If you prefer to bypass The Big Story and jump straight to the Local Market Report, click here.

The Big Story

Quick Take:

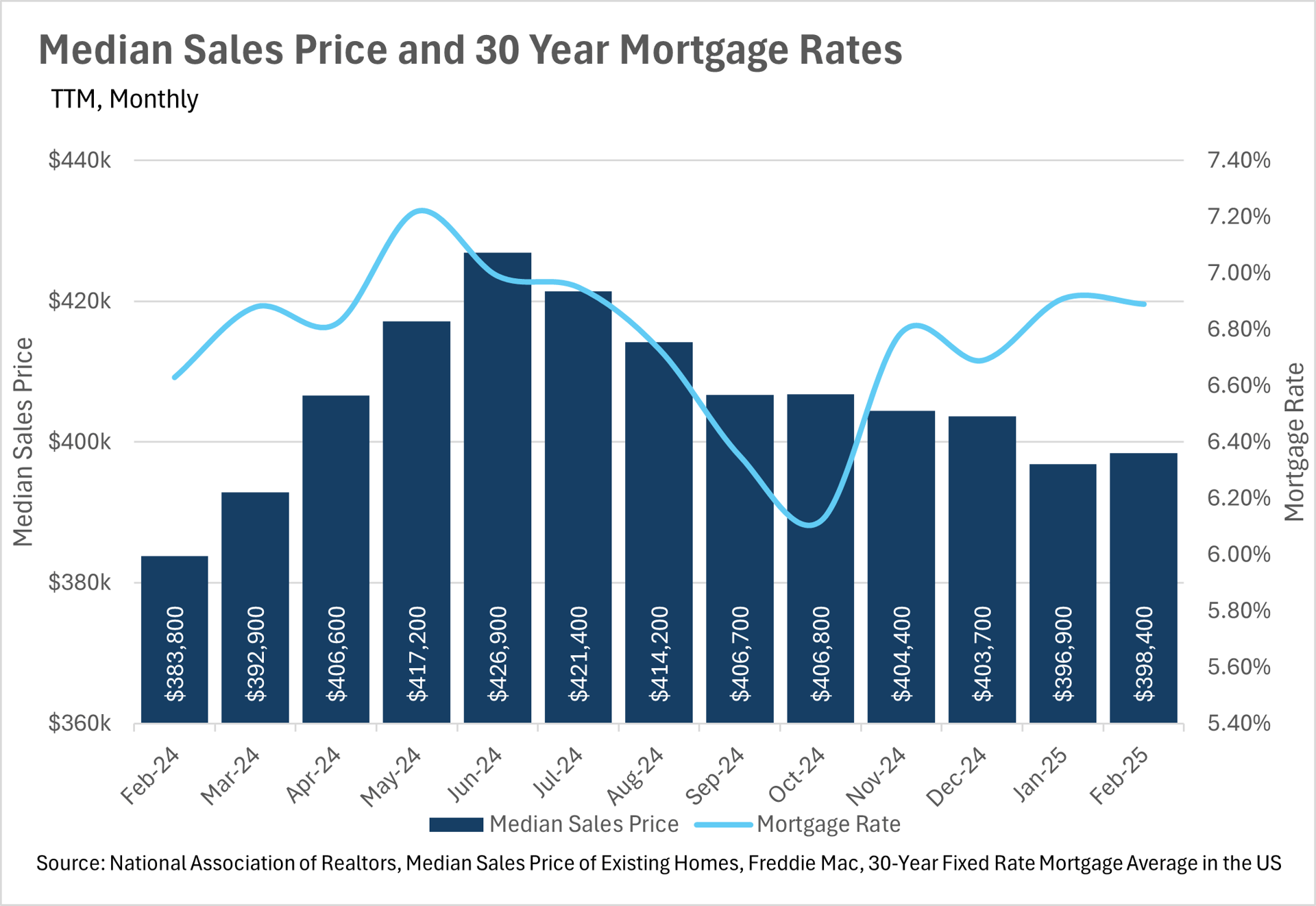

- Mortgage rates have ticked up slightly over the course of the past year, and coincidentally, so has the median sale price of a home in the US.

- According to Freddie Mac, the average 30-year mortgage rate is 6.62%, as of April 10th.

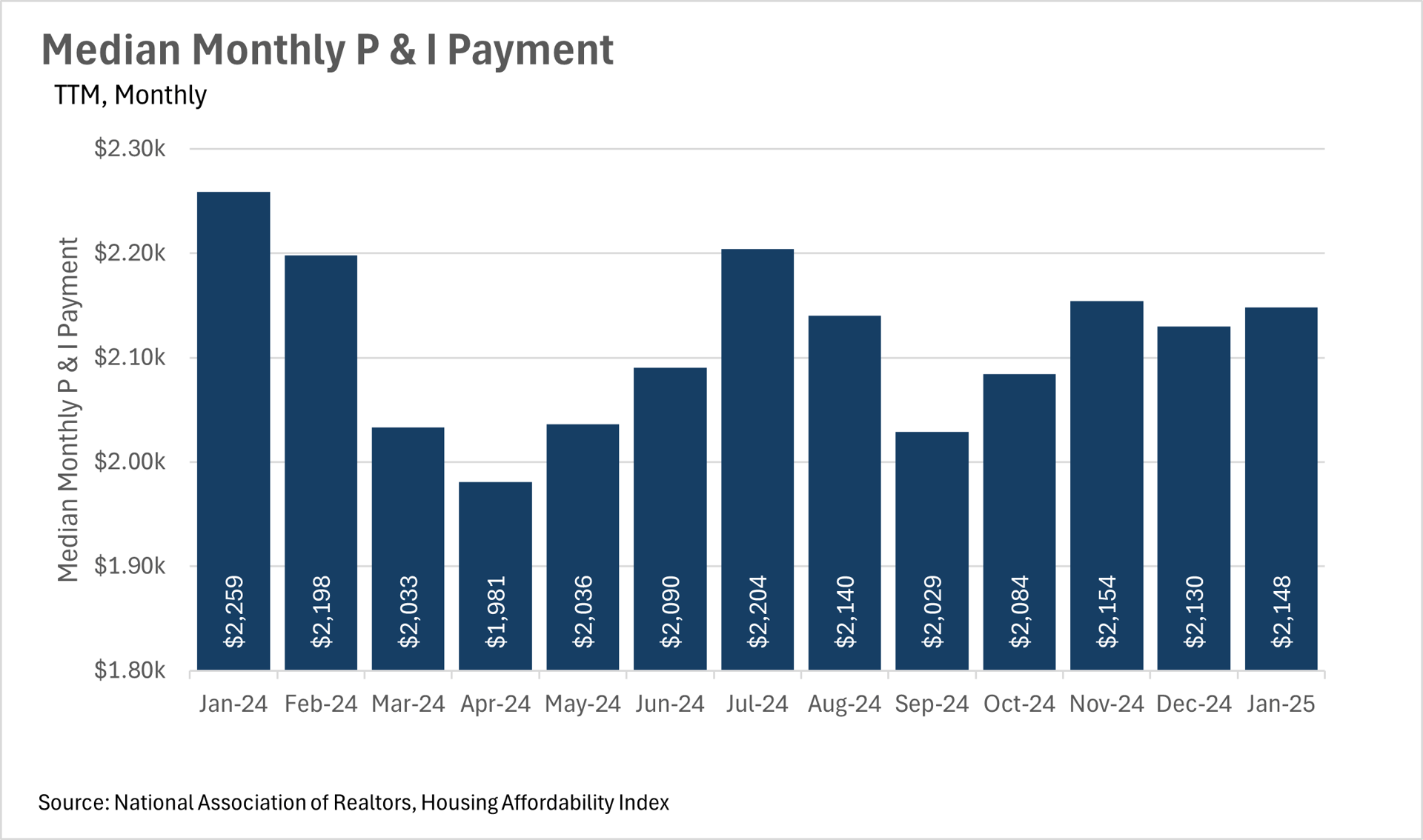

- Although affordability remains an issue throughout the country, the median monthly P&I payment has declined by over $100 on a year-over-year basis, representing a considerable savings for consumers!

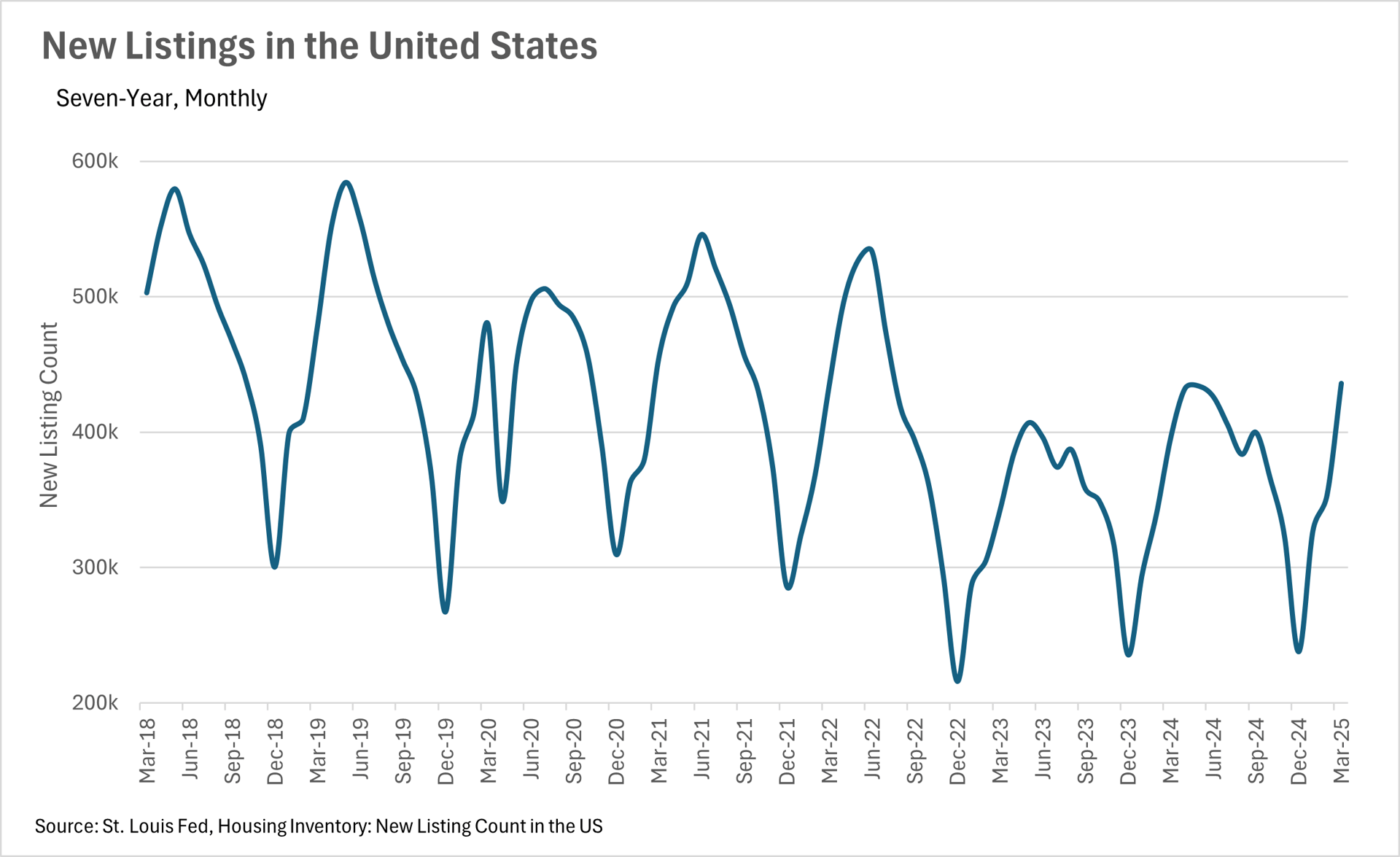

- We are seeing the trend of more new listings hitting the market continue, as we saw roughly 10% more new listings added in March when compared to a year ago.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

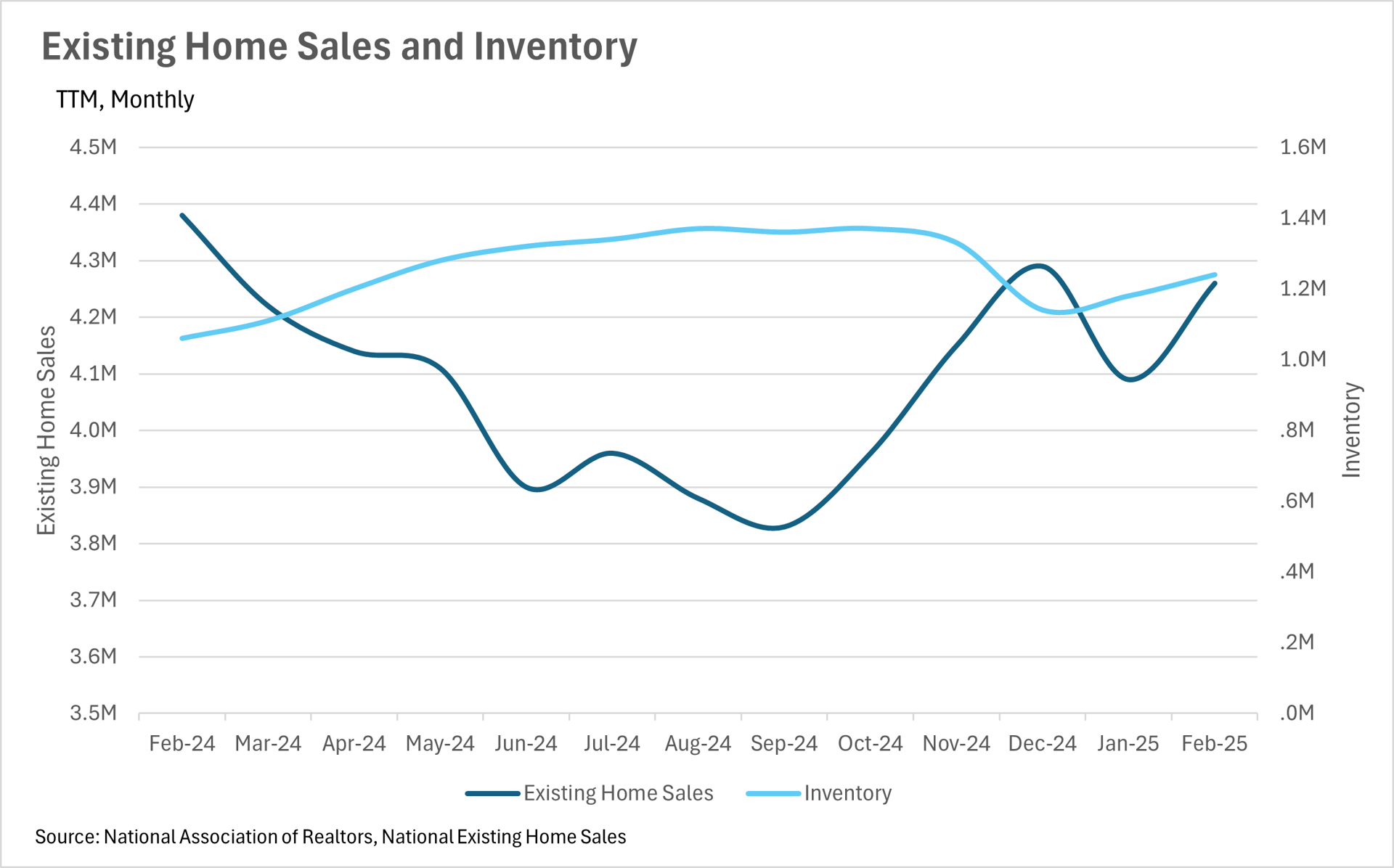

Home sales are roughly stagnant compared to last year

Although we are just about to exit the slow season for real estate sales, things are looking great overall. We saw a slight decrease in the number of sales on a year-over-year basis in February, with there being 4,260,000 sales in February 2025, compared to 4,380,000 in February 2024. However, on the flip side, we saw considerably more inventory added this year, with 1,240,000 homes on the market in February of this year, compared to 1,060,000 homes on the market around this time last year.

This means that all over the country, buyers have many more options than in recent years, which may lead to listings sitting on the market for a bit longer than what we’ve seen over the past couple of years. When you couple this with the fact that there are more new listings being added to the market, with just over 10% more listings added in March of 2025, compared to March of 2024, we might see some power start moving away from sellers to the buyers.

Additionally, this uptick in new listings might be an indication that sellers are starting to accept the fact that considerably lower mortgage rates aren’t coming anytime soon. Although many were holding out hope over the course of the past couple of years, the Fed has made it very clear that they’re not looking to drop rates by a considerable margin anytime soon. This, of course, means that prospective sellers have an important choice to make - whether they should sell, or continue holding out. From the data that we’re seeing, it seems that many sellers are beginning to choose the former option!

When turning to affordability, we saw a rather interesting phenomenon - median monthly P&I payments decreased by nearly 5%, all while interest rates and median sale prices increased by just under 4%. This likely means that there was a considerable cohort of homeowners out there that locked in rates toward the end of 2023 when rates were at a local high, and recently refinanced when rates came down a bit. The median consumer having an additional $100 in their pocket each and every month is a great thing for the economy, especially when we face economic uncertainty, tariffs, and ever-changing geopolitics!

