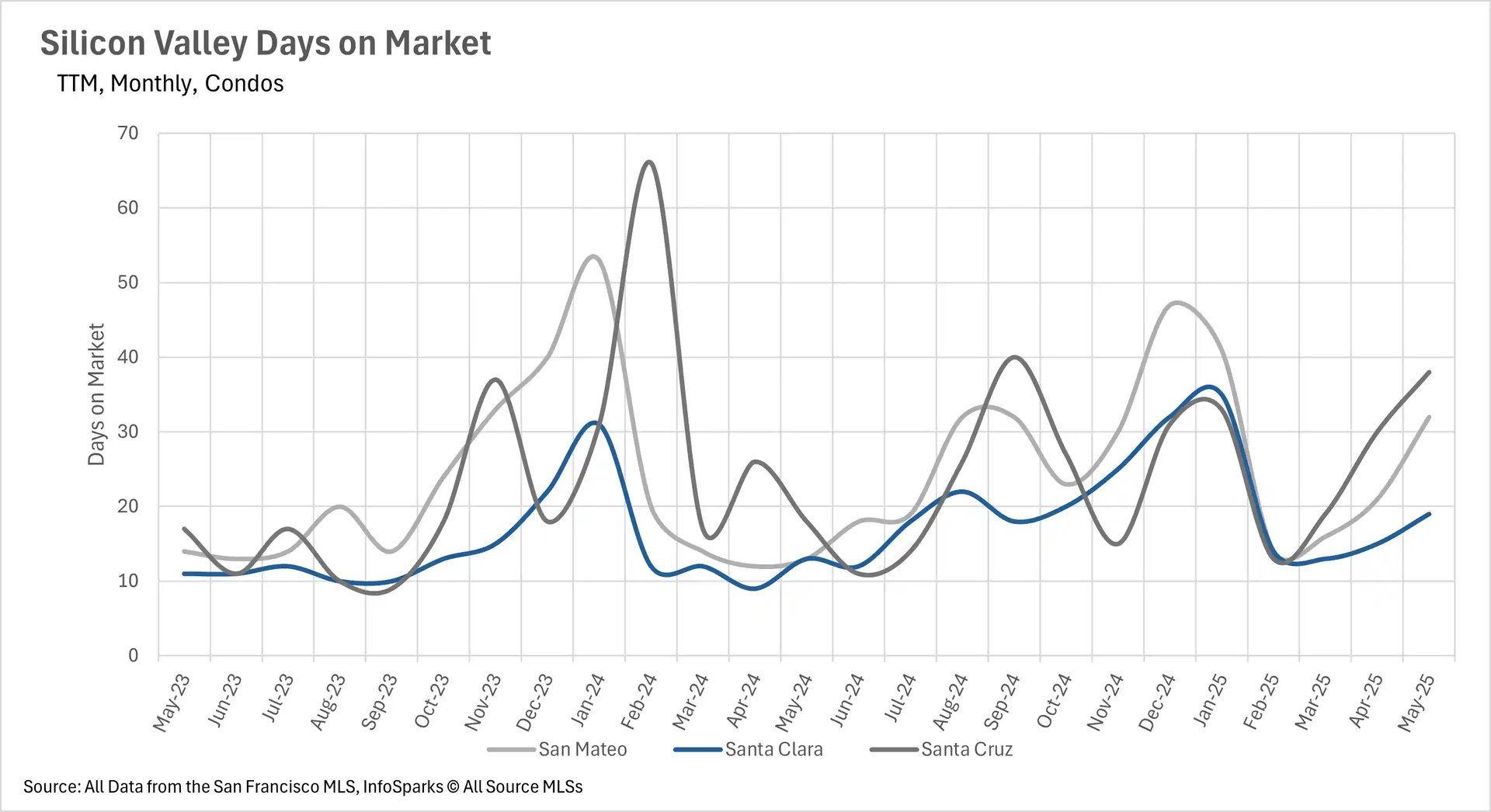

Silicon Valley single-family homes remain within their long-term averages for market time, but condos are experiencing significant delays, spending 46.15% more days on market in Santa Clara, 111.11% more in Santa Cruz, and 146.15% more in San Mateo Counties compared to last year. The North Bay shows the most consistent pattern of longer market times, with single-family homes spending 5 more days on market in Sonoma County and 2 more days in Marin, Solano, and Napa Counties year-over-year. These patterns suggest that while single-family homes continue to move relatively quickly throughout most of the Bay Area, the condo market is experiencing a fundamental shift toward longer selling periods, particularly in Silicon Valley.