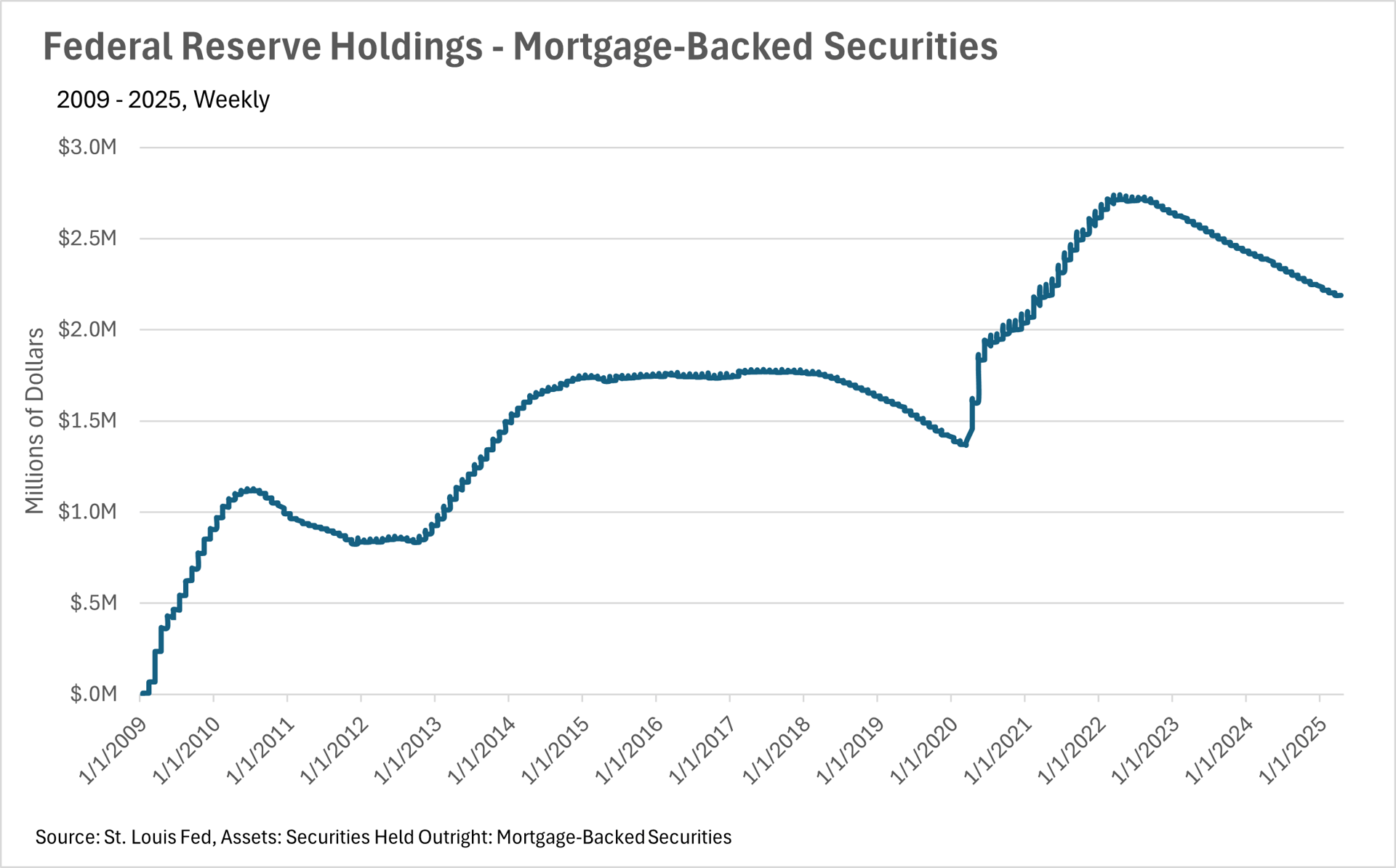

Lastly, it’s important to note that it’s business as usual in terms of the Federal Reserve. In their recent FOMC meeting, they decided to hold the federal funds rate firmly where it has been over the past couple of months. Fed officials also indicated that they are not in a rush to lower rates by a considerable margin anytime soon. However, that could always change, as we’re living in an incredibly dynamic era right now! Additionally, the Fed is continuing to offload mortgage-backed securities at a steady pace!

Ultimately though, this is just what we’re seeing at a national level. As we all know, real estate is an incredibly localized industry, so knowing what’s going on in your own market is pivotal. Below is our local lowdown, that outlines everything you need to know about what’s happening around you in your neighborhood and surrounding areas!

Big Story Data

The Local Lowdown

Quick Take:

- Housing markets across the Bay Area show mixed signals, with single-family homes outperforming condos in most regions.

- Inventory trends vary significantly by region, with Silicon Valley seeing increases while San Francisco continues to struggle with low supply.

- Single-family homes in most Bay Area regions remain in a seller's market, while the condo market generally favors buyers with higher months of supply inventory.

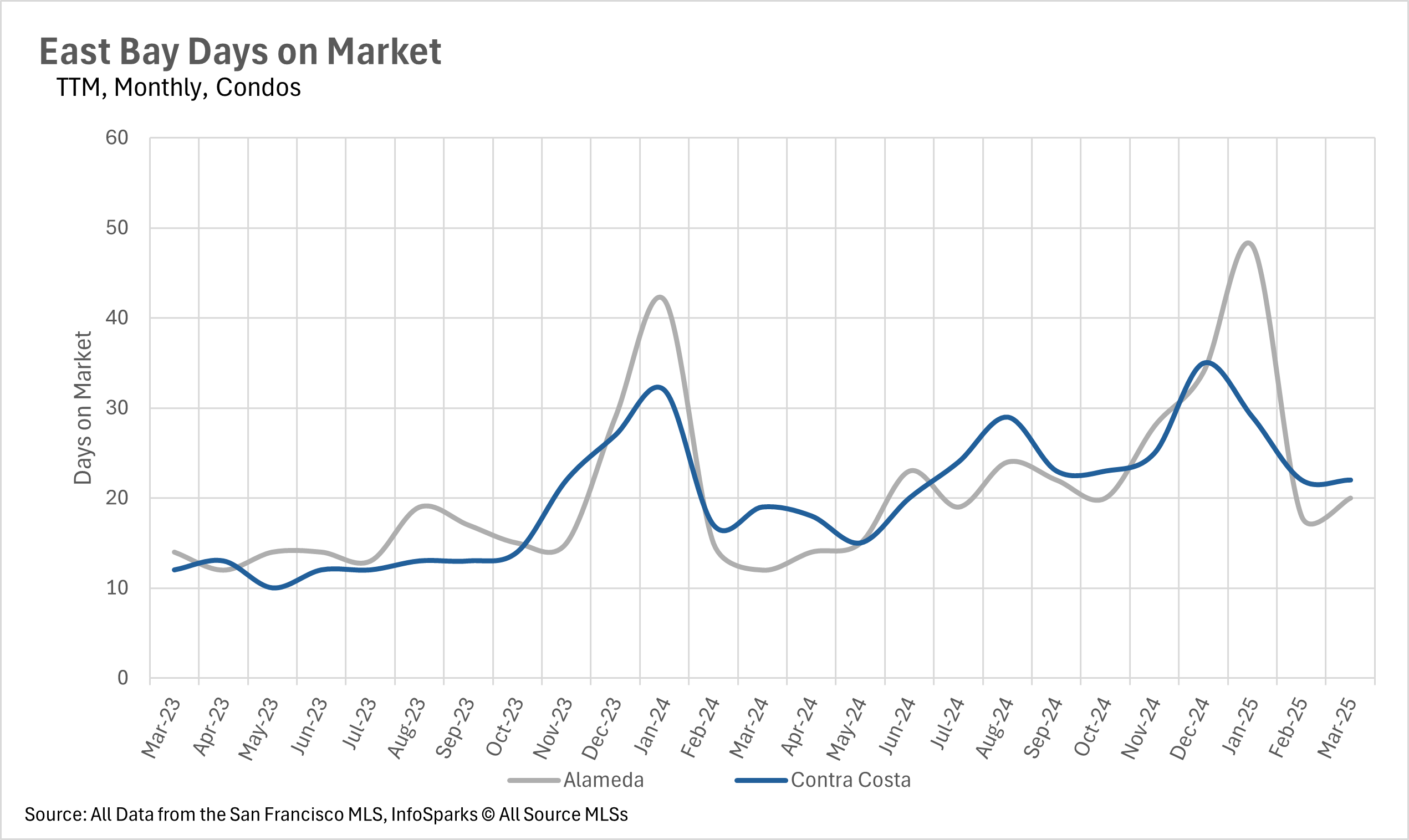

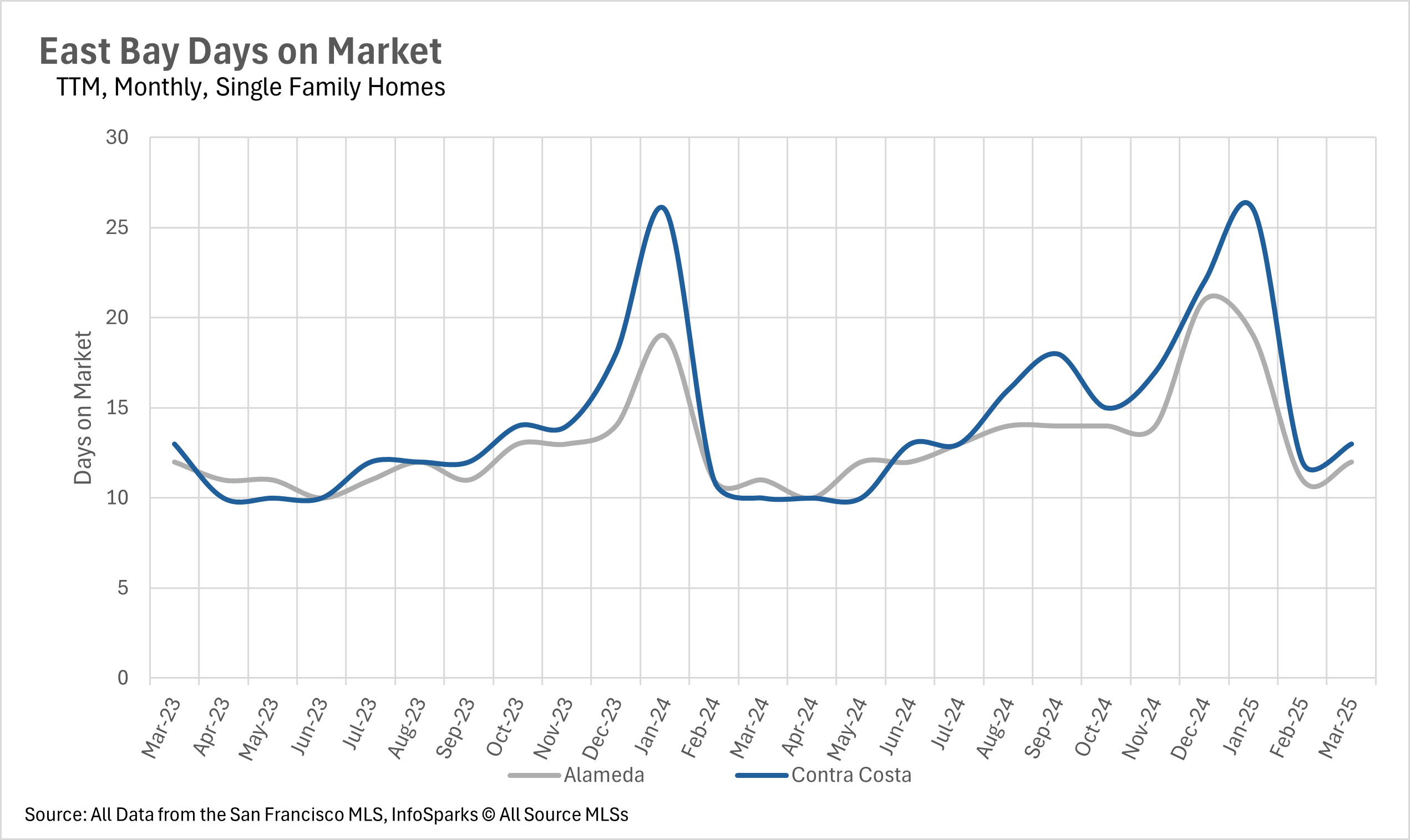

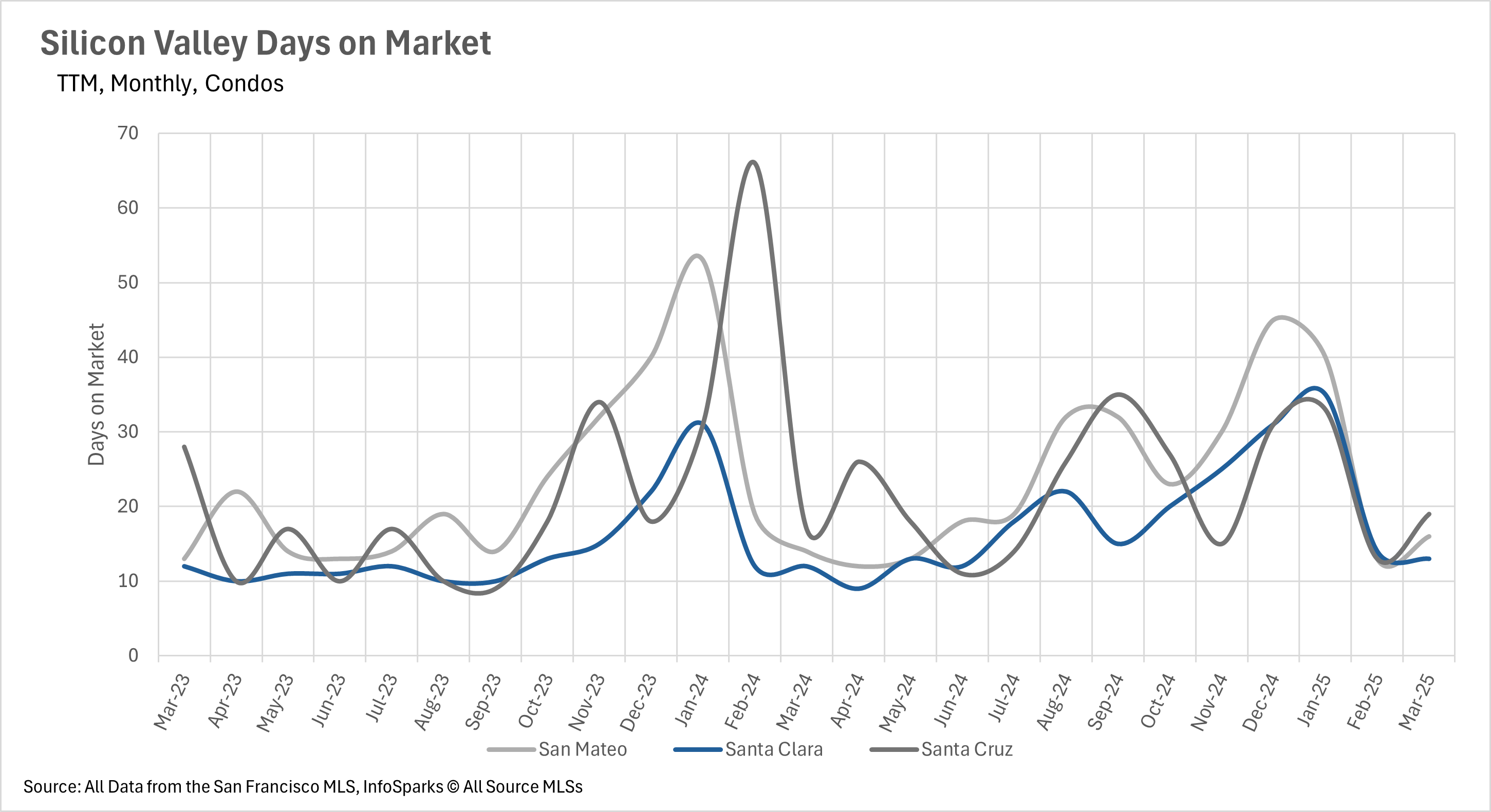

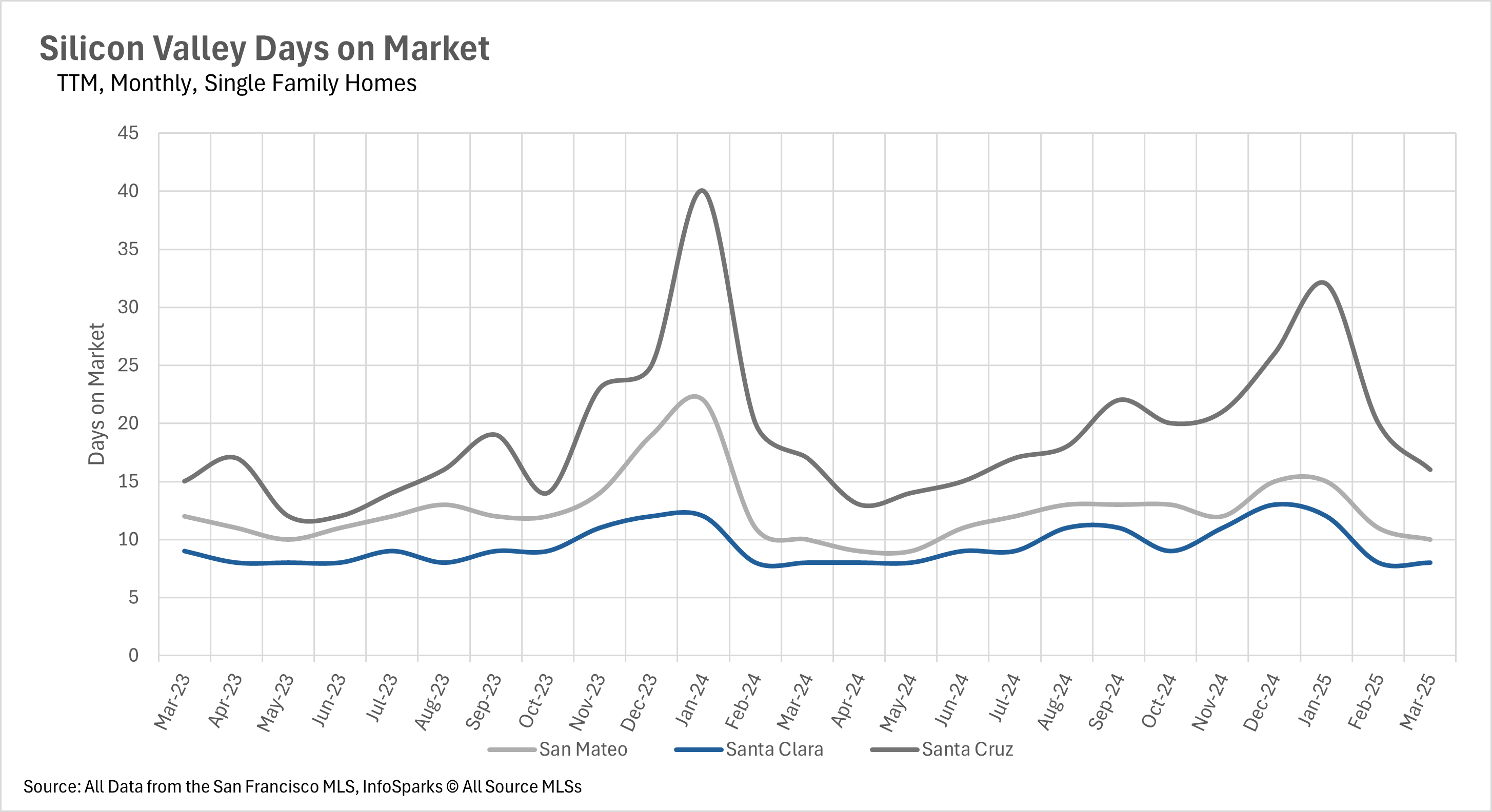

- Days on market vary dramatically across the Bay Area, from just 8-16 days in Silicon Valley to significantly longer timeframes in other regions.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Bay Area home values show divergent trends across regions