Market dynamics increasingly favor property type over location

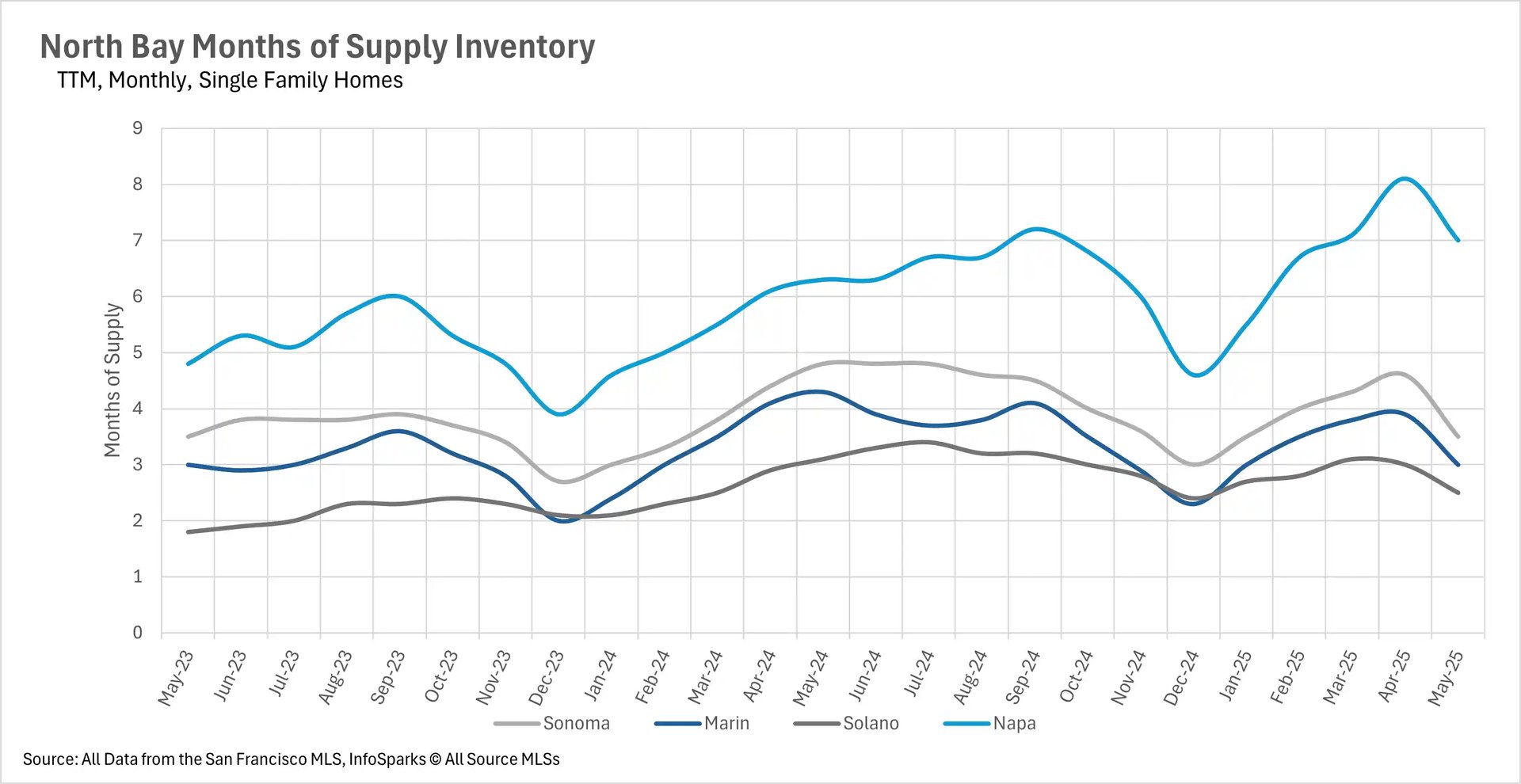

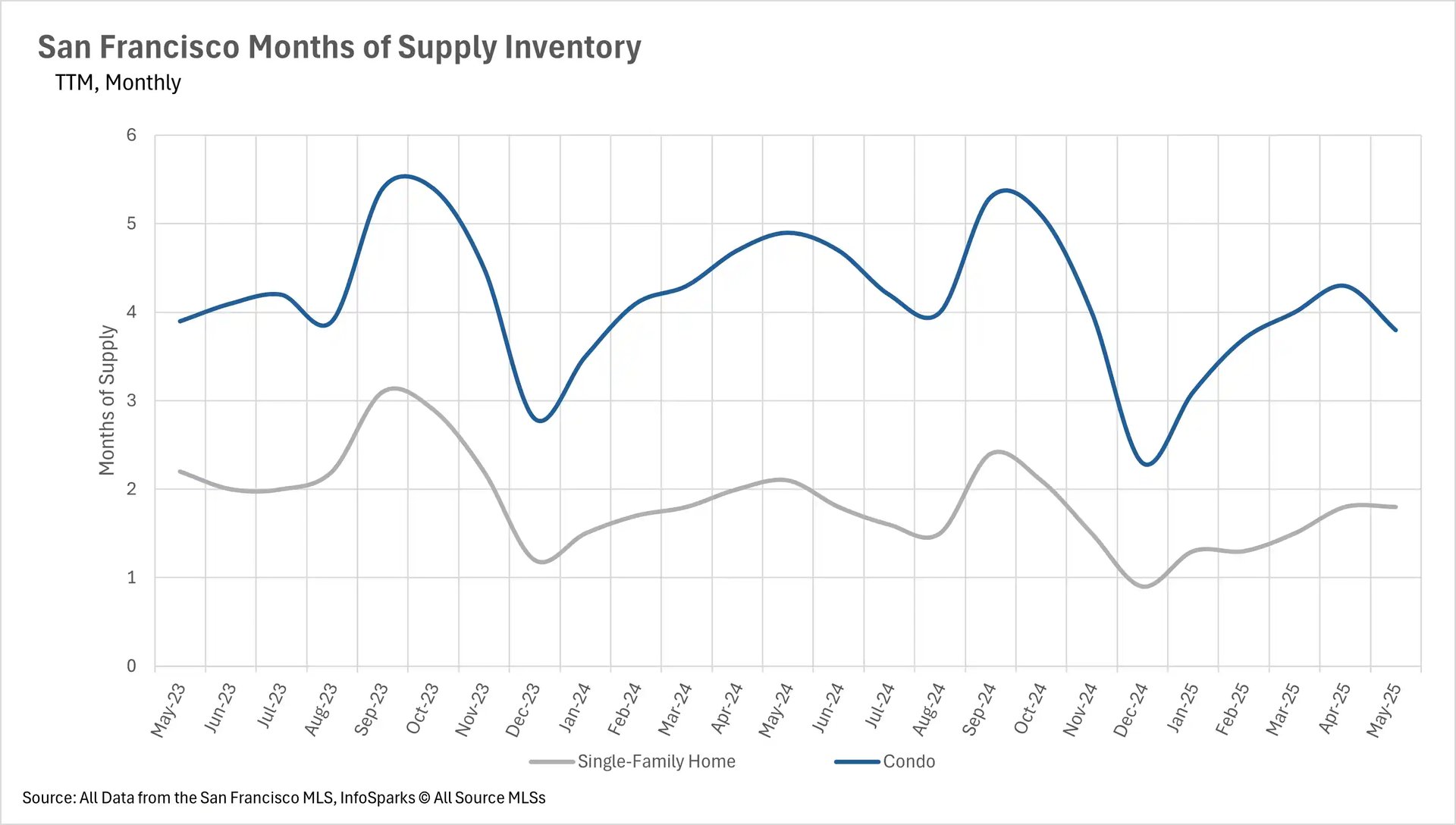

The months of supply inventory (MSI) metric reveals a consistent pattern across the Bay Area that transcends regional boundaries: single-family homes generally remain in seller's market territory while condos increasingly favor buyers. San Francisco exemplifies this split with single-family homes at just 1.8 months of supply (down 14.29% year-over-year) while condos sit at 3.8 months (down 22.45% but still favoring buyers). Silicon Valley has largely become a buyer's market, with all three counties showing buyer-favorable condo markets (4 months in San Mateo, 3.3 in Santa Clara, and 5.8 in Santa Cruz). However, Santa Cruz County's single-family market has shifted to favor buyers with 4.3 months of supply, while San Mateo (2 months) and Santa Clara (1.7 months) remain seller's markets.