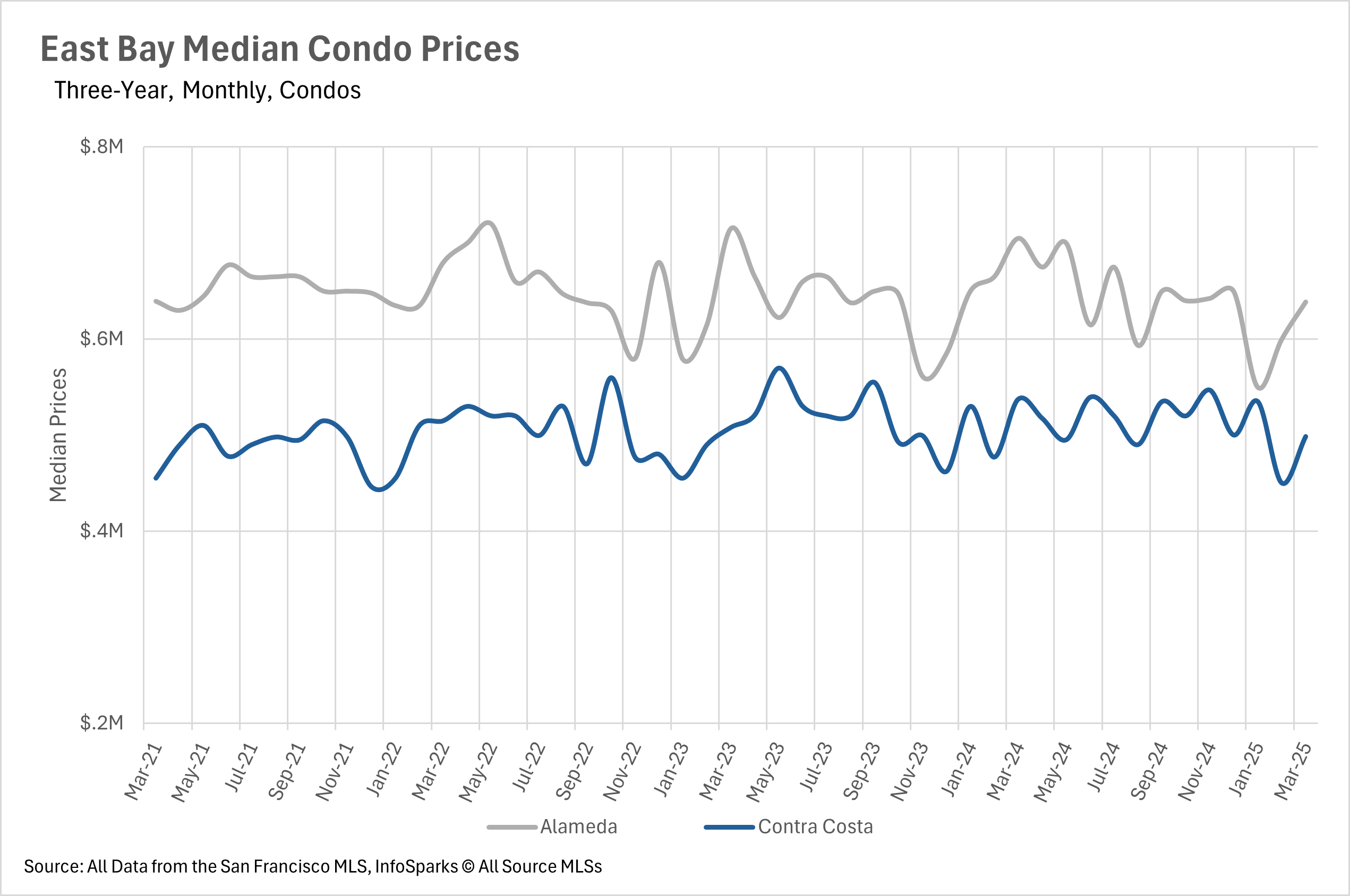

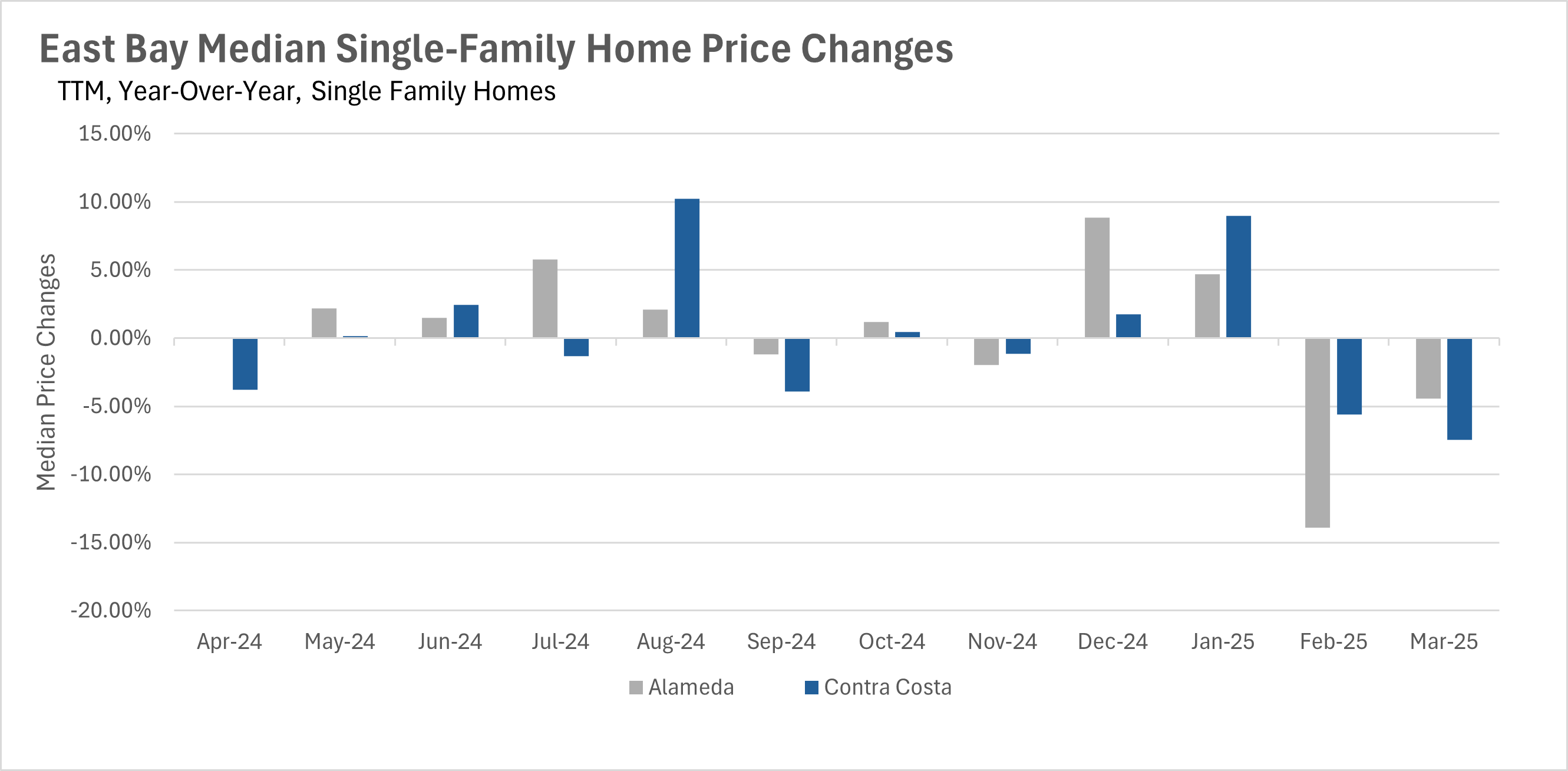

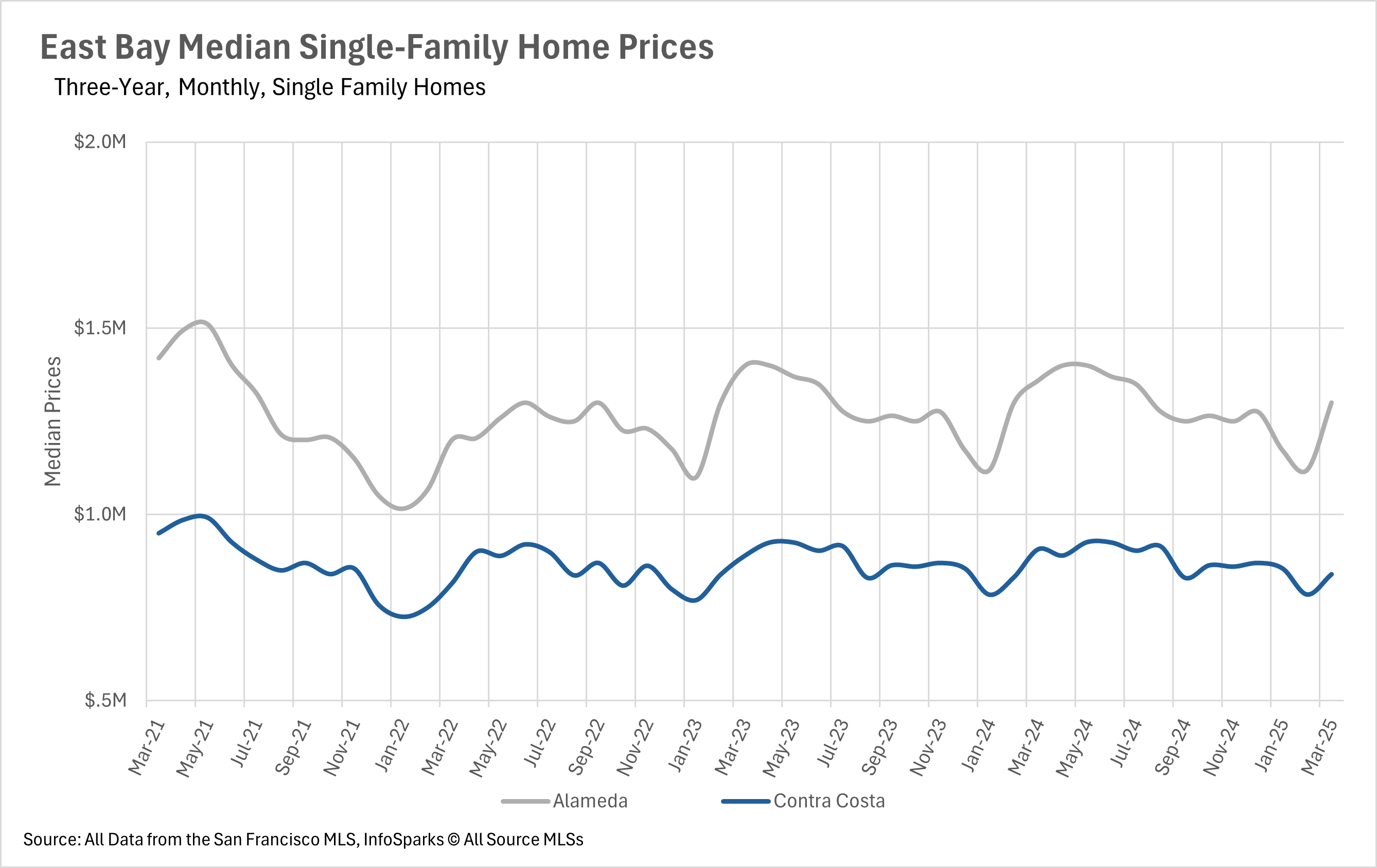

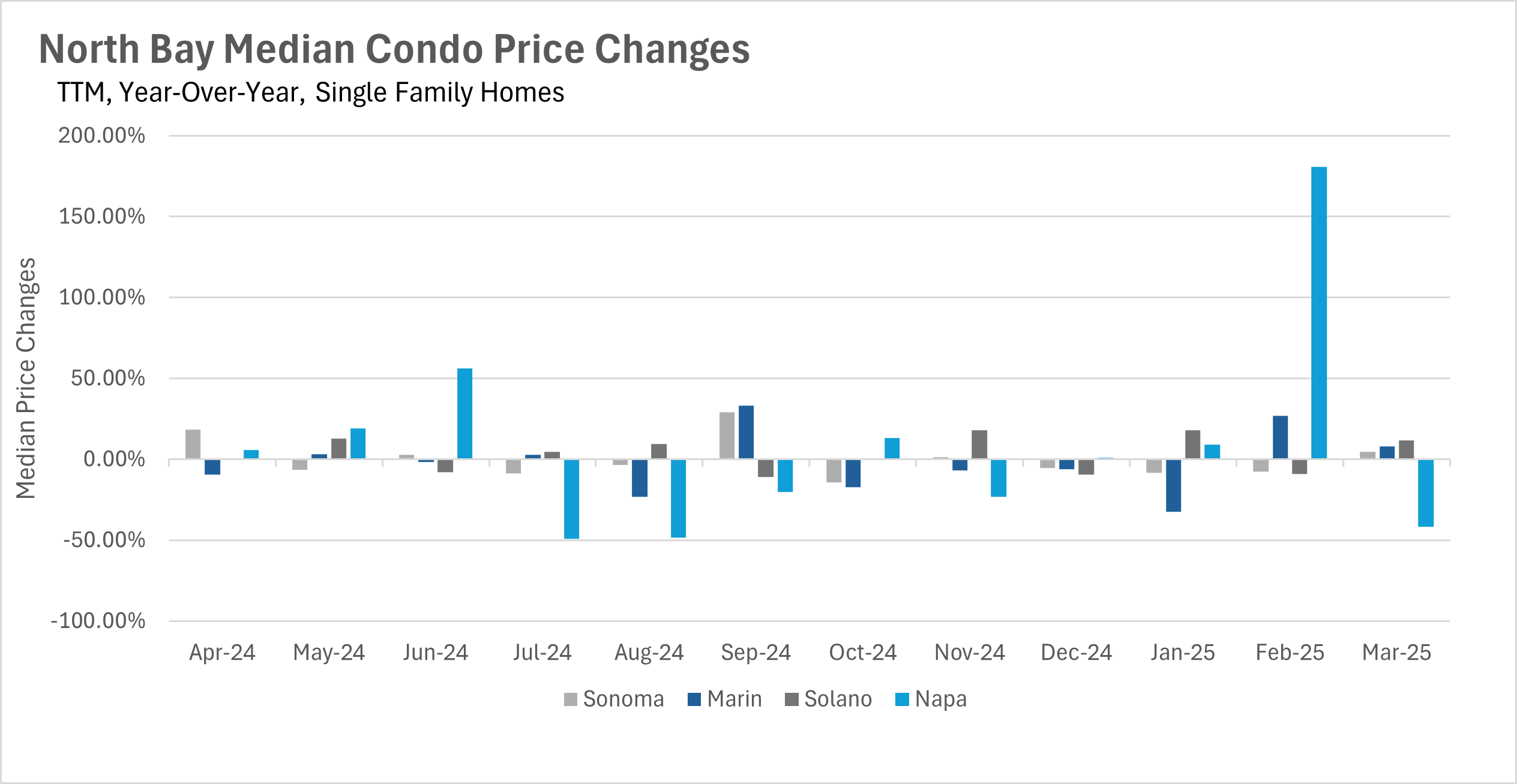

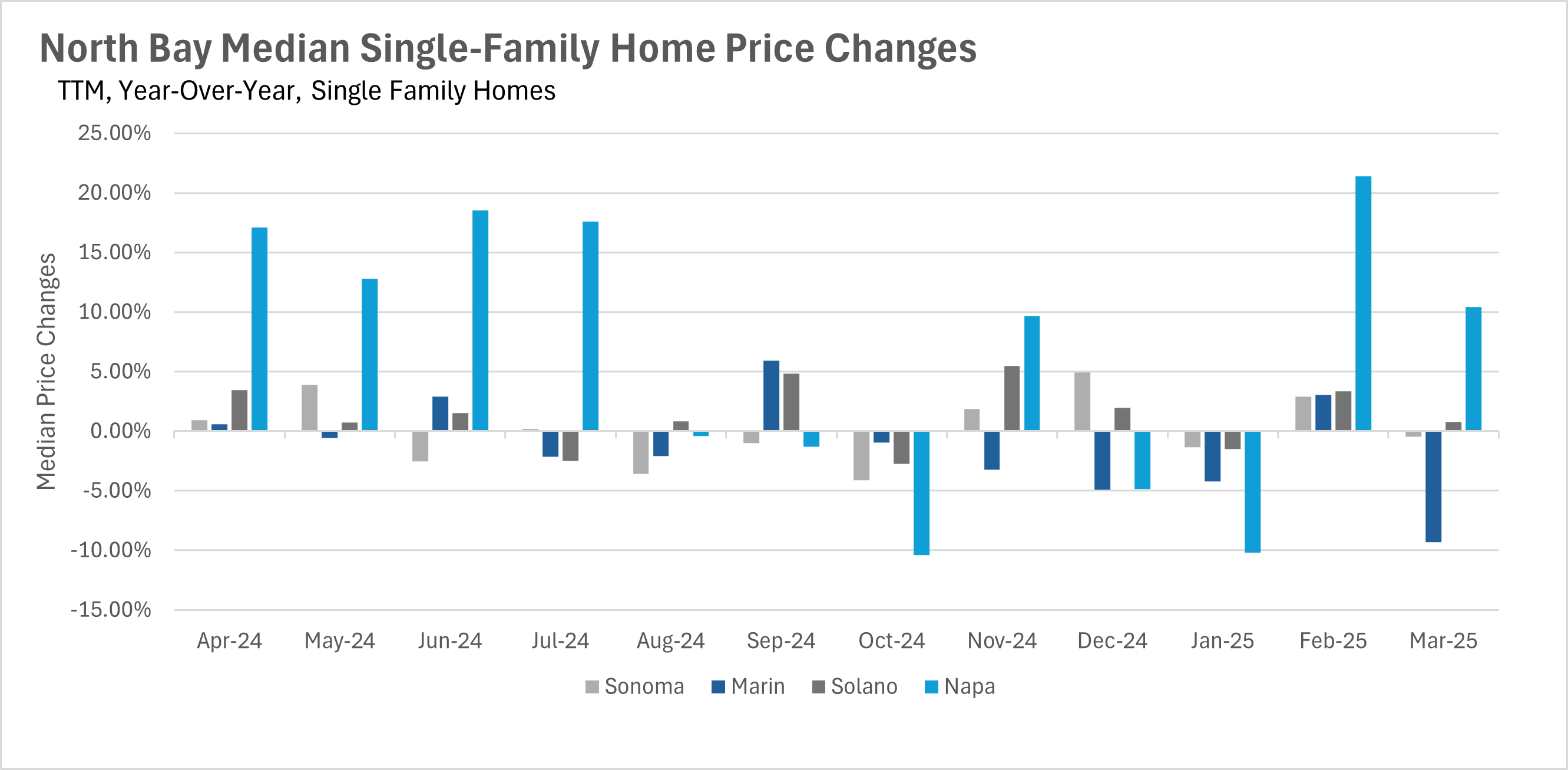

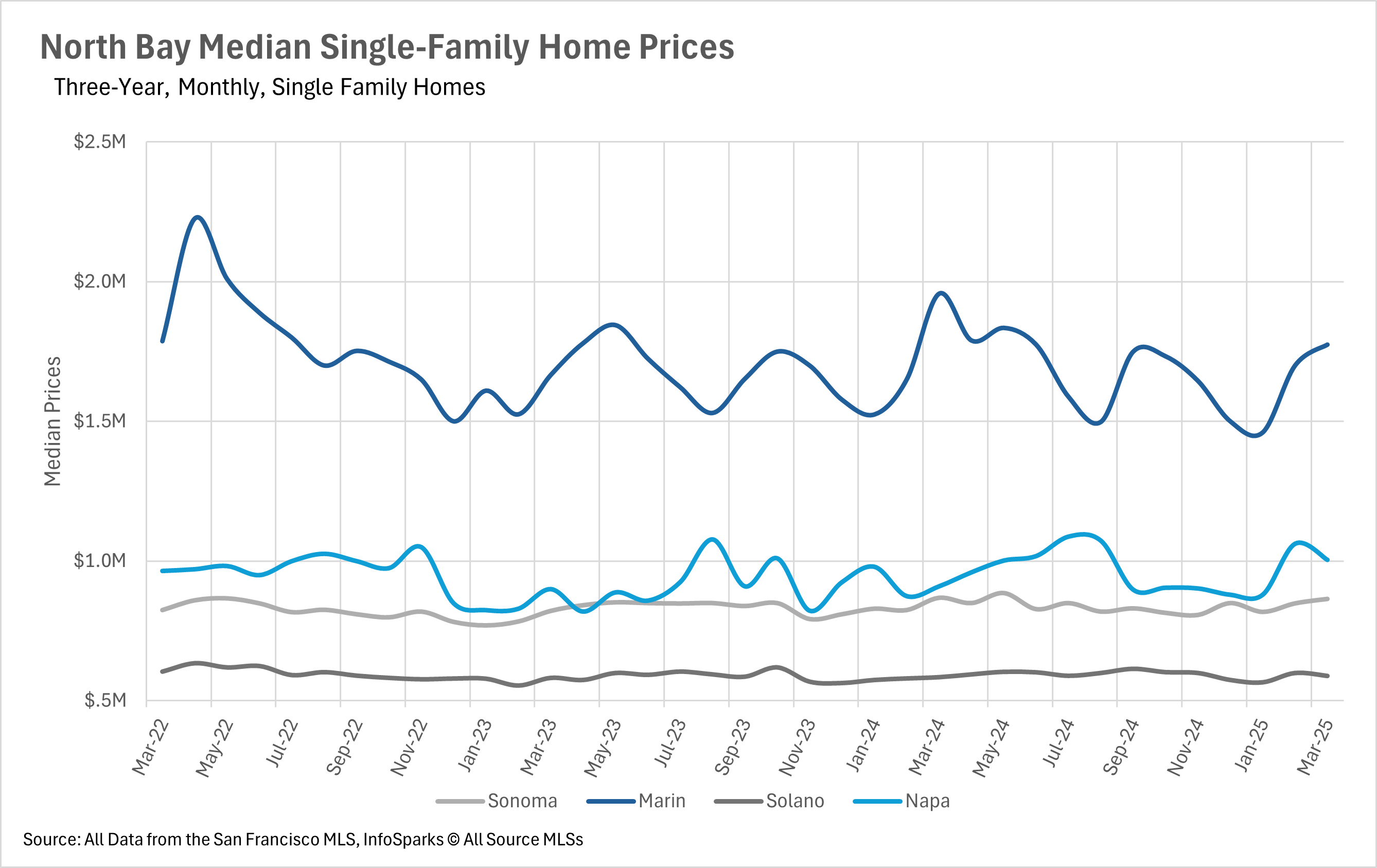

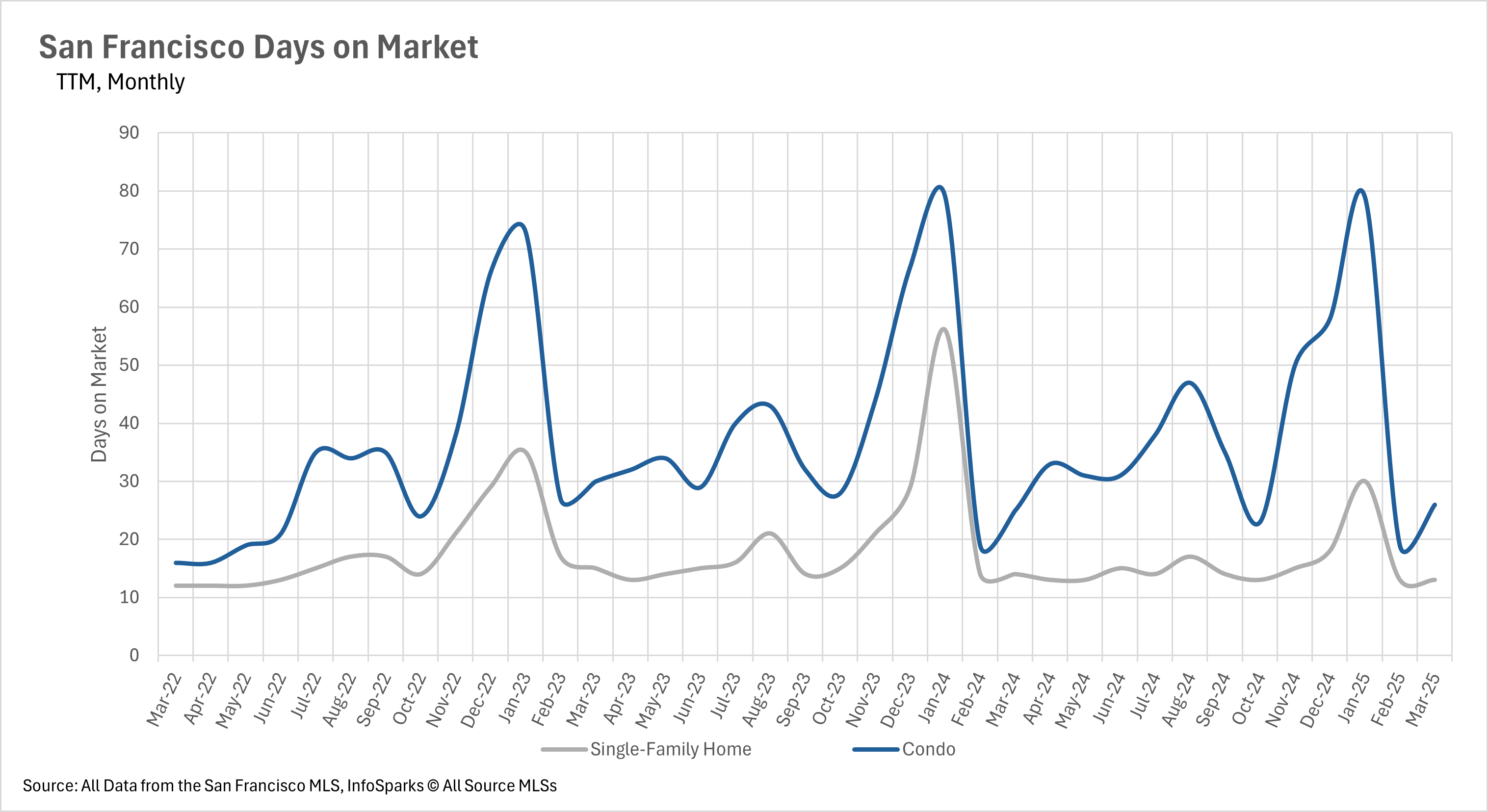

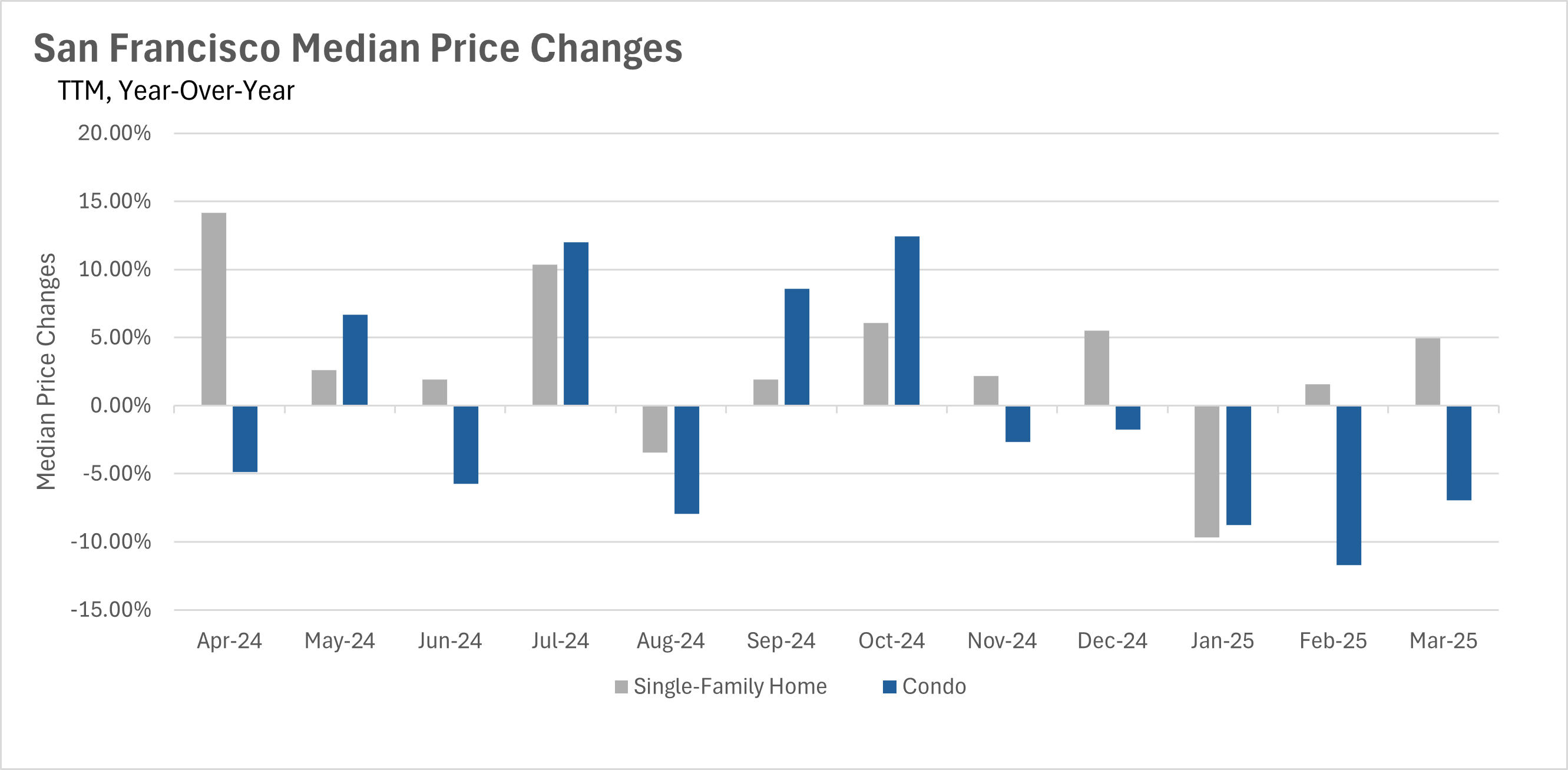

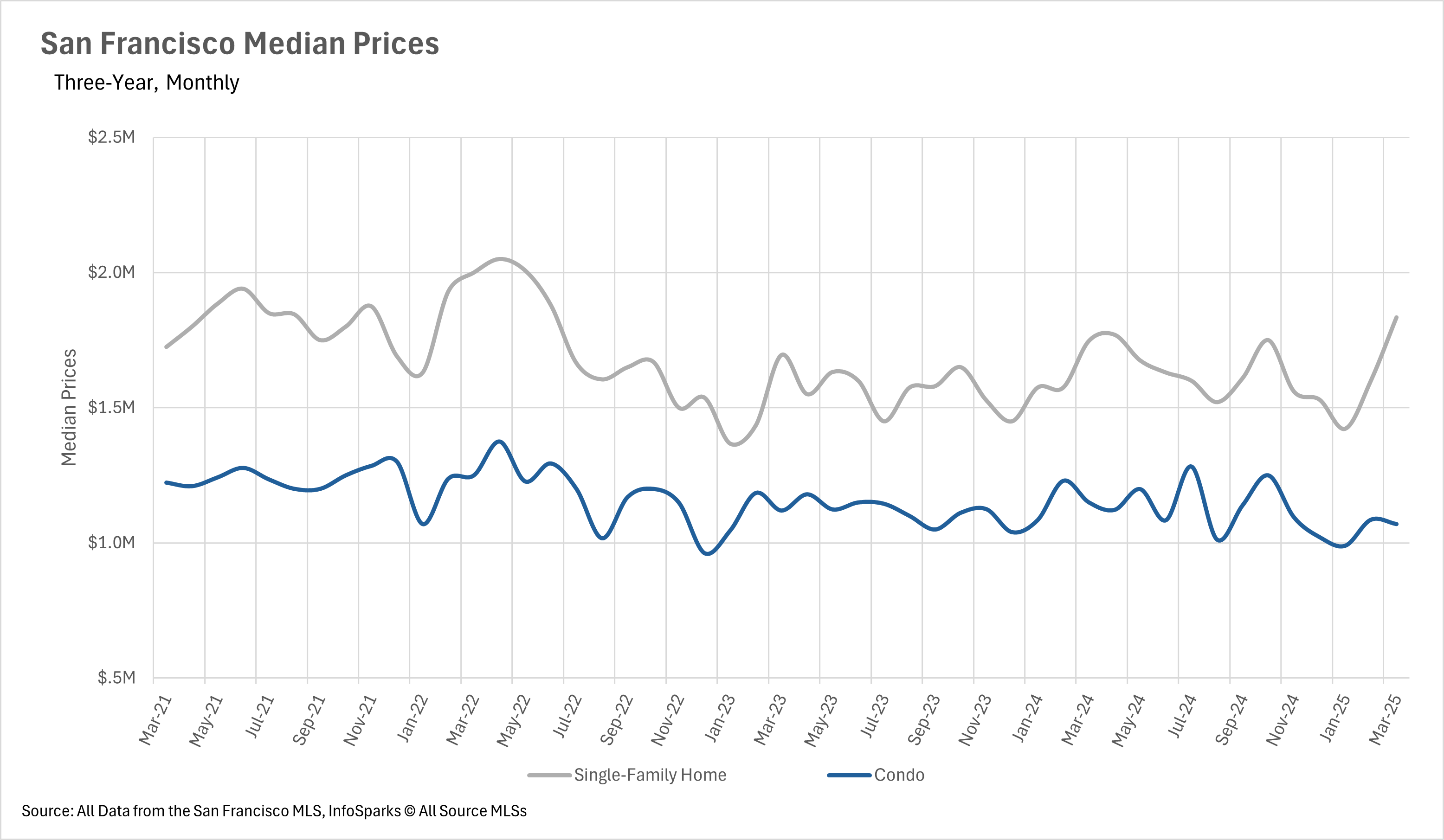

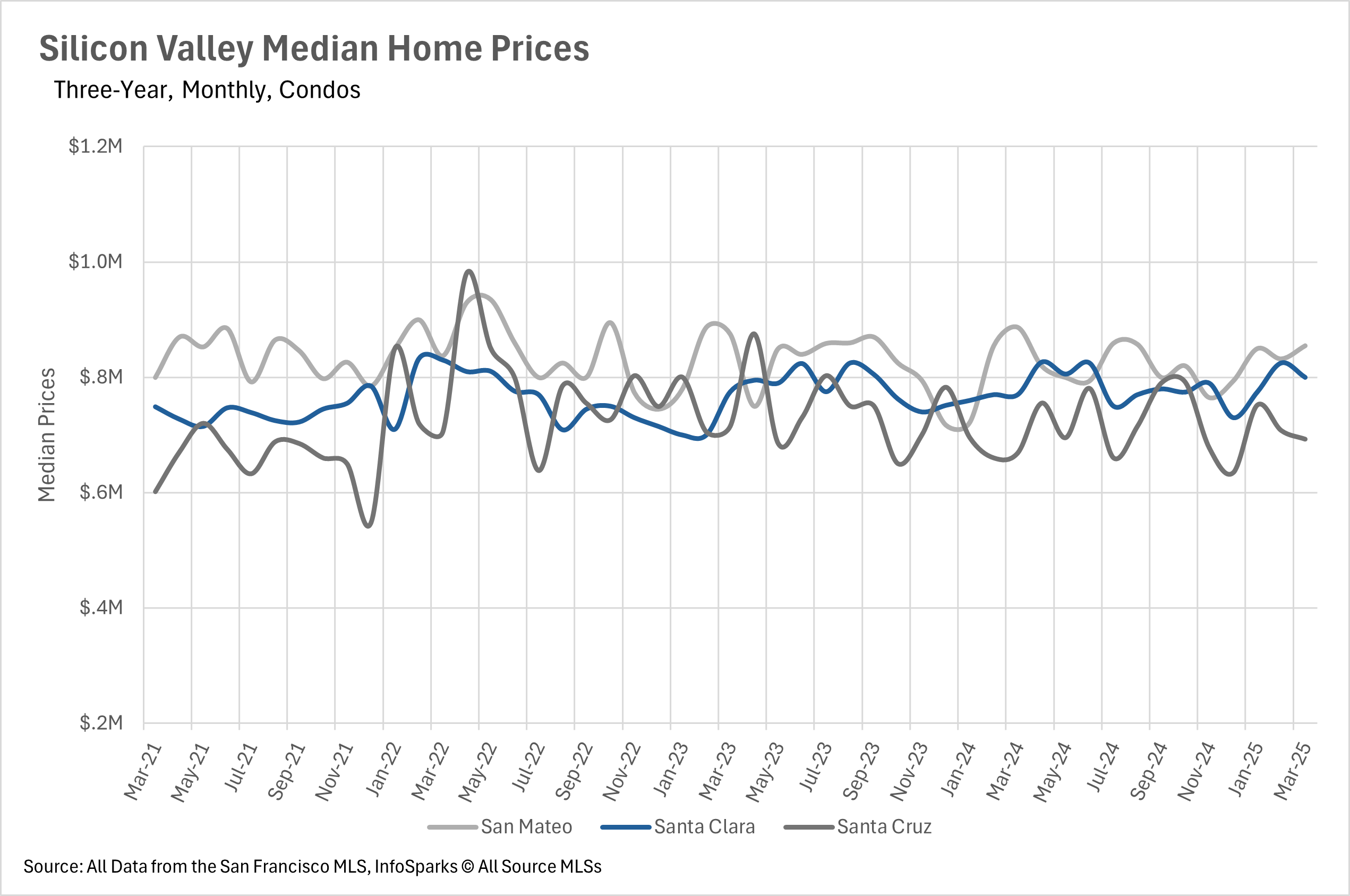

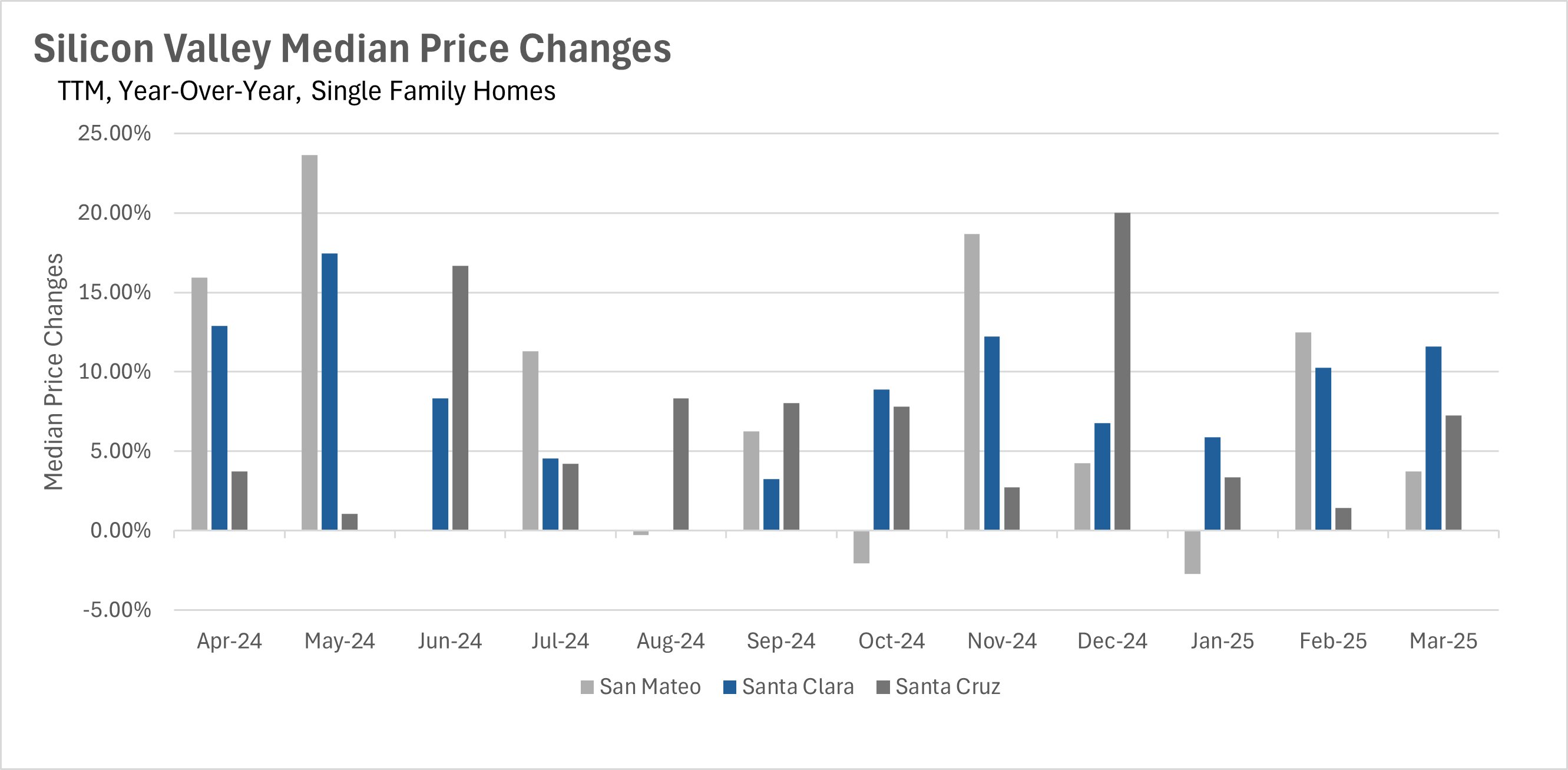

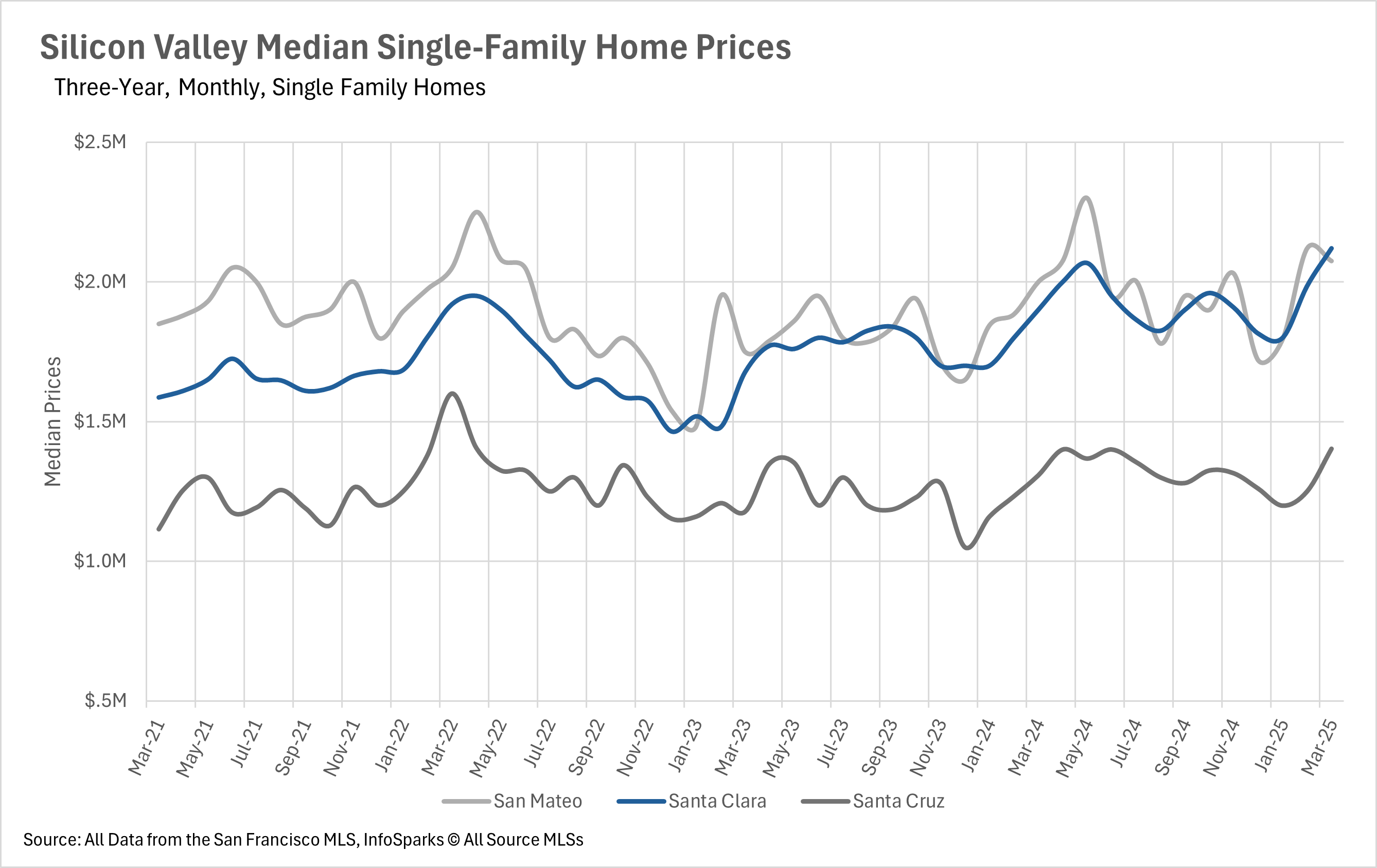

The Bay Area real estate market is showing varied performance across its different regions. Silicon Valley continues to be a hotspot for growth, with Santa Clara County experiencing an impressive 11.58% year-over-year increase in median sale price in March. San Mateo and Santa Cruz counties also saw healthy increases of 3.75% and 7.27%, respectively. In contrast, the East Bay market has cooled somewhat, with year-over-year median sale prices dropping by 4.41% in Alameda County and 7.44% in Contra Costa County, though month-over-month trends remain positive. San Francisco presents a tale of two markets, with single-family homes maintaining their value (increasing 6.63% over four years) while condo values have declined by 12.52% over the same period, highlighting buyer preference for detached homes over shared buildings.

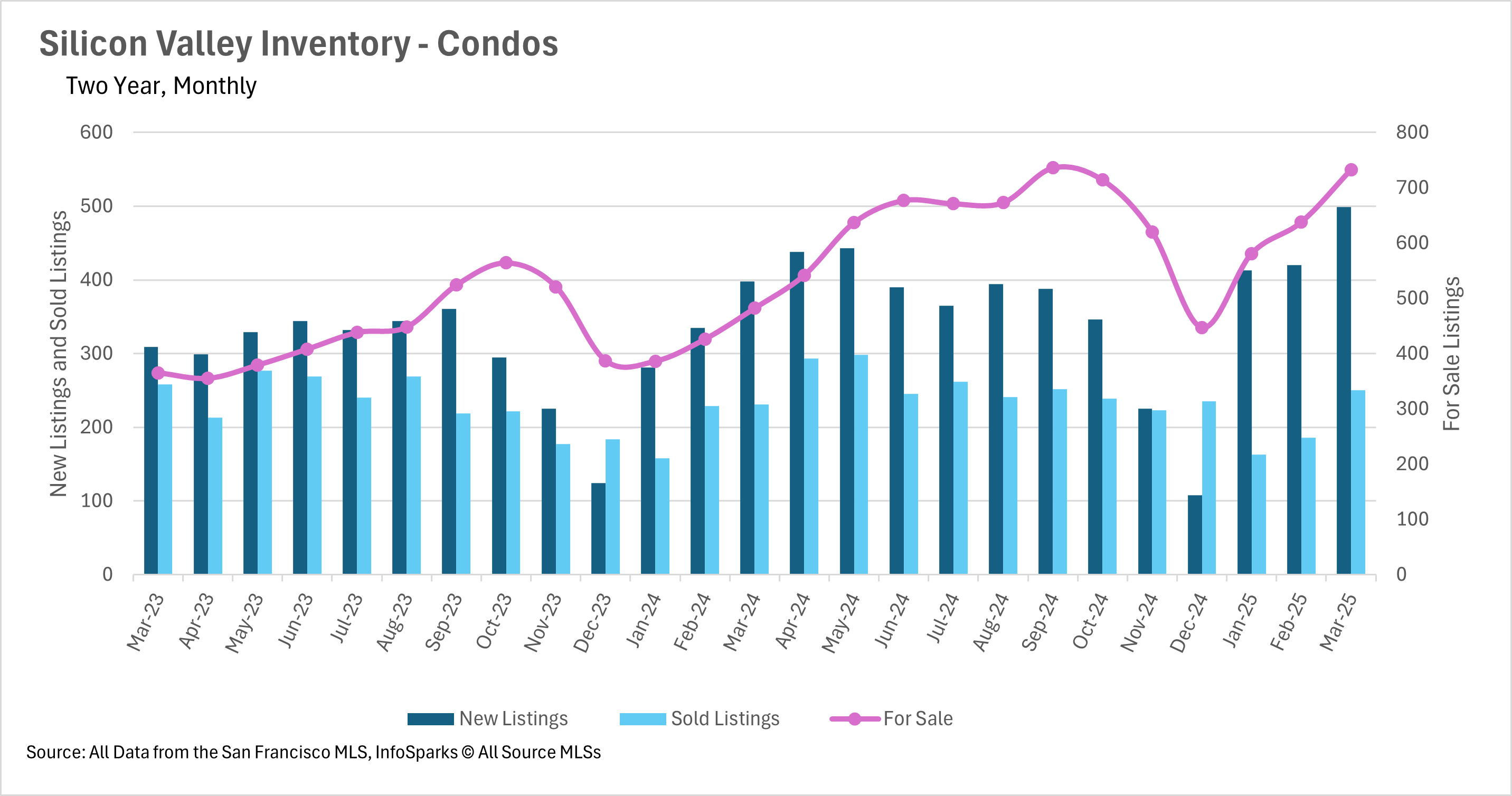

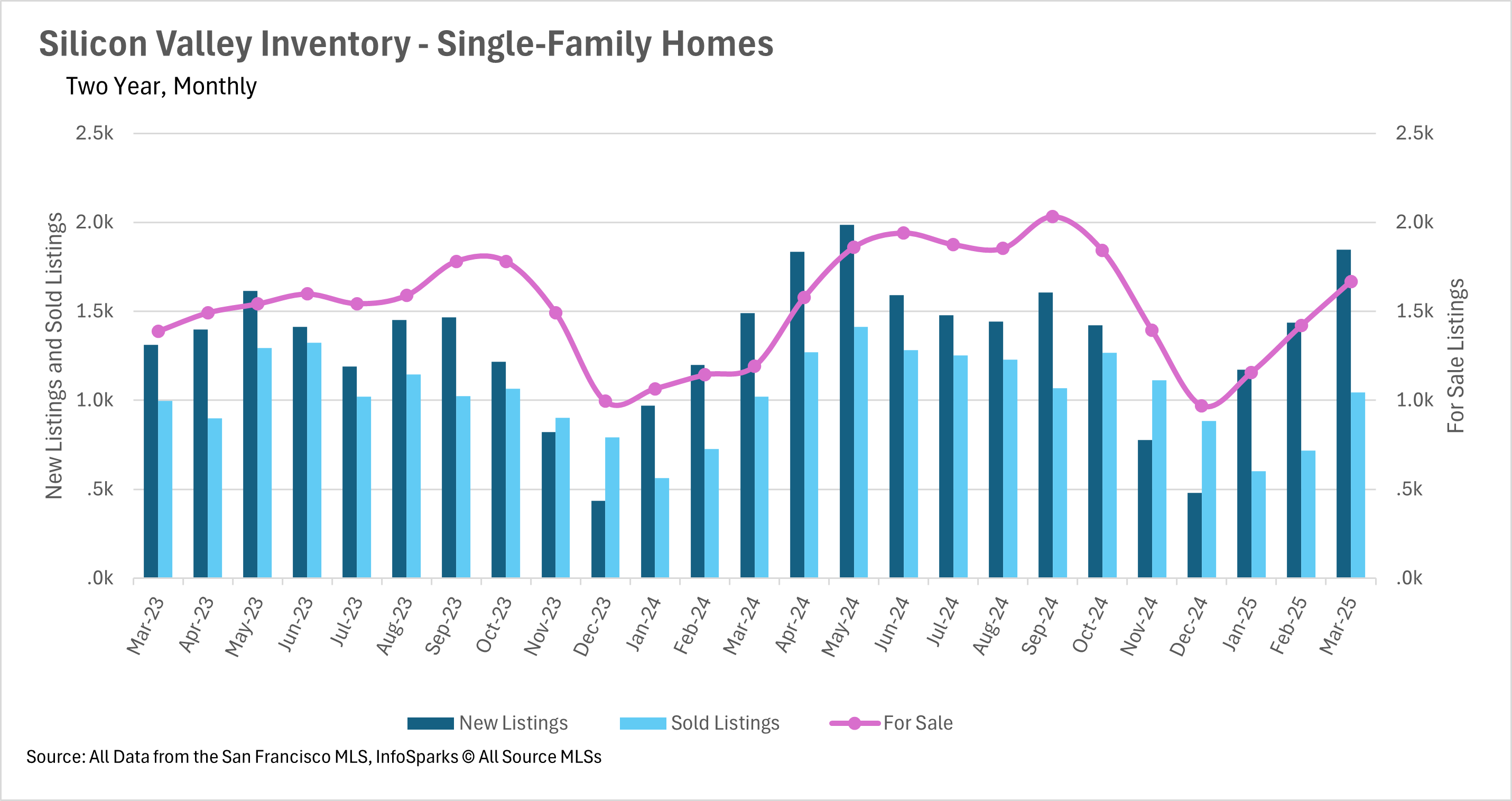

Inventory levels and new listings show regional variations

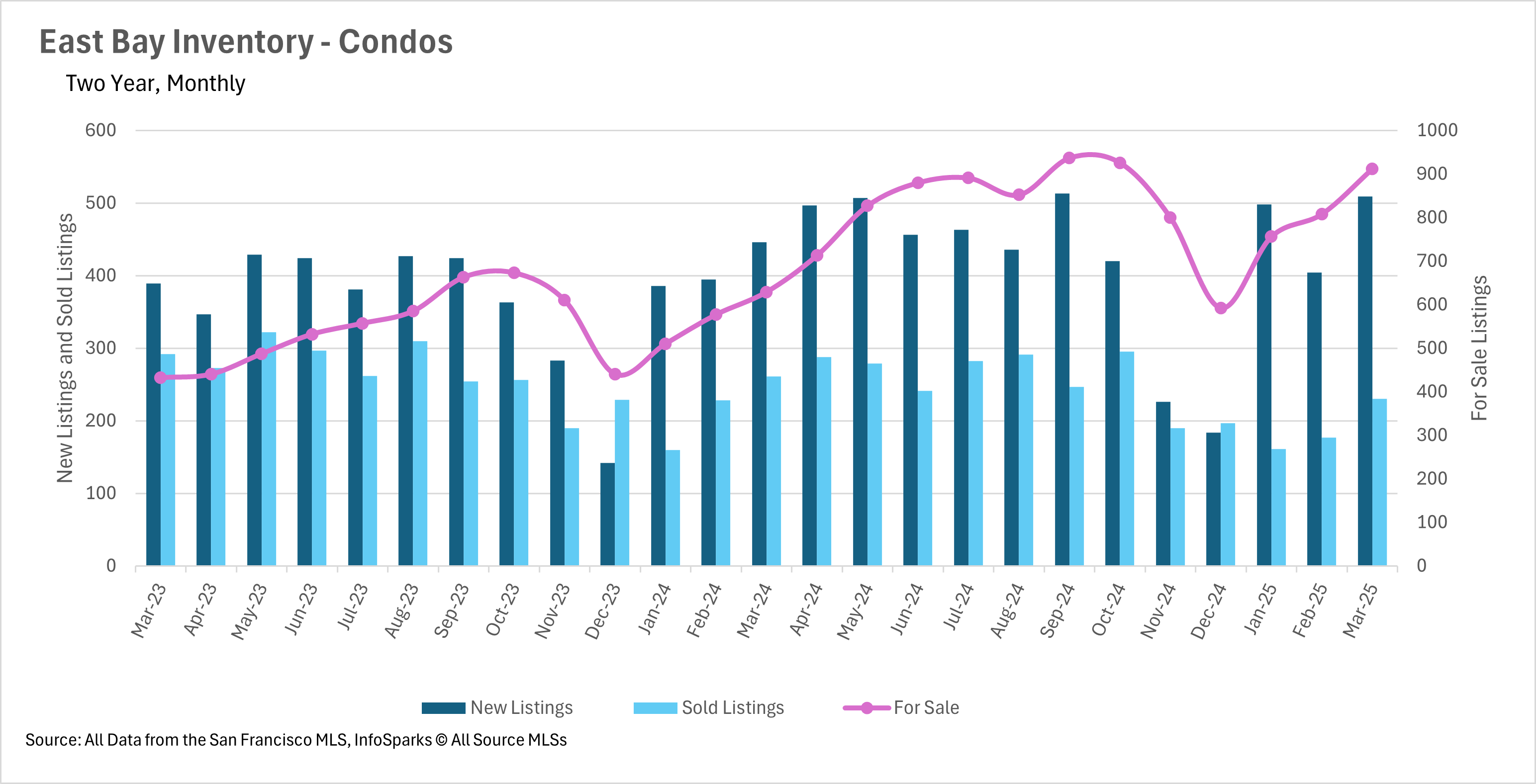

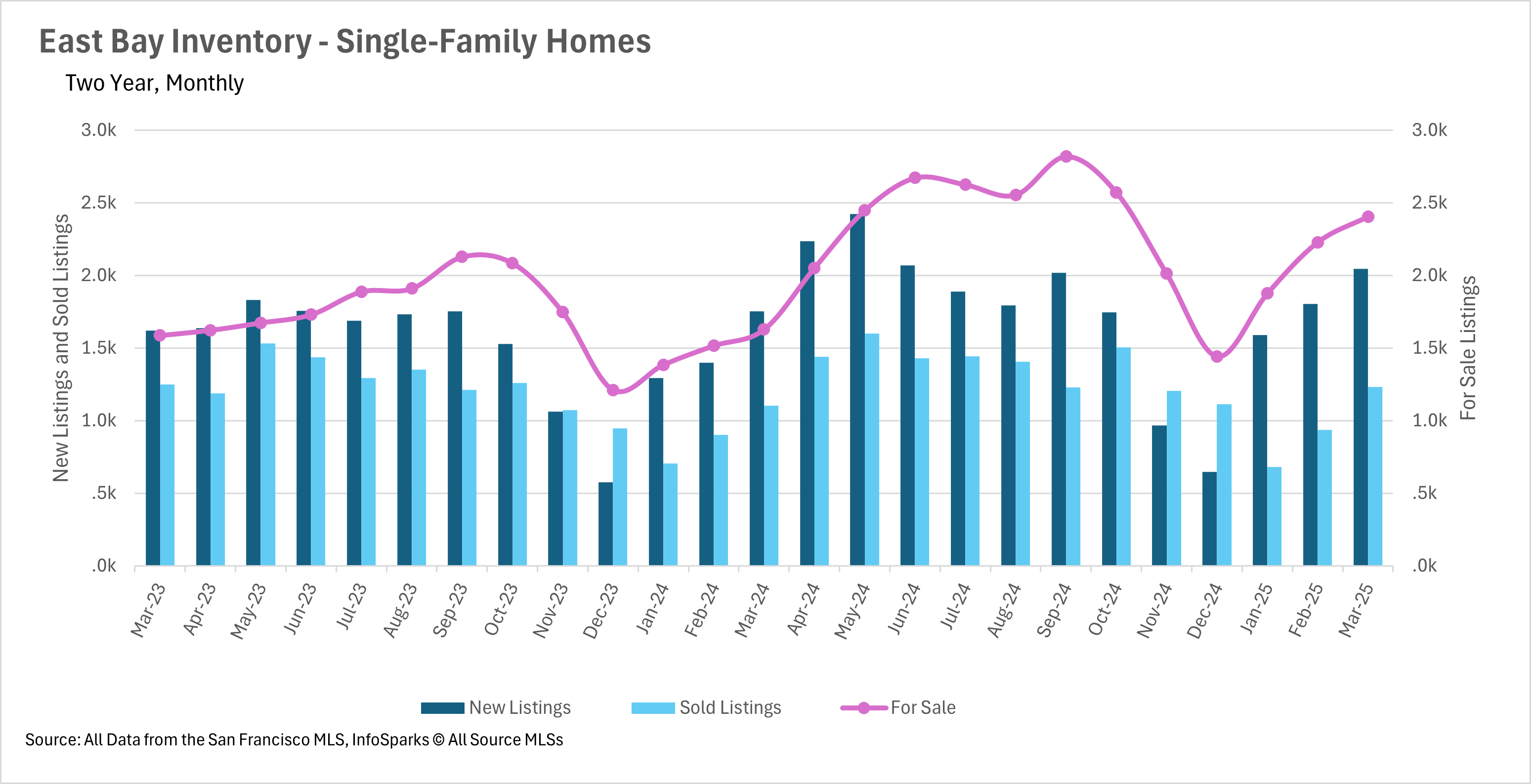

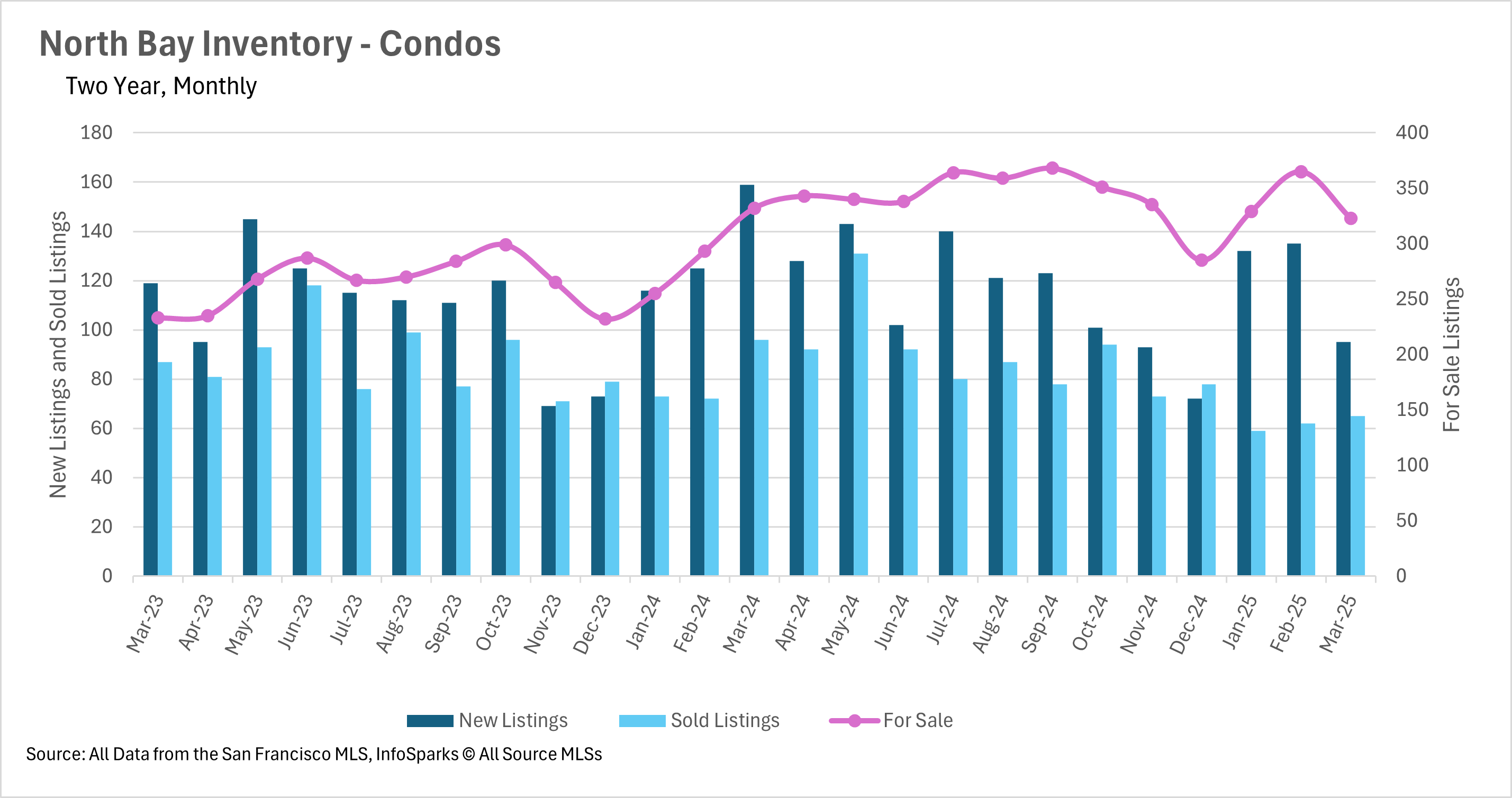

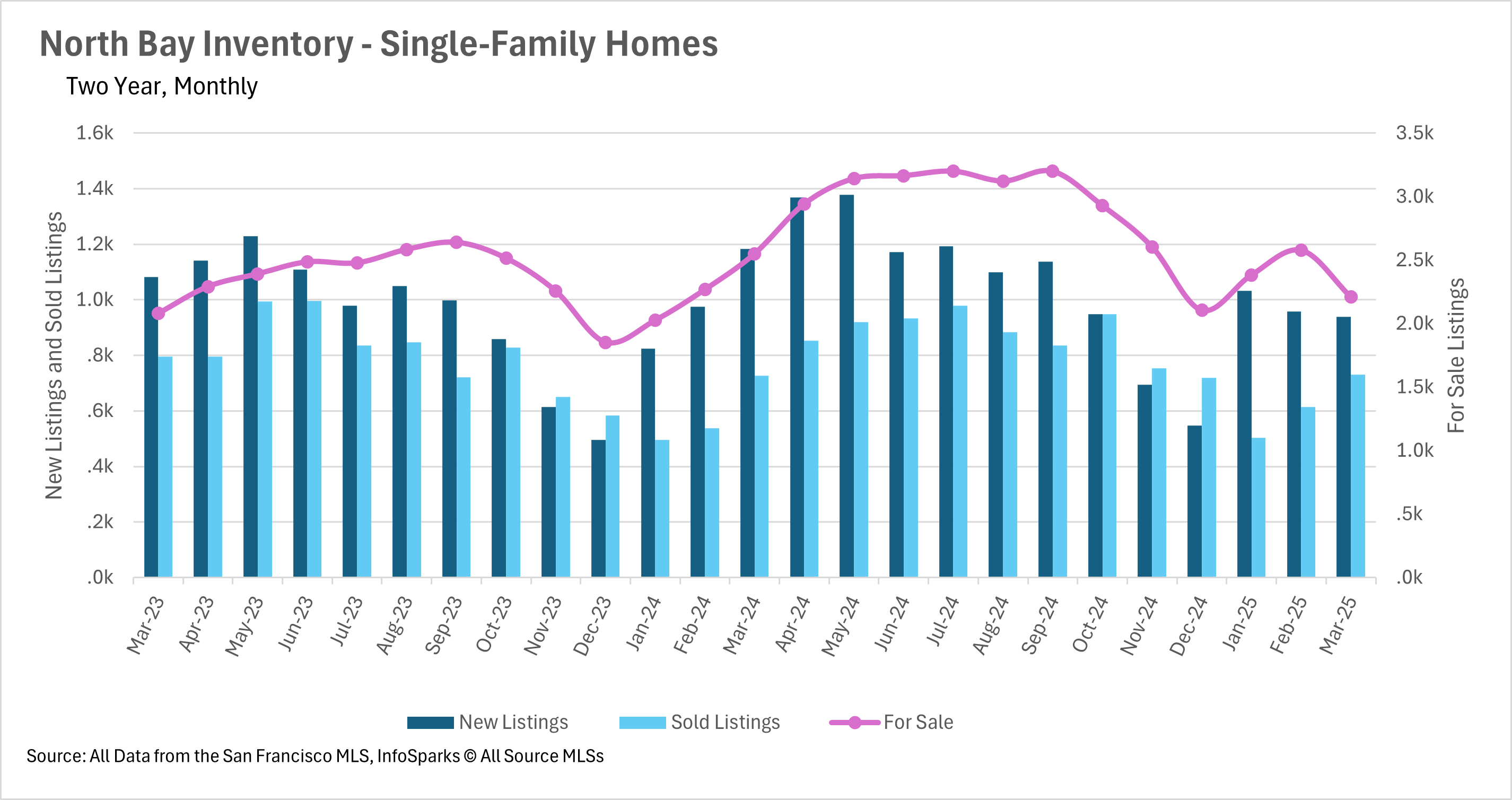

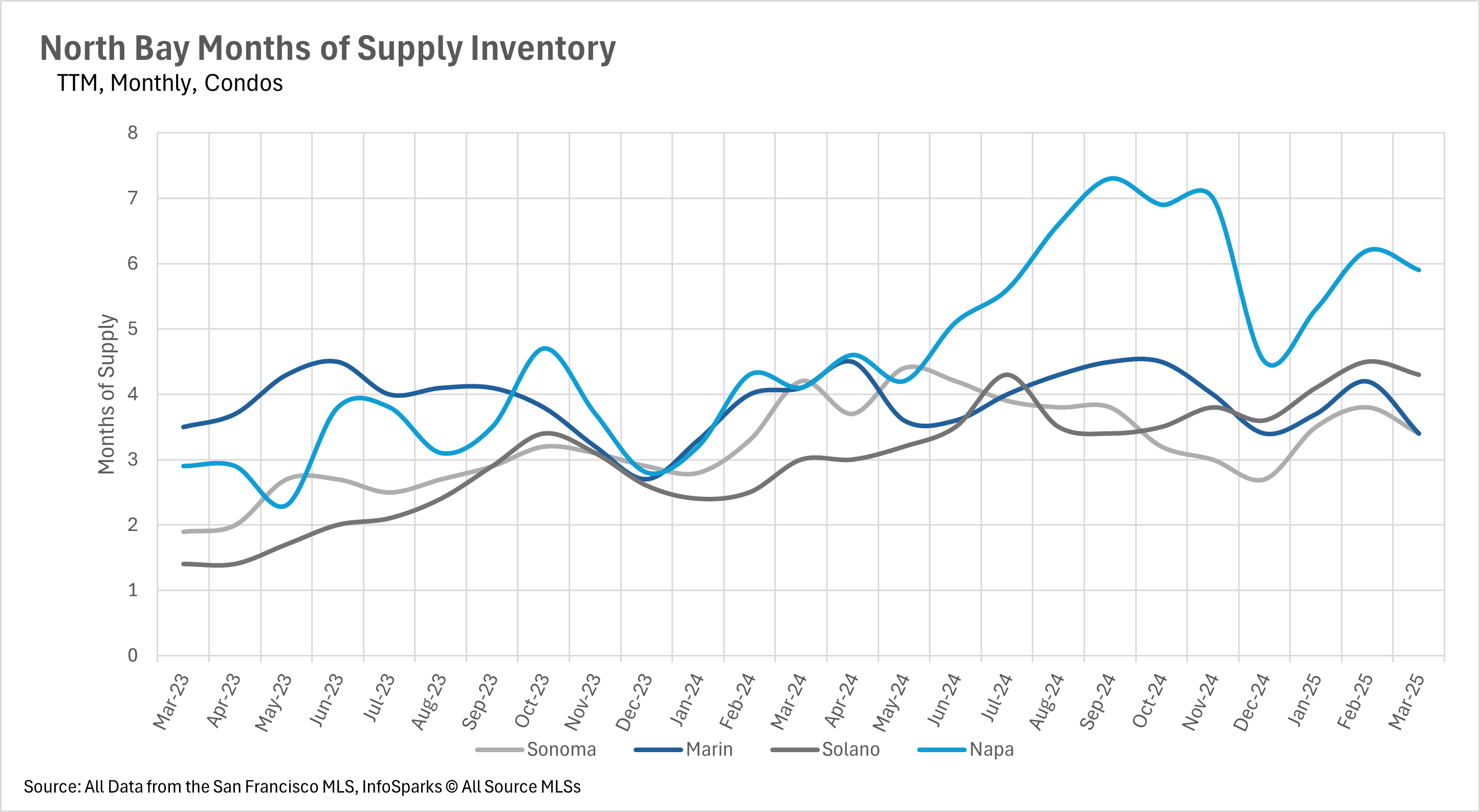

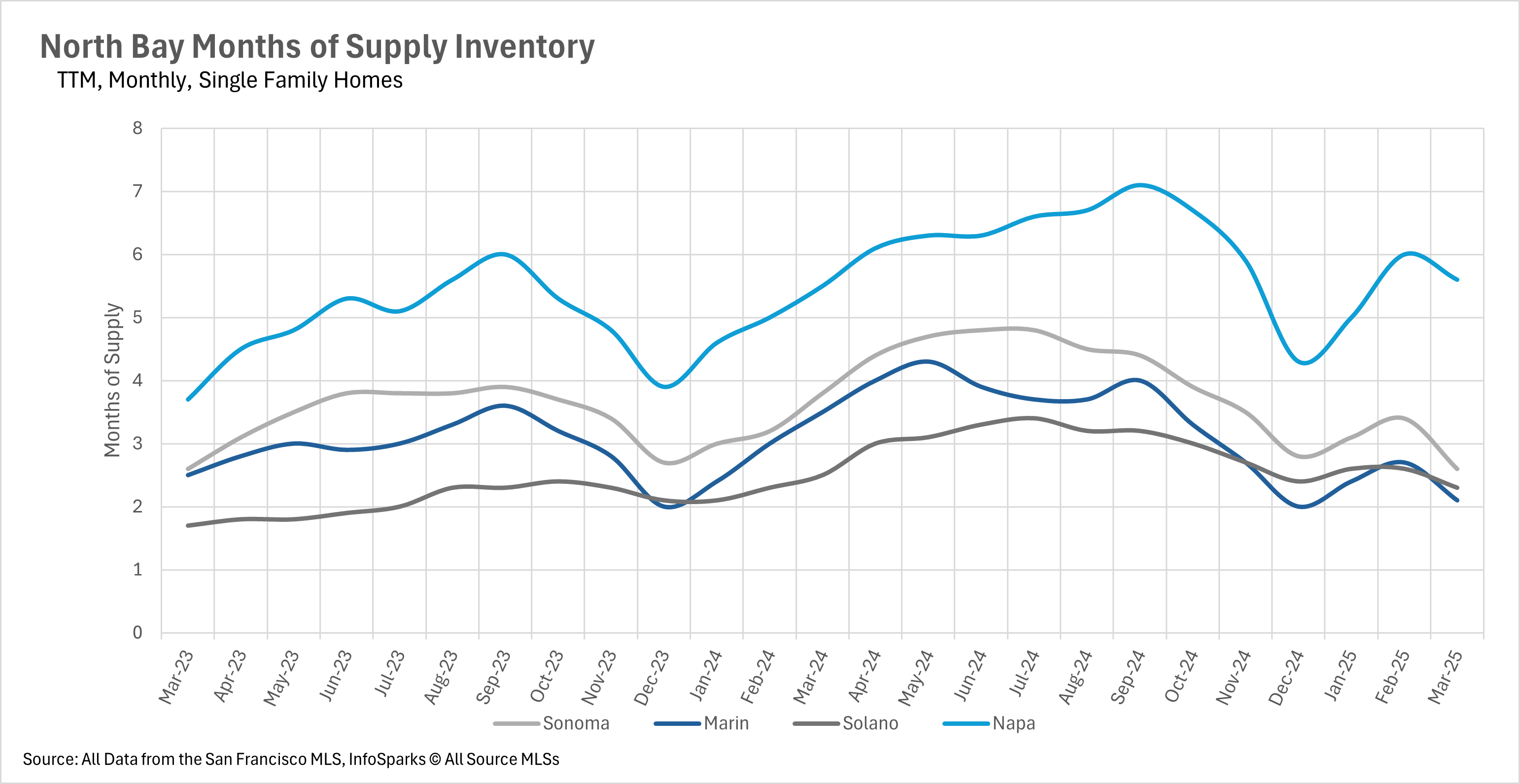

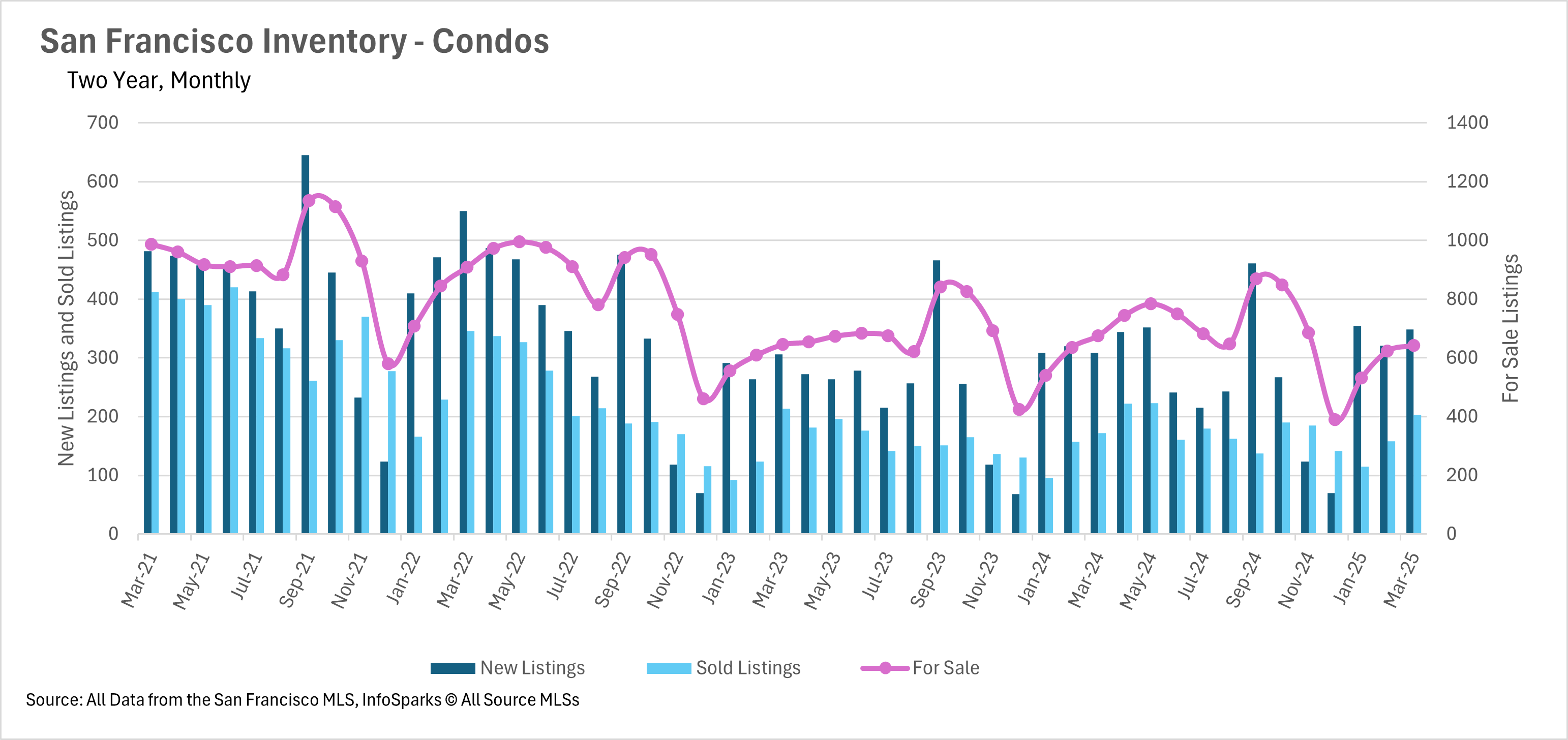

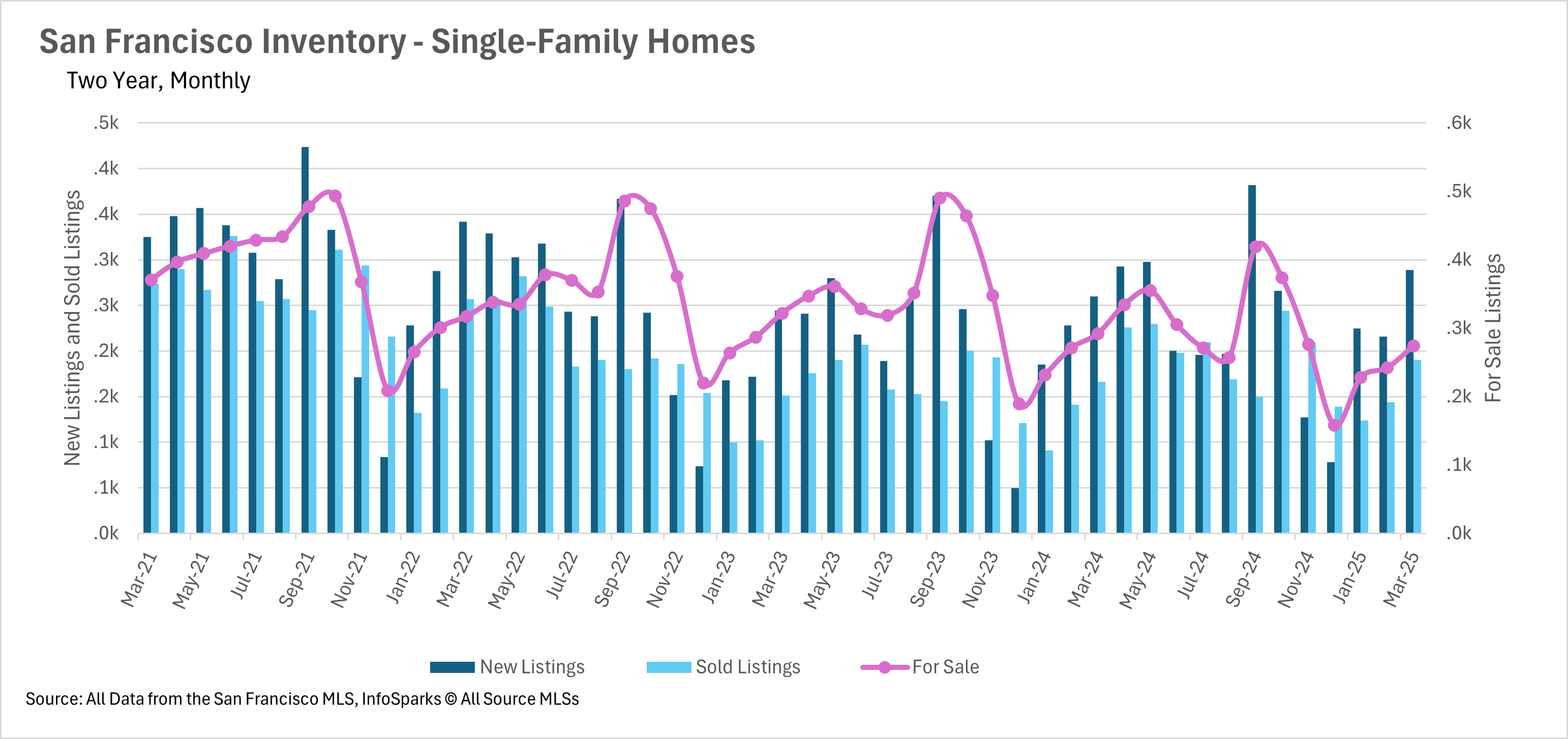

Inventory trends across the Bay Area show significant regional differences. Silicon Valley is experiencing substantial inventory growth, with single-family home inventories increasing by 40.05% in March, boosted by a 23.83% jump in new listings compared to last year. Similarly, the East Bay