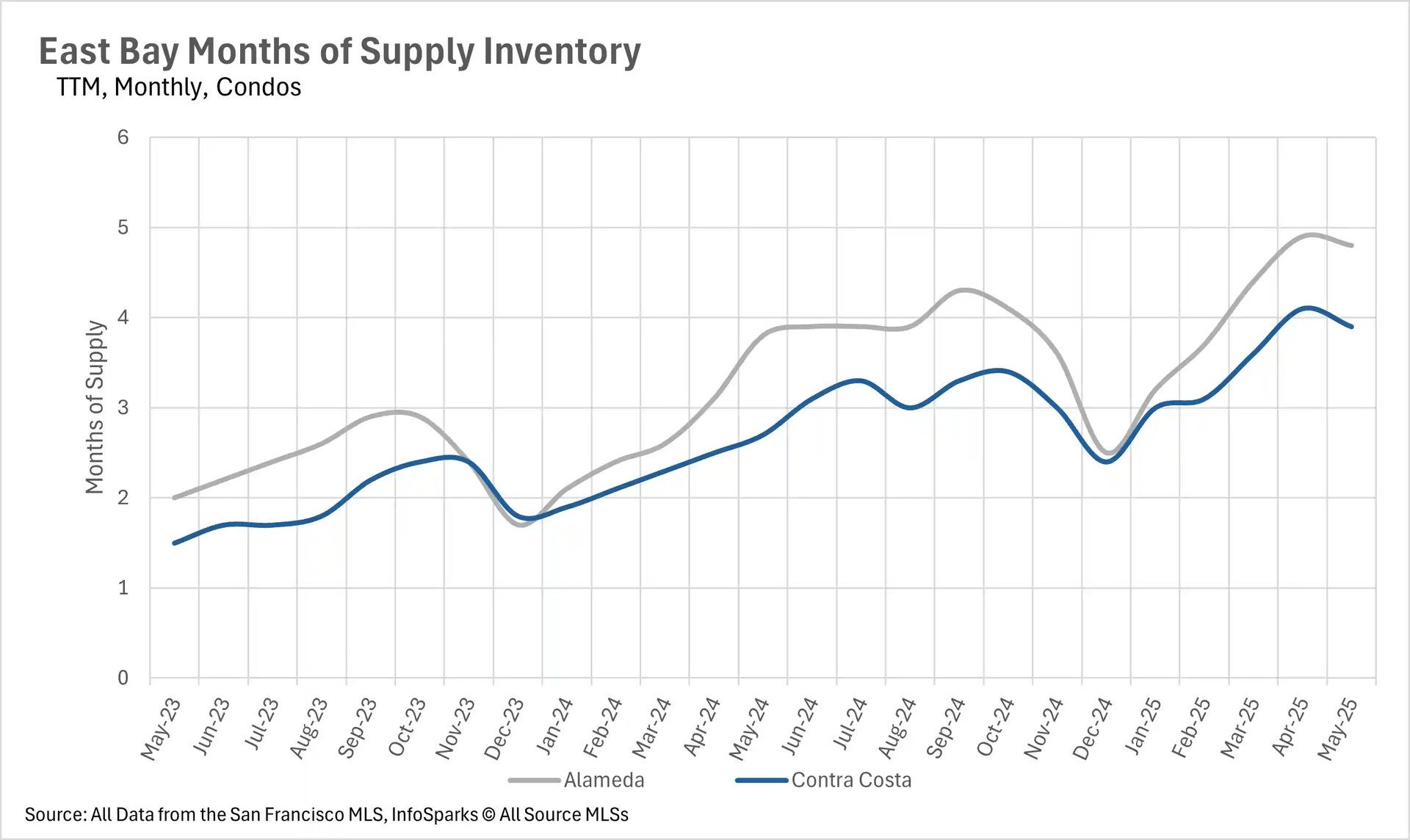

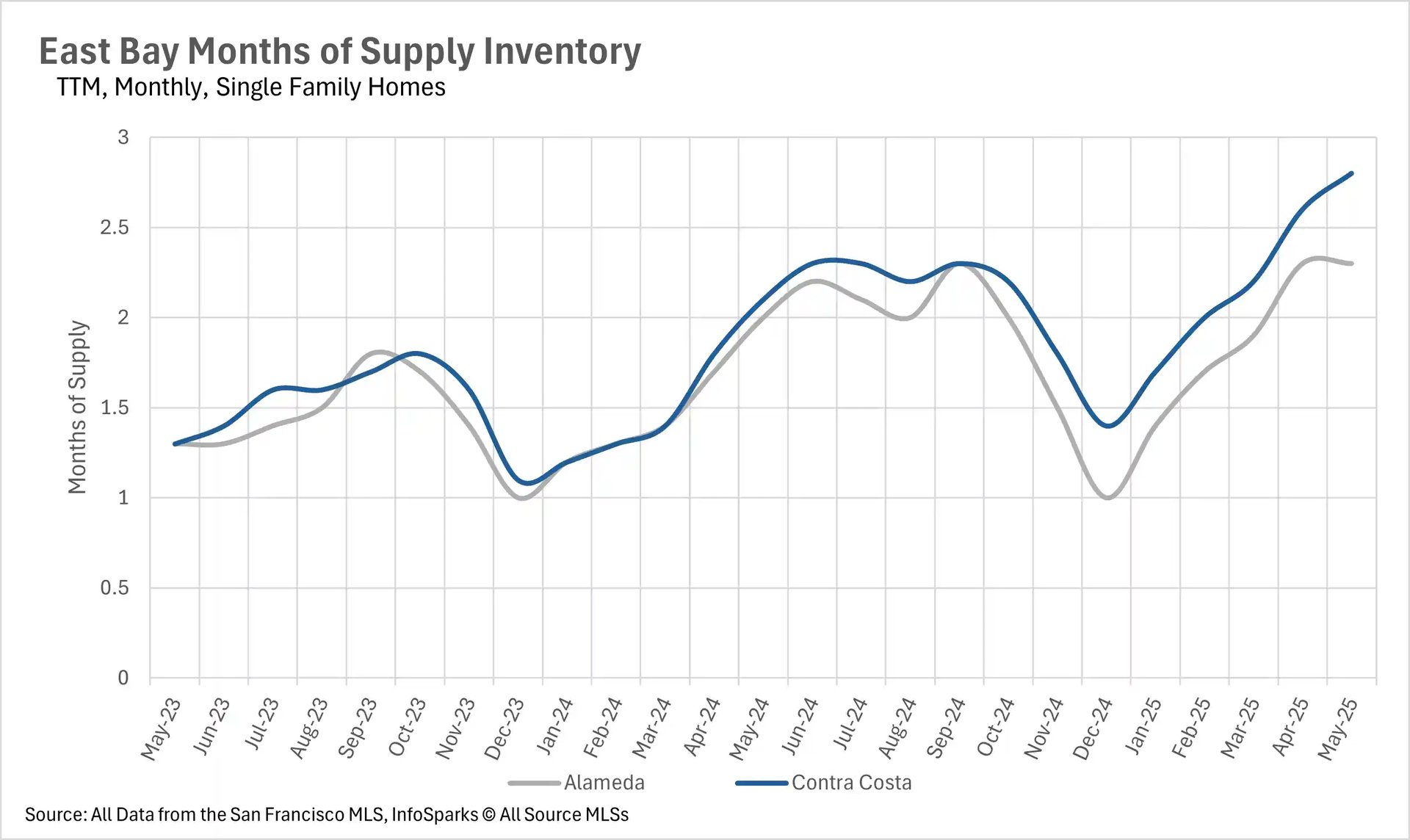

The East Bay continues its divided pattern with single-family homes at 2.3 months in Alameda and 2.8 months in Contra Costa (seller's markets), while condos favor buyers with 4.8 and 3.9 months respectively. The North Bay shows the most variation, with only Solano County (2.5 months) remaining a seller's market, Marin balanced at exactly 3 months, and Sonoma (3.5 months) and Napa (7 months) firmly in buyer's territory. This pattern suggests that across the Bay Area, single-family homes retain their premium status and seller advantage, while the condo market presents increasingly attractive opportunities for buyers willing to navigate longer search and closing timelines.