saw active listings increase by 47.79% year-over-year, with new listings in March up 16.78%. In stark contrast, San Francisco continues to struggle with inventory shortages, particularly for single-family homes, with just 1.5 months of supply available. The North Bay region is also facing inventory challenges, with a 14.28% month-over-month decrease in March and 20.78% fewer new listings compared to March 2024. These divergent inventory trends are creating different market dynamics across the Bay Area regions.

Days on market vary dramatically by region

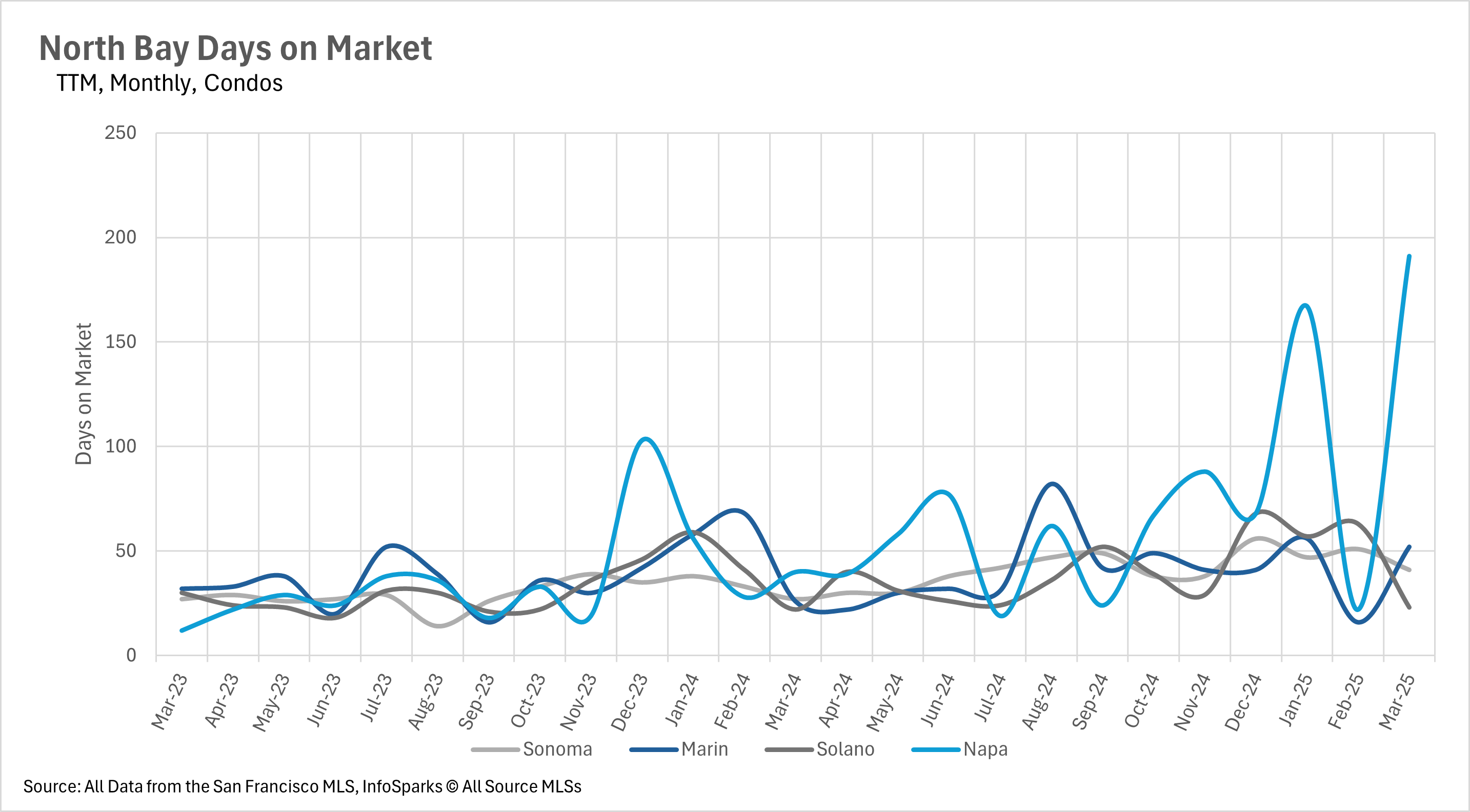

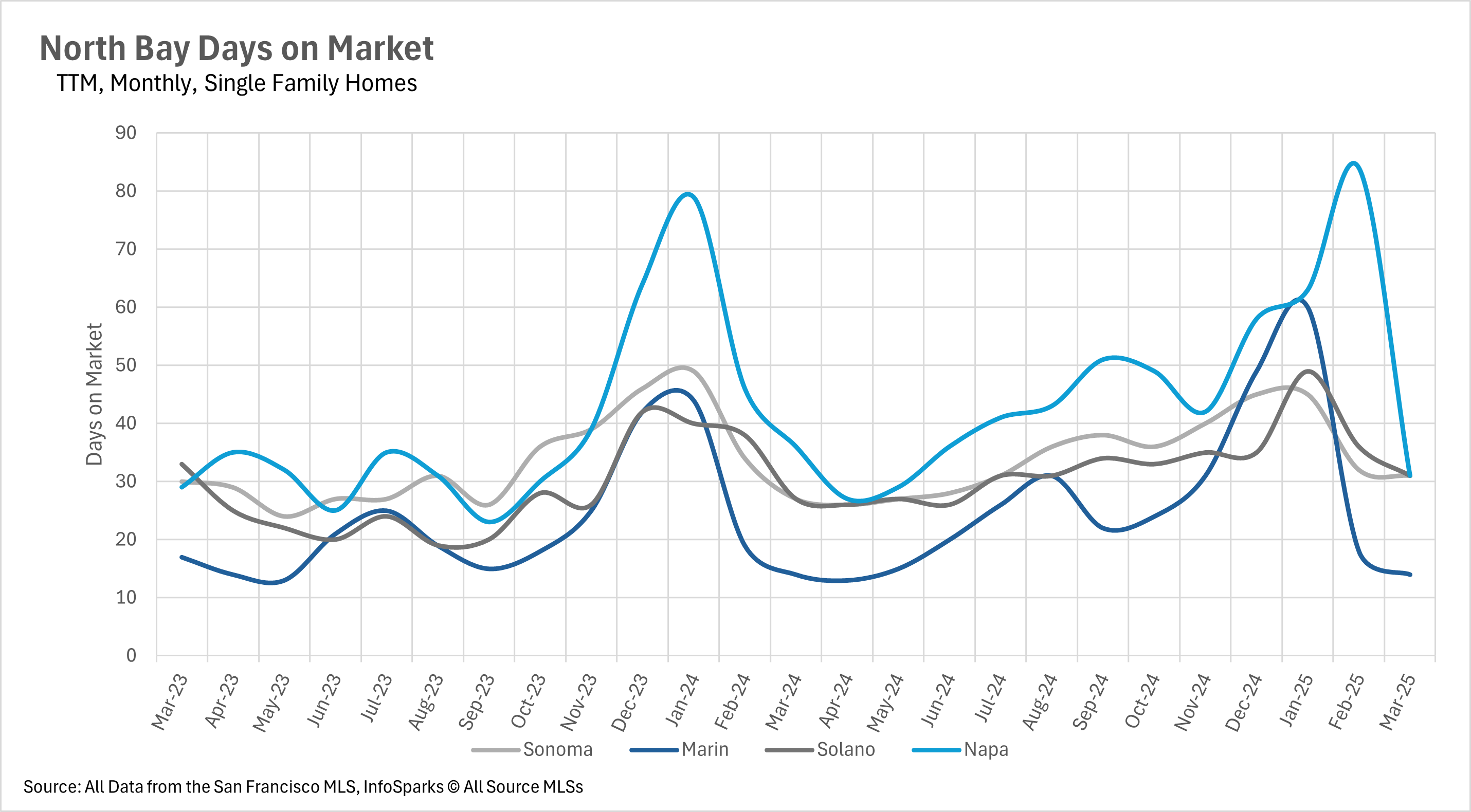

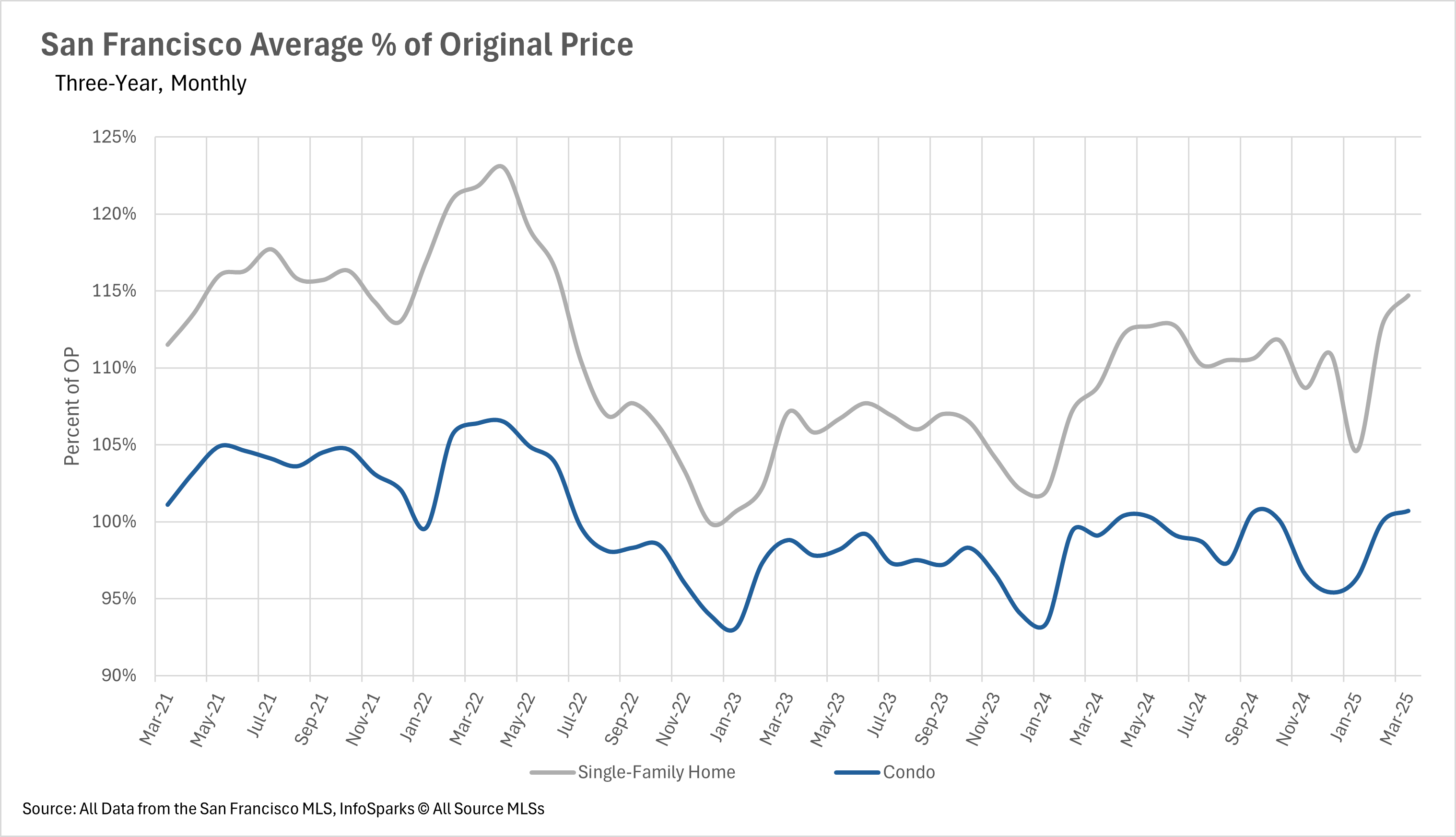

One of the most striking variations across Bay Area markets is the time homes spend on the market before selling. Silicon Valley homes are being snapped up quickly, with the average listing lasting just 8 days in Santa Clara, 10 days in San Mateo, and 16 days in Santa Cruz. The East Bay also shows relatively quick movement with homes typically selling in 12 days in Alameda County and 13 days in Contra Costa County, despite the significant year-over-year inventory increases. In San Francisco, single-family homes are seeing competitive bidding, selling for 114.7% of their original asking price - a level not seen since before the Fed began raising interest rates in June 2022. This contrasts sharply with markets like the North Bay, where homes in Sonoma and Solano counties are spending approximately 15% longer on the market compared to last year.

Market balance favors sellers for single-family homes, buyers for condos

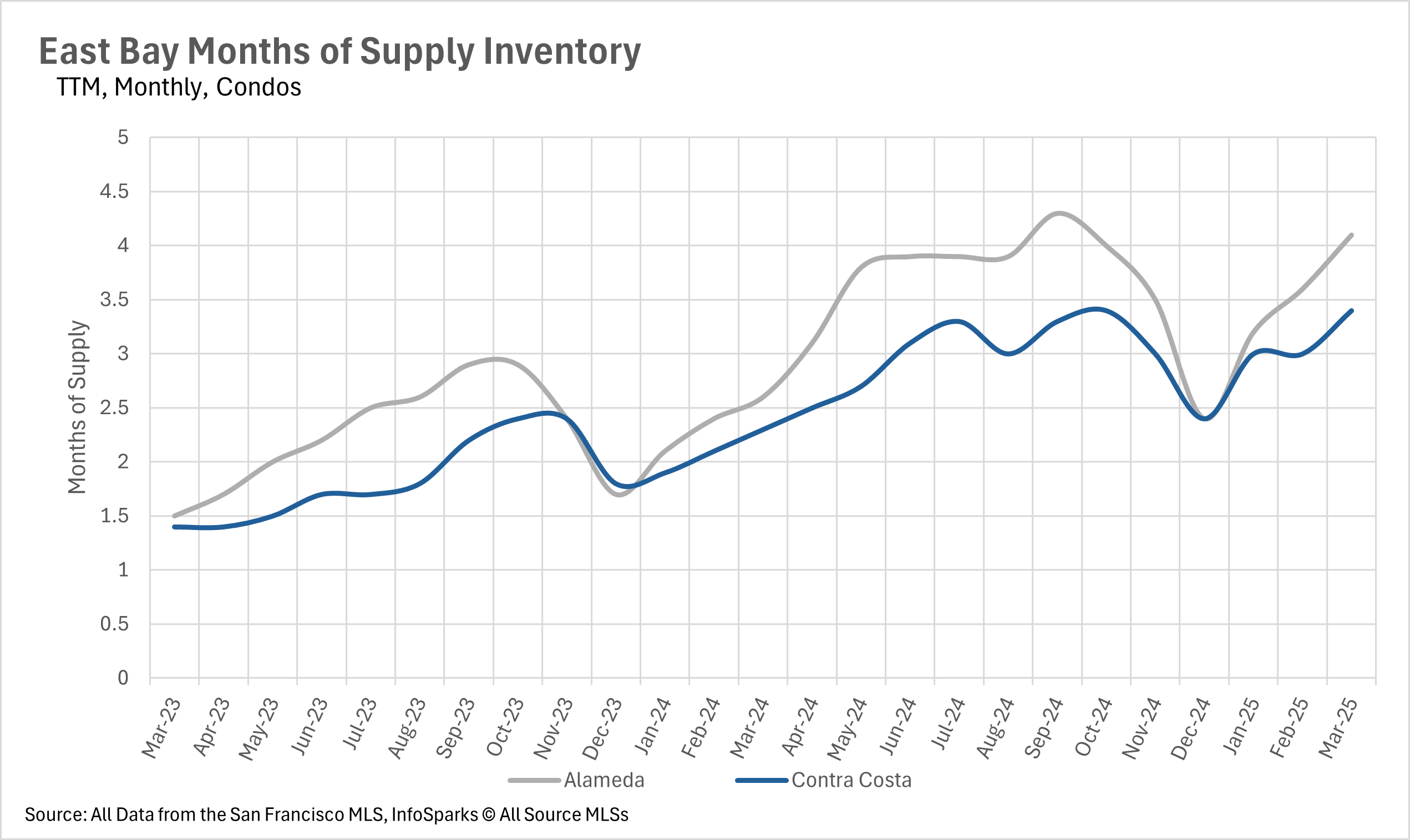

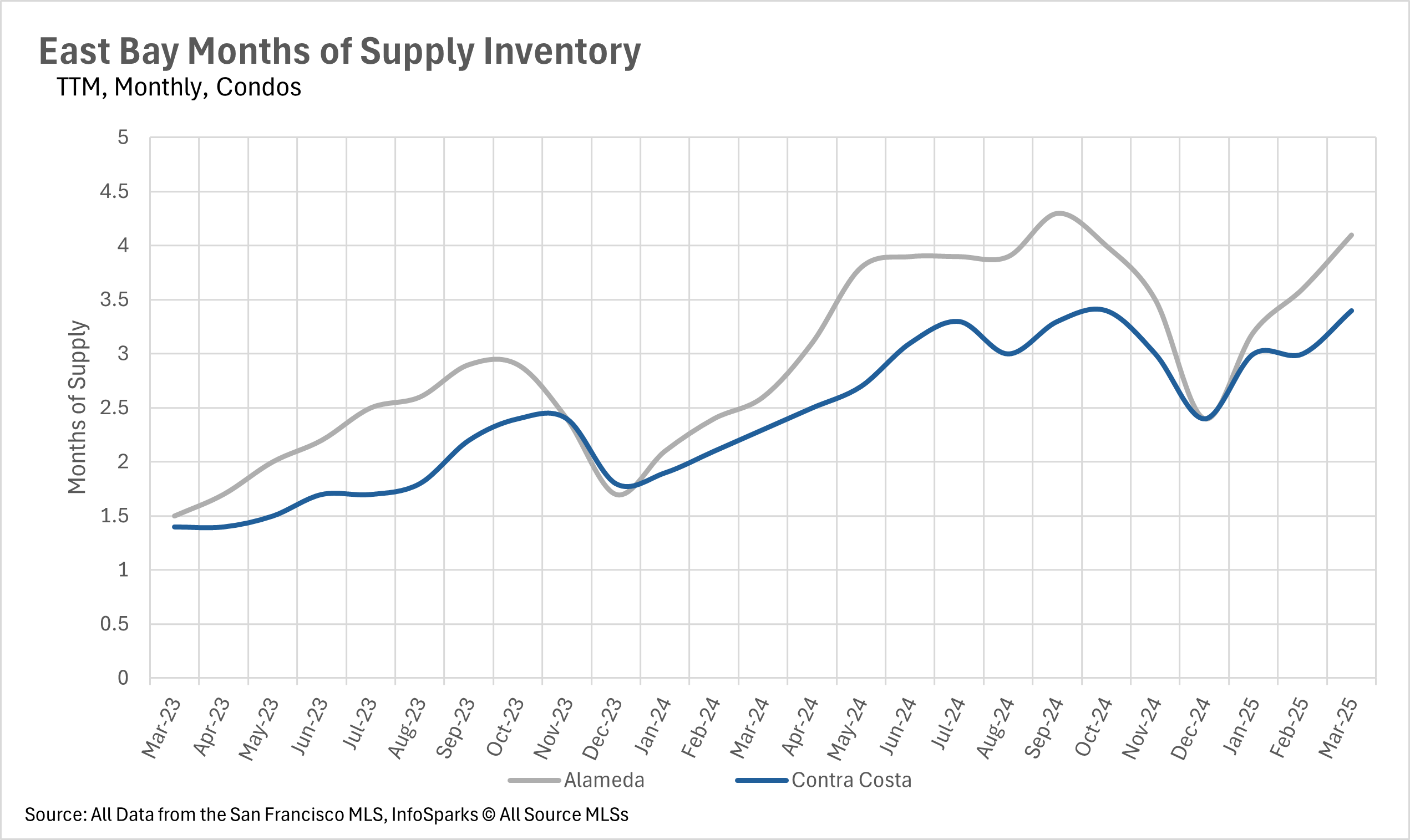

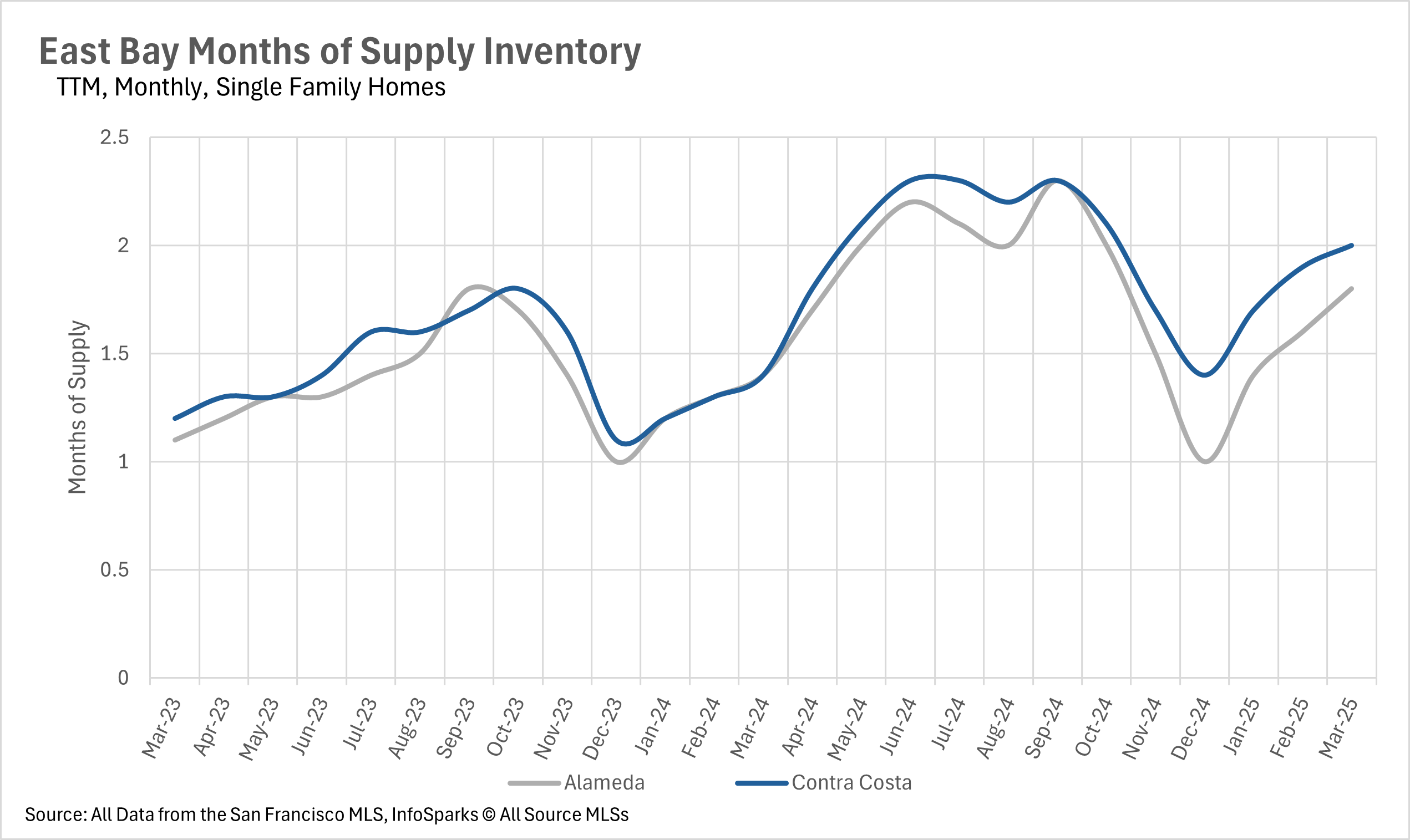

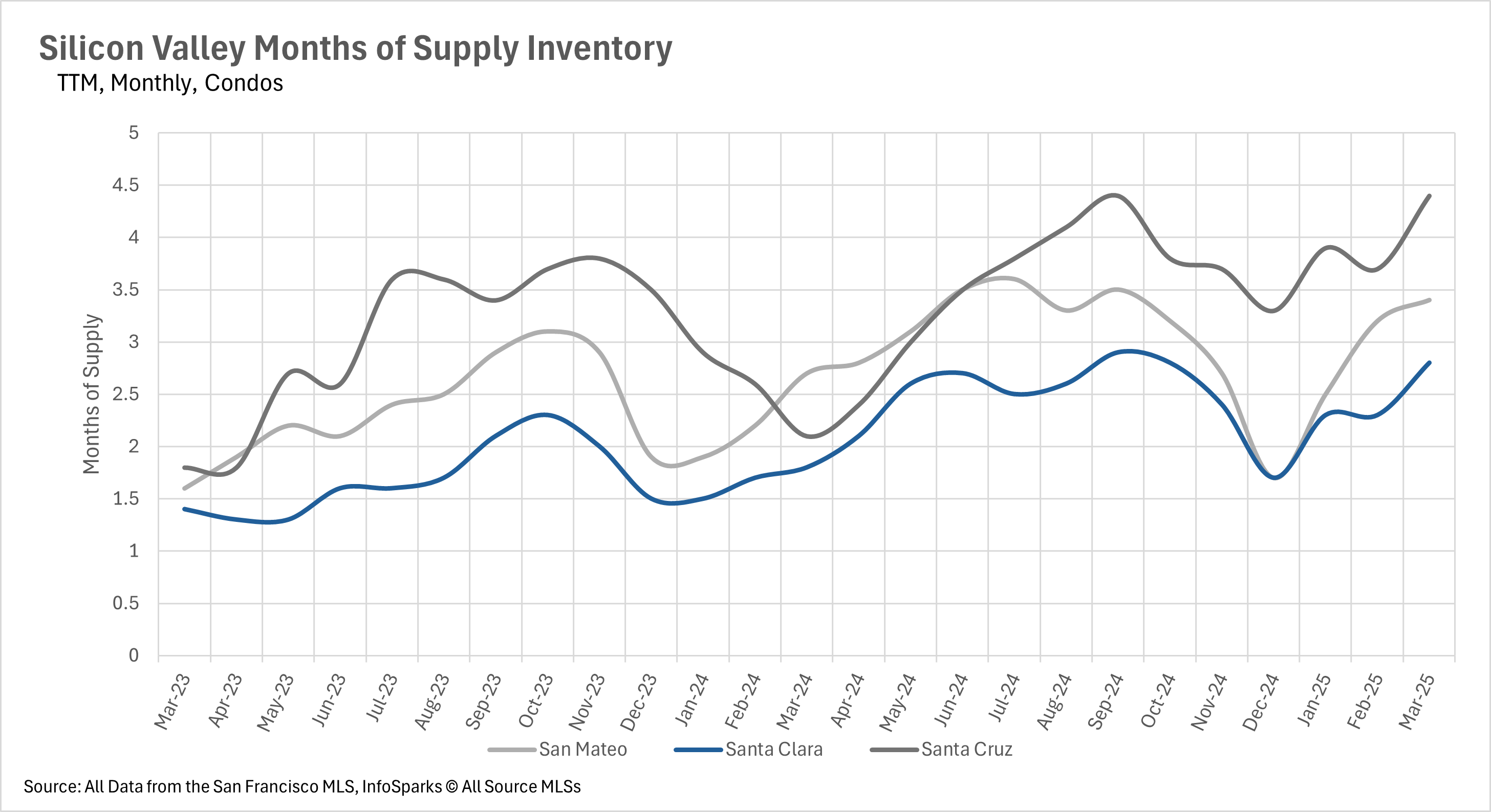

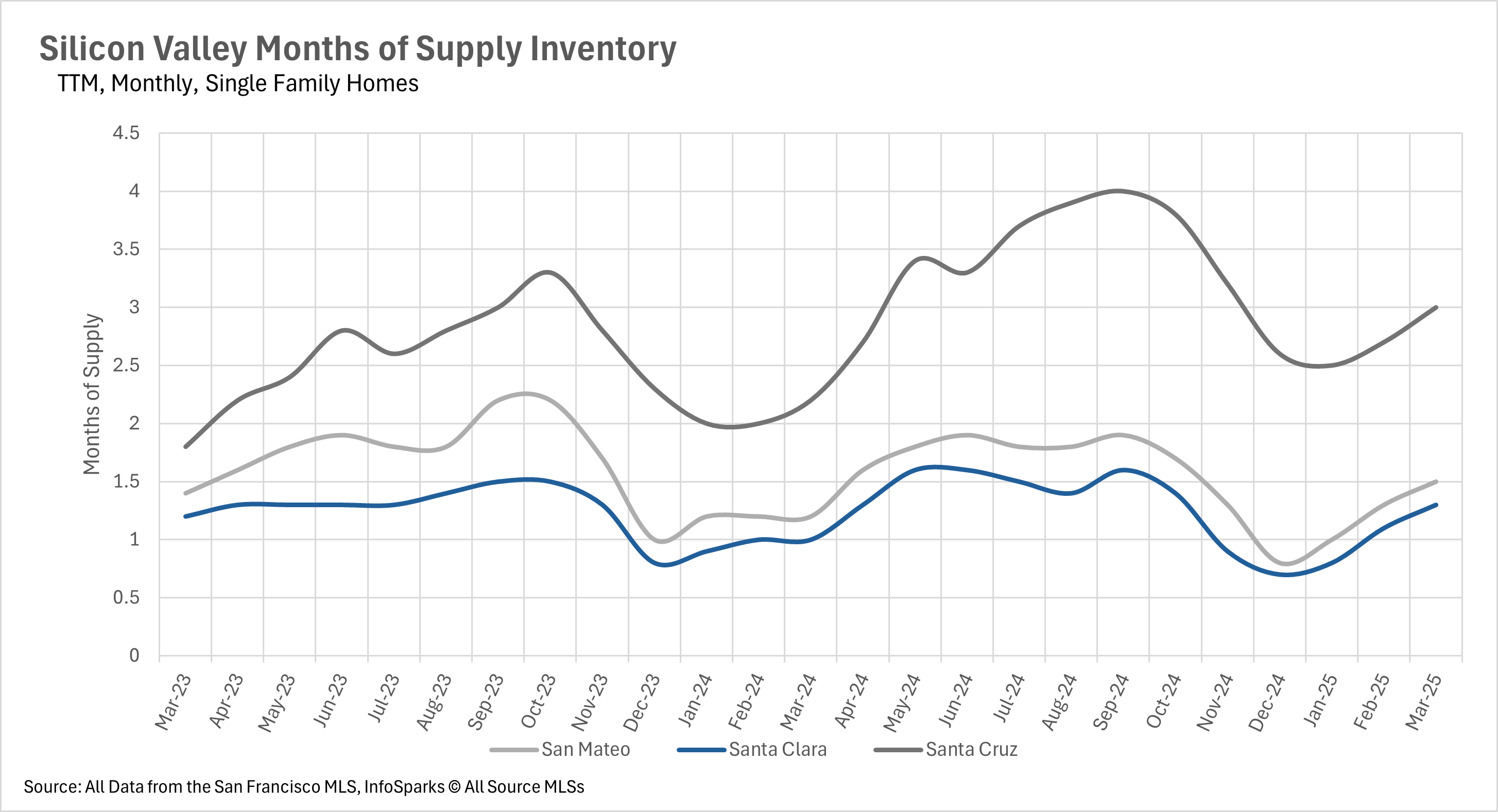

When assessing whether markets favor buyers or sellers, the months of supply inventory (MSI) metric provides clear insights. Historically, California averages around three months of MSI, with lower figures indicating a seller's market and higher figures a buyer's market. Across most of the Bay Area, single-family homes remain firmly in seller's market territory, with Silicon Valley showing just 1.3 months in Santa Clara and 1.5 months in San Mateo (though Santa Cruz is balanced at exactly 3 months). The East Bay reflects similar seller advantage with 1.8 months in Alameda County and 2 months in Contra Costa County. San Francisco has just 1.5 months of single-family home inventory, while most of the North Bay (except Napa County at 5.6 months) also favors sellers. However, the condo market tells a different story, generally favoring buyers with higher inventory levels - 2.8 months in Santa Clara, 3.4 months in San Mateo, 4.4 months in Santa Cruz, 4.1 months in Alameda, 3.4 months in Contra Costa, and 3.7 months in San Francisco. This distinct split between single-family home and condo markets is consistent throughout the Bay Area.

Local Lowdown Data